The Purpose and Practicality of Sinking Funds

Sinking funds are the superheroes of the financial world when it comes to preparing for planned expenses. They serve a simple, yet vital purpose: to spread the cost of significant expenditures over time, avoiding financial strain. Whether you’re looking forward to a dream vacation, prepping for festive season expenses, or bracing for the inevitable car repair, a sinking fund translates those large, one-off payments into doable, monthly savings. In practice, this not only provides peace of mind but also fosters a disciplined approach to saving. The practicality of sinking funds comes from their ability to prevent debt accumulation, allowing you to live within your means while still achieving your goals.

KEY TAKEAWAYS

- A sinking fund provides a level of protection for investors, making a company with debt more attractive for investment by ensuring there’s a way for investors to recoup their money in the event of default or bankruptcy.

- The establishment of a sinking fund may enable a company to secure lower interest rates on debt due to the increased security it provides to investors, as opposed to higher rates that would otherwise accompany poor credit ratings.

- Maintaining a sinking fund enhances a company’s financial stability by demonstrating its ability to repay debts and buy back bonds, leading to a stronger credit standing and increased confidence among investors.

Breaking Down the Sinking Fund Strategy

How Does a Sinking Fund Work?

A sinking fund works by allowing you to reverse-engineer your savings strategy. First, you decide on a financial goal. Let’s say you want to buy a new laptop in a year, and it will cost $1,200. You’d then break that total cost down into smaller, monthly amounts. If you start saving now, you’ll need to put aside $100 each month. Every month, you transfer that $100 into your sinking fund, a separate savings pot, and watch it grow. When the year is up, you’ll have the cash ready to make the purchase without reaching for a credit card or dipping into emergency savings. This methodical approach ensures that when it’s time to pay, the money’s there, waiting and ready.

