By using financial tools like the CAPM, which considers market volatility and the specific riskiness associated with individual stocks, investors can quantify the RRR. This methodology can help investors compare the expected return (re)on equity investments with the level of uncertainty they are willing to tolerate. Think of the RRR as a benchmark or a hurdle rate that your investment must leap over to prove that it’s worth your time and money.

By incorporating the RRR into your investment evaluation, you can gauge if an opportunity will likely meet or exceed your financial aspirations, helping to navigate the inherent uncertainty of equity investing.

Exploring the Basics of RRR

An investment’s journey isn’t without its ups and downs, and the Required Rate of Return (RRR) is the savvy investor’s tool for understanding just what those rollercoaster rides might look like. At its core, the RRR helps you, as an investor, to pinpoint the lowest return you should accept to make an investment worthwhile, factoring in the various risks, including the riskiness of your chosen securities. In simpler terms, it’s the percentage of profit or gain you expect to receive from an investment to justify the risks you’re taking.

Calculating the RRR isn’t a whimsical guess; rather, it merges the risk-free rate—usually based on government bonds, often referred to as “return rf”, with the risk premium, an additional return expected for bearing extra risk. The risk premium can be understood as the equity risk premium (ERP), which represents the additional return expected for investing in the broader stock market over the risk-free rate. It’s not as simple as apples to apples but more apples to a fruit basket, where the risk premium is the diversity of fruits you’re eyeing, influenced by the volatility, or the riskiness, and the potential for loss or gain of your investment. The RRR isn’t static and will differ from one investment to another, ensuring your financial goals and risk tolerance are always aligned with your investment selections.

KEY TAKEAWAYS

- The Required Rate of Return (RRR) is pivotal in determining whether an investment opportunity is worth pursuing. It takes into account not just the expected return from the investment but also the associated level of risk, the time horizon for the investment, and the cost of attaining the necessary capital. The RRR must exceed the return obtained from risk-free investments in order to justify the additional risk.

- The calculation of the RRR involves several key inputs, including the overall expected market returns, the risk-free rate of return (such as returns from government bonds), the volatility or beta of the security in question, and the cost of capital for projects. The RRR for a given investment can vary among different investors or companies as it reflects their specific risk-return profiles, inflation expectations, and capital structures.

- The higher the Required Rate of Return, the more potentially lucrative, – The Required Rate of Return (RRR) is a critical financial metric employed by investors and companies to evaluate whether to pursue a potential investment, considering the minimum acceptable return given the risk involved, expected market returns, and investment time frame. The RRR must be greater than the risk-free rate to warrant the additional risk.

- The factors influencing the calculation of RRR include market returns, the risk-free rate of return, the investment’s risk level as measured by its volatility or beta, and a project’s overall cost of funding. Individuals and companies have varying RRRs due to differing risk-return preferences, inflation expectations, and capital structures.

- Practically, the RRR is instrumental for financiers and investors in determining appropriate investments and strategic decisions. It guides whether investing in assets, such as stocks or bonds, launching new products, acquiring equipment, or considering mergers and acquisitions, is financially justifiable when compared to other available options, especially in light of management fees and risk. The demand for a higher RRR typically correlates with the acceptance of greater investment risk.

Unpacking How RRR Is Calculated

Diving into the Capital Asset Pricing Model (CAPM)

Dive into the Capital Asset Pricing Model (CAPM) and you’re immersing yourself in a world that combines the thrill of the stock market with the precision of complex calculations. To tap into this treasure trove of financial modeling, you’ll be looking at the relationship between the expected return of an investment and its market risk, encapsulating what investors should expect as compensation for choosing riskier equities over risk-free securities. Understanding this relationship is crucial as it includes considerations of the equity risk premium, which seeks to quantify the additional return expected for investing in equities over a risk-free rate.

The CAPM formula, a stroke of financial genius that’s stood the test of time, is wonderfully straightforward yet loaded with insights:

[ R_e = R_f + \beta \times (R_m – R_f) ]

Here, ‘R_e’ stands for the cost of equity or the return an investor would like to earn to compensate for the riskiness they’re taking on. It can be refined using various equity models to better fit different investment scenarios. ‘R_f’ is our investment safety net, representing the return rf or the risk-free rate often sourced from stable government bonds. ‘Beta’, symbolized as ‘β’, represents the level of riskiness in comparison to the market – a stock with a beta above 1 is considered more volatile than the benchmark equity index. Lastly, ‘R_m’ denotes expected market return, assessing the average market performance to set a benchmark for equity returns.