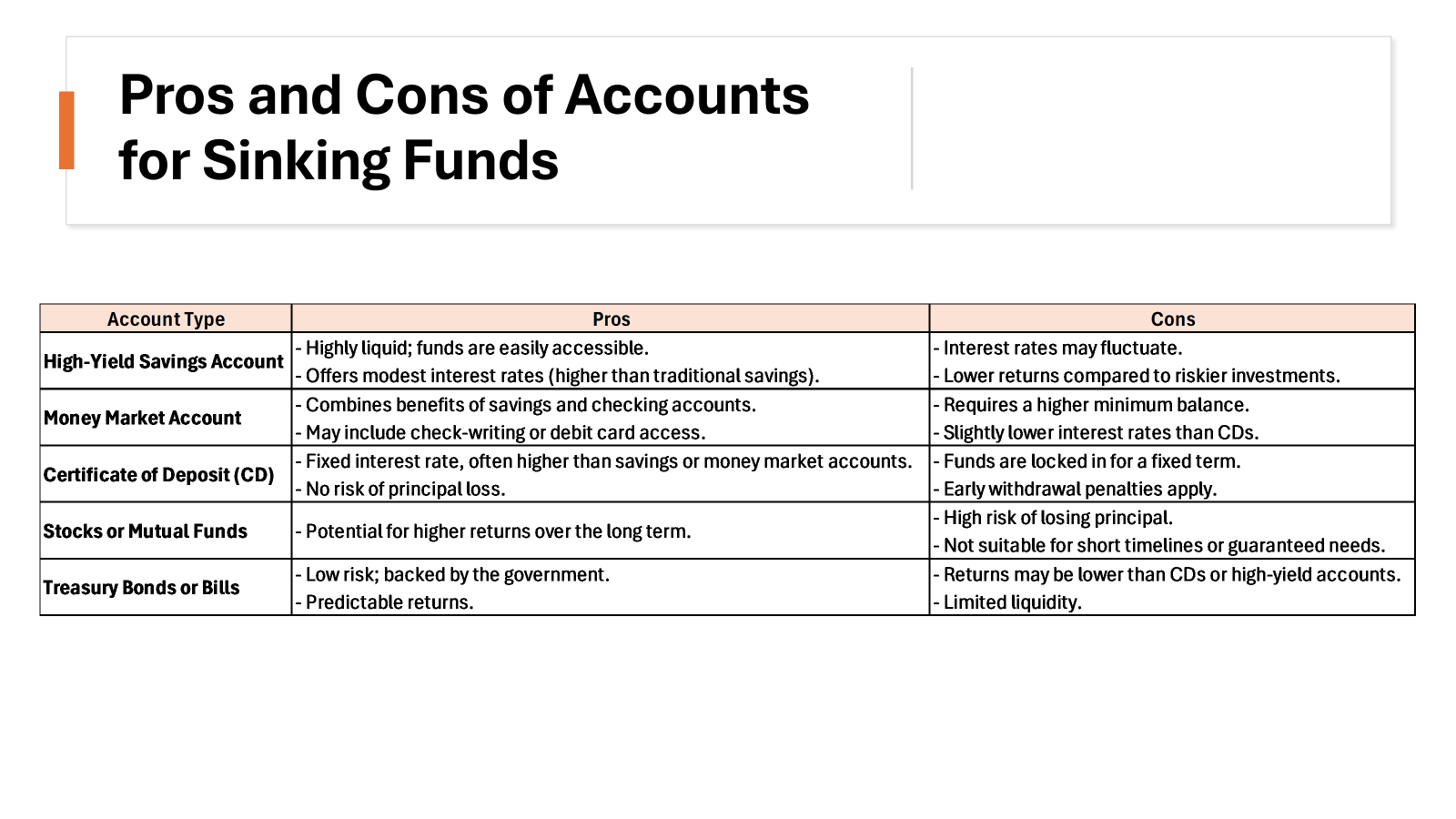

Should You Invest Your Sinking Fund?

When it comes to your sinking fund, it’s wise to prioritize accessibility over potentially higher returns from riskier investments. If your saving timeline is short (like a year or less), stick with liquid accounts — think high-yield savings accounts or money market accounts. These options offer modest interest while keeping funds easily available.

For longer-term saving plans (several years out), you might consider a certificate of deposit (CD). CDs can offer higher interest rates but come with the caveat that your money is locked in for a specified period. It’s generally advised against investing your sinking fund in the stock market due to the risks that can lead to a loss of your principal – the exact opposite of what sinking funds are designed for: a guarantee that funds will be there when you need them.

Setting Up Your Sinking Fund Step by Step

Identify Your Savings Targets

Before diving into the world of sinking funds, take time to pinpoint your savings targets. Start by listing down any large expenses coming up in the future, such as holiday gifts, car maintenance, property taxes, or even a kitchen remodel. Next, put a price tag on each goal. If you’re not sure of the exact amount, base your estimate on past expenses or the average costs you can research.

Once you have your list of expenses and their estimated costs, prioritize them. Decide which expenses are must-haves versus nice-to-haves and order your list accordingly. This will provide a clear picture of your saving objectives and help you determine where to funnel your sinking fund contributions first.

Plan Your Saving Schedule

With your savings targets in hand, it’s time to create a roadmap. Determine how much time you have before the expense is due and how much you can realistically save from each paycheck. Suppose you’re aiming to save $3,000 for a holiday in 18 months. You’d divide $3,000 by the number of paychecks you’ll receive in that period to find out your saving rate per paycheck.

Then, choose a contribution frequency that aligns with your cash flow—weekly, bi-weekly, or monthly are common options. By calculating your contribution amount and establishing a regular deposit schedule, you’ll turn lofty savings goals into routine financial habits. This systematic approach ensures your sinking fund grows steadily, making the final expense far less intimidating when the time comes.