With CAPM, you’re looking beyond the horizon, taking into account not just what you could earn from a risk-free investment, but also the premium you’d expect for choosing the adventure of the stock market instead, often indicated by the equity risk premium, which is incorporated into the model to adjust expectations for market realities.

Weighted Average Cost of Capital (WACC) Simplified

Untangling the Weighted Average Cost of Capital (WACC) unveils a financial metric that offers a glimpse into what a company pays for the capital it uses to fund operations and growth. Imagine a quilt where each patch symbolizes different sources of finance—some are equity, others are debt, and perhaps there’s a swatch for preferred stock, each being a distinct financing source within the company’s capital structure. WACC stitches these together, weighted by their proportion in the overall capital structure, effectively realigning their cost to reflect tax benefits. The formula takes the corporate tax rate (t), here standing at 25%, into account by allowing for the deduction of interest expenses.

To lay it out simply, WACC represents the average rate a company must pay to its security holders to finance its assets. Here’s the recipe for this financial concoction:

WACC= Wd×Rd×(1−Tc) + Wp×Rp + We×Re

Here, ‘Wd’, ‘Wp’, and ‘We’ are the weights of debt, preferred stock, and equity, respectively—think of them as the specific patches on your quilt representing different portions of the financing mix. Next, ‘Rd’, ‘Rp’, and ‘Re’ correspond to the costs of debt, preferred stock, and equity. These latter figures reflect the individual cost associated with each financing source, including a cost of equity (re) of 12% calculated using CAPM. Companies typically aim for a WACC that’s lower than the return on invested capital (ROIC), ensuring they’re creating value.

For investors, the WACC serves as a barometer for risk. A higher WACC signals that the financing costs—and consequently the risk—is more substantial, prompting investors to expect a higher risk-adjusted rate of return. It’s the financial world’s way of ensuring that companies acknowledge not just the average cost, but the true cost of their sources of capital after adjusting for the corporate tax rate, to fund their ventures and that investors are apprised of the stakes involved.

Practical Approaches to RRR

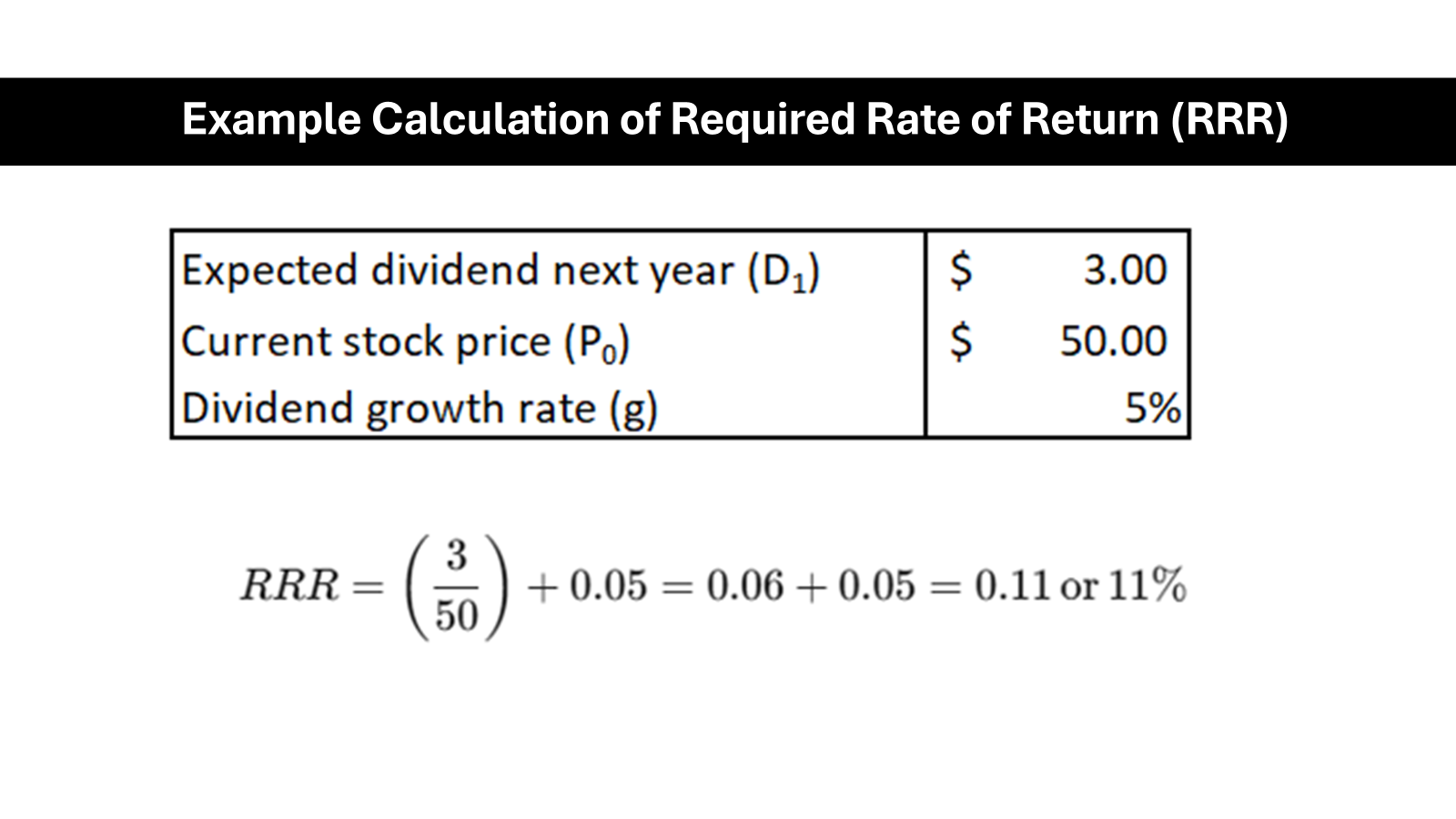

Calculating RRR for Equity Investments

Mastering the art of calculating the Required Rate of Return (RRR) for equity investments is akin to learning a secret handshake into an exclusive club; it’s where the rubber meets the road in investment analysis. The calculation of RRR is essential, especially when considering dividend income from equity shares, which can influence long-term investment strategies. The formula for calculating RRR on equity often hinges on anticipated future dividends and growth rates, incorporating models such as the dividend discount model and, at times, the equity model.

To set the scene, imagine a stock that pays dividends. You’d use the dividend discount model (DDM), considering factors like the expected dividend payment, the annual dividend growth rate, and the current stock price. The formula, as melodious as any financial refrain, might look something like this:

Here, ‘D1’ is the expected dividend in the next period, ‘P0’ the current stock price, and ‘g’ the expected dividend growth rate, which often reflects the company’s historical performance and future outlook. This method is particularly suited for income-oriented investors focused on stocks offering a verifiable way to forecast the RRR grounded in tangible, cash-based returns associated with mature, dividend-paying companies.

When dividends are not in the picture, the Capital Asset Pricing Model steps back into the limelight, or an investor might consider multi-factor discount models to account for the comprehensive risk factors. Calculating the RRR using CAPM factors in that nifty beta coefficient, reflecting the stock’s volatility relative to the broader market, alongside the expected market return and the risk-free rate. In particular, the Fama and French Multifactor Models or the Arbitrage Pricing Theory (APT) can offer a more nuanced assessment by including multiple economic factors.

No matter the formula used, calculating RRR for equity investments demands a keen eye on factors such as market trends, economic indicators, and the financial health of the company in question.

Assessing RRR for Debt Instruments

When you’re assessing the Required Rate of Return for debt instruments, you’re essentially looking to measure the promised land of interest against the quicksand of risk. Debt instruments, such as bonds, carry their own unique RRR calculations, primarily hinging on the yield to maturity (YTM), which is the total return anticipated on a bond if held until it matures.

Consider the YTM as the guiding star for bond investors. It blends the current market price, par value, coupon interest rate, and time to maturity to supply an annualized rate of return. The RRR for debt then takes into account this yield but also considers the bond rating, which paints a picture of its credit risk.

To calculate RRR for a bond:

[ RRR = YTM + Credit Risk Premium ]

The ‘Credit Risk Premium’ compensates you for the chance that the bond’s issuer might default. Bonds with lower credit ratings demand a higher premium to seduce investors into assuming that extra degree of risk.

This careful balancing act ensures that the interest rate you’re reaching for adequately rewards the treacherous tightrope walk of credit risk you’re performing by investing in bonds. Whether you’re eying corporate debentures or sovereign notes, grasping the RRR for debt instruments keeps your expectations tethered to the grounded realities of the debt markets.

RRR vs. Other Financial Metrics

Understanding RRR in Relation to Expected Rate of Return

When you’re sizing up the Required Rate of Return (RRR) and the Expected Rate of Return, you’re essentially playing matchmaker between what you hope to earn (expected return) and the minimum you need to earn (RRR) to make the risk worth it. It’s a dance between desire and necessity, forecasting and prudence.