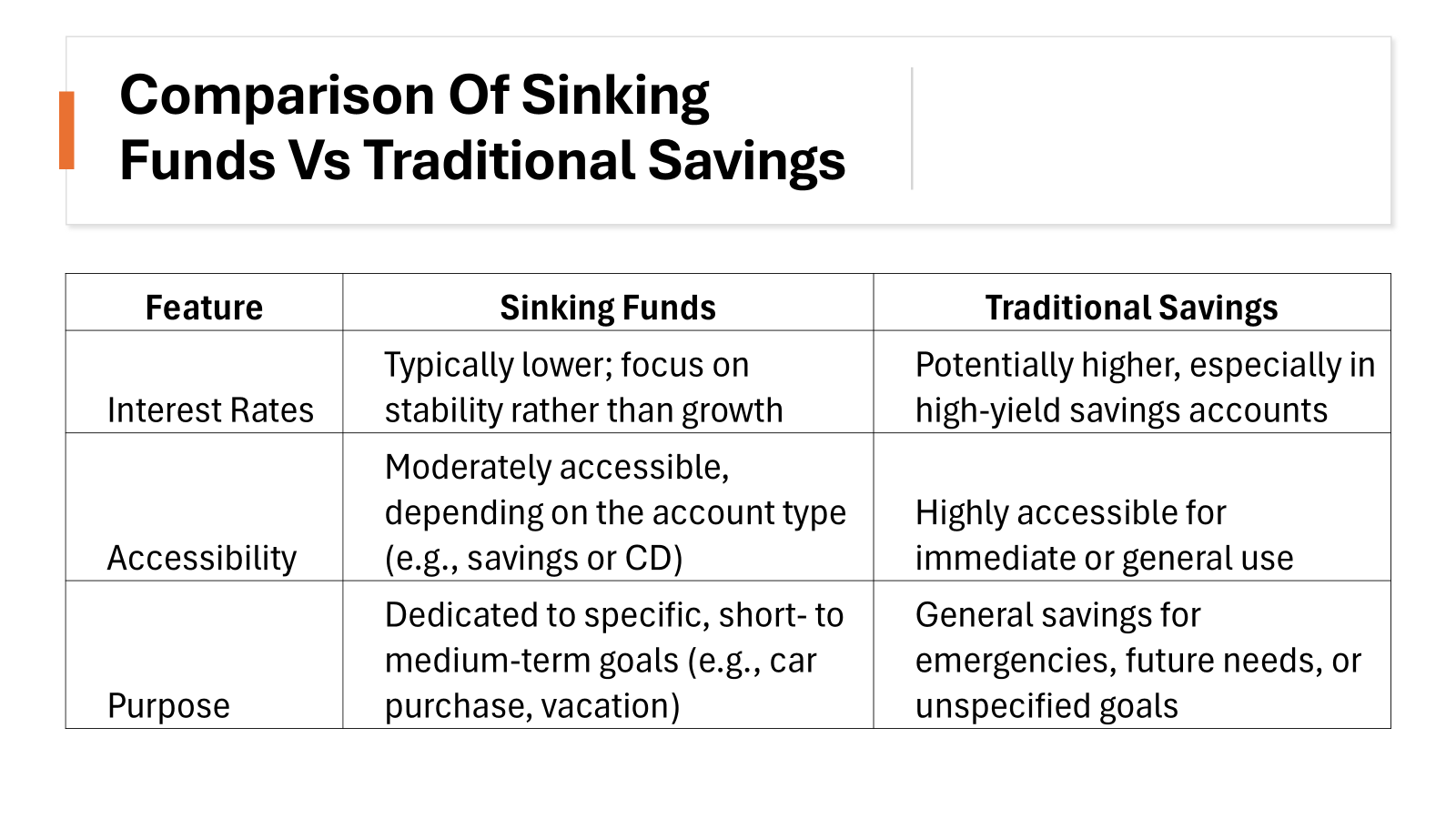

Sinking Fund vs. Savings Account: Making the Distinction Clear

Advantages of Sinking Funds Over Traditional Savings

Sinking funds bring a level of organization and clarity to your finances that traditional savings accounts often lack. They focus on saving for specific purposes, which makes it less tempting to dip into funds for non-essential items. By virtue of their targeted nature, you might also feel more committed and motivated — watching a vacation or home renovation fund grow can be particularly satisfying.

Additionally, sinking funds could potentially offer financial benefits. For instance, you can shop around for accounts that might yield a better interest rate than your regular savings account, further boosting your savings. Moreover, if you’re saving for a debt repayment, like a bond, sinking funds can reduce overall interest payments by decreasing debt ahead of schedule, and they may improve your creditworthiness by demonstrating financial responsibility.