The Expected Rate of Return tells a tale of optimism—based on past performance, forecasts, and the current market climate, it’s the return you predict will come from an investment. It doesn’t wear the bulletproof vest of guarantees, but provides an educated guess that helps shape your enthusiasm for a potential investment.

On the flip side, RRR is the protective parent, setting a benchmark that ensures you’re not just chasing rainbows. It’s driven by your personal risk tolerance, time horizon, and the market’s risk-free rate, plus a risk premium reflective of the investment’s volatility. If the expected return can’t outshine the RRR, the investment might not earn a place in your portfolio; it’s like saying, “Thanks, but no thanks” to a second date because the connection didn’t spark enough joy.

So, while these two rates often travel together in the investment journey, they serve distinct purposes helping you make heart and head agree on your financial decisions.

Contrasting RRR and Return on Investment (ROI)

Distinguishing between the Required Rate of Return (RRR) and Return on Investment (ROI) is like comparing a guardrail to the road itself. While both are essential navigational tools in the investment journey, they serve different purposes and provide different insights.

The RRR, standing firmly as the guardrail, represents the minimum threshold of profitability you demand from an investment, considering the risk you’re shouldering. It’s proactive, future-focused, and personalized, accounting for the return needed to justify an investment before you commit your funds.

In the lane of actual progress, ROI serves as the road itself—a retrospective and objective measure of an investment’s profitability after the fact. It’s calculated by considering the gain from an investment relative to its cost.

If the ROI busts through the RRR, it’s like a green light that the investment exceeded your minimum expectations. However, if ROI is crawling below the RRR, it’s a red flag that you may not be compensated enough for the risks you’ve taken.

Remember, the RRR sets the stage for what should happen, while ROI tells the tale of what did happen. They’re two sides of the same coin, each invaluable in guiding your investment endeavors toward safe and fruitful destinations.

Real-World Examples and Scenarios

Implementing RRR in Portfolio Management

When you slip the Required Rate of Return (RRR) into your portfolio management toolkit, you’re not just making a smart move; you’re ensuring that your investment mix is tailored precisely to your financial goals and risk appetite. Implementing RRR in crafting your portfolio is like dialing in the right temperature in your home—it makes for a comfortable and suitable investment climate.

Consider RRR as the yardstick when picking and choosing between potential investments. For each asset, you’ll be asking: Does this meet or exceed my RRR? If yes, it’s a candidate for your portfolio. If not, it’s left out in the cold. This means that higher-risk investments will need to promise higher returns to make the cut. Conversely, safer bets with lower returns might still find a cozy spot in your portfolio if they align with your RRR.

Calibrating your portfolio using RRR brings efficiency and focus to portfolio rebalancing as well. Should your RRR change—perhaps due to nearing retirement or a shift in financial circumstances—some investments may no longer fit the bill. You might reduce positions in high-volatility stocks in favor of steady-eddy bonds or dividend-rich utilities, thus maintaining the harmony between your portfolio and your evolving RRR.

By baking RRR into your portfolio management process, you’ll curate a well-tuned collection of investments that not just resonate with your personal financial symphony but also work in concert to achieve your long-term objectives.

Case Studies: Navigating RRR Adjustments Over Time

As you traverse the ever-changing terrain of the financial markets, the Required Rate of Return (RRR) is bound to evolve, akin to how a ship adjusts its sails to the shifting winds. These adjustments are a testament to the dynamic nature of investing, where the journey is as important as the destination.

Delve into the case studies of investors who’ve navigated the ebb and flow of RRR adjustments, and you will discover a wealth of strategy and adaptability. For instance, an investor initially comfortable with high-risk, high-reward tech stocks might realign their RRR downwards when nearing retirement age, favoring income-generating bonds instead to preserve capital and ensure consistent income.

Another case might involve a savvy investor who, after a market downturn, spots an opportunity to adjust their RRR upwards, anticipating an eventual market rebound. By recalibrating their RRR in anticipation of this shift, they give themselves the flexibility to capitalize on growth opportunities that arise as the market cycle progresses.

These case studies underline the importance of monitoring both personal financial goals and market conditions. Adapting your RRR over time helps to maintain an efficient and effective investment portfolio that continuously aligns with your risk tolerance and return expectations.

Essential Considerations and Limitations

Factors Influencing the Fluctuation of RRR

RRR doesn’t live in a bubble—it dances to the tune of various external and internal factors that can cause it to fluctuate. One of the headliners in this fluctuation festival is the risk-free rate, which often finds its groove based on government bond yields; when these shift, so does the baseline for RRR. Similarly, the market risk premium can get the RRR moving, as it adjusts for the expected excess return from the overall market compared to risk-free assets.