Sinking Fund or Emergency Fund: Knowing When to Use Each

Understanding the difference between a sinking fund and an emergency fund is crucial for sound financial planning. Use your sinking fund for known, upcoming expenses you can anticipate – like annual insurance premiums, back-to-school shopping, or predictable home repairs. It’s like having a mini-budget within your budget for those larger bills that only pop up once in a while but aren’t surprises.

In contrast, your emergency fund is your financial safety net for life’s unpredictable moments—the unplanned, the unexpected, and the emergencies. When the car suddenly breaks down or you face medical emergencies, your emergency fund is there to cushion the blow, ensuring such surprises don’t derail your finances.

In short, draw on your sinking fund for the expenses you can foresee, and preserve your emergency fund strictly for those you can’t.

Real World Examples: Sinking Funds in Action

Common Expenses Ideal for Sinking Funds

Your sinking fund can transform how you manage a variety of expenses. It’s perfect for one-time or infrequent expenditures, like saving for a wedding, which can be quite sizable, or annual insurance premiums, which sometimes catch you off guard. Major home repairs or renovation projects also fit the bill; setting aside money regularly means those necessary fixes or updates won’t leave you strapped for cash.

Sinking funds also apply to life’s inevitable, but not always predictable, moments: car accidents, unexpected car repairs, medical or dental emergencies, and last-minute travel. Moreover, they’re ideal for more joyous occasions, such as holiday or vacation savings, or even preparing for a new family member’s arrival. Essentially, any significant expense that you can see on the horizon is a candidate for its own sinking fund.

Success Stories: How Sinking Funds Make Big Purchases Easier

Sinking funds have turned financial dreams into reality for many. For example, one family was able to afford a dream vacation to Europe by starting a sinking fund a year and a half in advance. They calculated the cost, broke it down into monthly savings, and by the time the trip rolled around, they were fully funded without any stress.

Another person may share their success in using a sinking fund for home renovations. They started saving well before the planned start date and, by the time they were ready to begin, they had enough to cover all the costs, avoiding the burden of a loan or maxing out credit cards. Success stories like these highlight the empowering effect sinking funds can have, allowing individuals and families to make significant purchases or investments with ease and confidence.

Tips for Managing Multiple Sinking Funds

Staying Organized with Your Funds

Keeping your sinking funds organized is key to ensuring each dollar you save is working towards its intended purpose. Start by labeling each fund clearly—either within a budgeting app or on a spreadsheet—so there’s no confusion about what each fund is for. Consistency is also crucial; make regular contributions and track them meticulously.

If you’re a fan of technology, use budgeting tools or apps that offer features like virtual envelopes or separate accounts for each goal. For the more old-fashioned, a ledger or notebook can work just as well. Regardless of the method, the goal is to have a clear, up-to-date record of your contributions and balances for each sinking fund.

Balancing Sinking Funds with Other Financial Priorities

Juggling multiple sinking funds along with other financial commitments can be like walking a tightrope. To maintain balance, never allow your sinking fund contributions to compromise essential expenses or emergency savings. A sound strategy is to pay yourself first by depositing into your emergency fund and retirement savings, then allocate what’s left into your sinking funds.

Additionally, keep your financial goals aligned with your income. Resist the temptation to create a sinking fund for every foreseeable expense if it stretches you too thin. Instead, focus on a few top priorities to ensure you can meet all your obligations without sacrificing your financial stability. It might mean sacrificing smaller goals in the short term but keeping your financial foundation strong is paramount.

Potential Pitfalls and How to Avoid Them

Common Missteps When Using Sinking Funds

Even the most well-intended saver can stumble when dealing with sinking funds. A common misstep is failing to regularly contribute, which can lead to a last-minute scramble to meet your savings target. Another pitfall is treating your sinking fund like a discretionary spending account, which defeats its purpose. Rein in the impulse to raid these funds for unrelated expenses, no matter how tempting it may be.

Not calculating accurate cost estimates for your goal can also backfire, leaving you short when the bill comes due. Stay realistic about costs and adjust your contributions if prices change. Finally, overlooking the need for separate accounts or clear labels can make it difficult to track your progress and stick to your plan. Maintain separate, clearly defined funds to keep everything straight.

Ensuring Your Sinking Fund Stays Afloat

To keep your sinking fund afloat amidst financial ebbs and flows, stay consistent with contributions. Life will throw curveballs, and your budget may shift, but try to contribute something each time you’re paid. Adjust if necessary, but keep the habit alive.

Review your sinking fund goals regularly to ensure they still align with your priorities and make adjustments as your financial situation evolves. If an emergency drains your funds, regroup and rebuild without getting discouraged. Keeping a buffer in your sinking fund can also protect against unexpected cost increases for your planned expense.

Remember, flexibility is a strength, not a weakness. If you need to pause or redirect funds to deal with a financial surprise, do so — just circle back to your sinking fund plan as soon as you’re able.

Conclusion

A sinking fund is a financial reserve specifically set aside by an organization or individual to repay debt or replace long-term assets. In business accounting, sinking funds are often used by companies to ensure the availability of resources to meet financial obligations, such as bond repayment, without creating a financial strain. For instance, corporations issuing bonds often establish a sinking fund to systematically save for the bond’s principal repayment, reducing the likelihood of default or bankruptcy. This disciplined approach to financing not only instills confidence among investors but also improves the company’s creditworthiness in the marketplace.

The usage of sinking funds extends beyond bonds. They can serve as a reserve fund to handle hardship situations or unforeseen shortfalls, such as the need to replace expensive equipment or address major repairs. By regularly contributing to a sinking fund, businesses and individuals can mitigate the risks of overspending and better plan for future expenses. Tools such as analytics and financial planning software can help monitor the fund’s growth and ensure its adequacy to meet its intended purpose.

From a banking perspective, the concept of sinking funds aligns with the principle of financial preparedness. Just as an individual might save money in a savings account or use an ATM card to withdraw small amounts responsibly, businesses allocate resources to a sinking fund to avoid sudden large expenditures. Media outlets like CNBC often highlight the importance of such funds in maintaining financial health, particularly in times of economic uncertainty. By planning for predictable liabilities, organizations can reduce financial stress and avoid the guilt of failing to meet obligations.

Sinking funds also provide an opportunity for companies to benefit from discounts or other financial advantages. For example, a company that has accumulated enough in a sinking fund may redeem bonds at a discount before maturity, thereby reducing its overall cost of borrowing. Additionally, maintaining a sinking fund demonstrates sound financial management, which can support certification in financial standards or boost trust in the company’s financial practices. In summary, sinking funds are a vital component of strategic financial planning, ensuring stability and resilience against potential economic challenges.

FAQ: Common Questions About Sinking Funds

What Types of Expenses Should I use a Sinking Fund For?

Use a sinking fund for any large, planned expense, such as annual bills, appliance replacements, or personal goals like vacations and weddings. These funds are also ideal for periodic maintenance costs, such as vehicle servicing or home repairs.

How Many Sinking Funds Can I Have at One Time?

It depends on your budget and goals, but generally, keep it manageable. Aim for a few key sinking funds to avoid spreading your finances too thin and to ensure meaningful progress in each.

Where Is the Best Place to Keep My Sinking Fund?

The best place for your sinking fund is in a high-yield savings account. It keeps your money safe, accessible, and earning interest without the risks tied to investment accounts.

Can Sinking Funds Actually Help Improve My Credit Score?

While a sinking fund itself doesn’t directly affect your credit score, it can lead to better financial habits that improve credit. By saving for and paying off debts on time, you demonstrate creditworthiness, which can boost your score.

Is There an Ideal Amount of Money to Save in a Sinking Fund?

The ideal amount for a sinking fund varies based on your specific financial goal. Calculate the total cost of your expense, then divide it by the amount of time you have to save to find your ideal monthly saving amount.

What is the meaning of a sinking fund?

A sinking fund is a savings tool specifically for accumulating money over time to pay for a future expense or debt, ensuring when the bill arrives, the funds are ready and waiting.

What is a bond sinking fund?

A bond sinking fund is a provision in which the issuer sets aside assets to retire a portion of the bond issue before maturity, reducing risk and ensuring the ability to pay back bondholders.

What are the benefits of bonds with sinking funds?

Bonds with sinking funds are attractive to investors for their added security, potentially lower interest rates, and the issuer’s demonstrated commitment to fiscal responsibility.