Investment-specific risks also lead the conga line, influencing the RRR based on company performance, industry stability, and even geopolitical events that could alter the landscape. Expect to see changes in RRR due to inflation projections as well, since the purchasing power of future income streams is paramount.

Macro-level rehearsals include economic indicators and market volatility, both of which can cause strategic pivots in RRR as they forecast the climate in which investments will either bask or shiver. Investors’ risk appetites often change with life stages and financial goals; hence their RRR adjusts to maintain a harmonious risk/return balance.

In essence, the RRR isn’t set in stone—it’s a living, breathing part of your investment process that mirrors the dynamic nature of the financial world, allowing you to skate to where the puck is going to be, not where it has been.

Recognizing the Constraints in RRR Calculations

While the RRR provides a numerical beacon for aiming your investment decisions, it’s not without its constraints and challenges that may obscure its guiding light. The subjective nature of risk assessment plays a prominent role here; investors with different appetites and stomachs for risk will calibrate their RRR differently, even when looking at the same investment. Your personal threshold for what constitutes an acceptable risk can tint your RRR calculations in a unique hue.

Moreover, RRR calculations often rely on models like CAPM, which come bundled with their own assumptions about market behavior, such as efficiency and the distribution of returns. These assumptions, more often than not, are simplifications of a far more complex reality.

Historical data is a major ingredient in calculating RRR, and while looking backward can teach valuable lessons, it’s also true that history doesn’t always predict the future. This reliance could lead to RRR estimates that don’t quite catch the nuances or forward thrust of market dynamics. Let’s not forget that market volatility and liquidity issues can further toy with RRR calculations, making them a moving target rather than a steadfast rule.

In light of these constraints, it’s important to handle RRR calculations with a mixture of mathematical rigor and a dash of humility, acknowledging that numbers only tell part of the story.

FAQs about the Required Rate of Return

What is the meaning of RRR?

The Required Rate of Return, or RRR, is the minimum return that an investor expects to achieve on an investment, considering the risk involved. It’s essentially the threshold of profitability that justifies the investment’s risk.

The required rate of return (RRR) is a critical metric in finance, used to evaluate whether an investment is worth pursuing. It incorporates several factors, such as liquidity risk, risk tolerance levels, and the risk premium accounts to ensure accurate asset valuation. The RRR is often calculated using a valuation model, which takes into account the treasury rate as a risk-free baseline and adjusts it for market-specific risks. This forms the foundation for discount rate calculations that are crucial in determining the present value of future cash flows. Stakeholders and investors use RRR to guide decision-making, particularly in equity valuation and when assessing listings in the marketplace.

While the RRR provides valuable insights, it is not without its drawbacks. For instance, the assumptions underlying value calculations, such as expected returns and sensitivity to market conditions, may lead to inaccuracies. Additionally, the RRR might not fully account for qualitative factors, leaving room for misjudgment in decision-making. However, by leveraging tools like Excel and consulting resources such as Investopedia, investors can improve the accuracy of their RRR estimations. The bottom line is that a well-calculated RRR helps in aligning investments with individual or institutional risk tolerance levels while ensuring that the dividend amount or return potential justifies the associated risks.

What Determines a Good Required Rate of Return?

A good Required Rate of Return depends on individual risk tolerance, investment duration, inflation, and the performance of market benchmarks. It should exceed the risk-free rate and account for the investment’s risk level.

How Can Investors Use RRR to Enhance Portfolio Performance?

Investors can use RRR to enhance portfolio performance by selecting investments that meet or surpass their RRR, ensuring a good balance between risk and return, and aiding in diversification decisions.

Can the Required Rate of Return Evolve with Market Conditions?

Yes, the Required Rate of Return can evolve with market conditions as it reflects risk appetite and factors such as economic climate, interest rates, and market volatility. It needs regular reassessment.

Is It Possible for the Required Rate of Return to Be Negative?

While theoretically possible, a negative Required Rate of Return is highly uncommon since it implies an investor is willing to accept a guaranteed loss, a scenario most investors would naturally avoid.

What is the equation for the required rate of return?

The equation for the Required Rate of Return (RRR), which is paramount in assessing the compensation an investor demands for the riskiness of their stock investment, is typically calculated using the Capital Asset Pricing Model (CAPM). This formula is: RRR = Risk-free rate (Rf) + Beta x (Equity risk premium), where the equity risk premium represents the additional return expected over the risk-free rate. The CAPM’s use of beta provides a measure of the riskiness of a security relative to the market.

Can you provide an example of finding the required rate of return?

Certainly, if an investor is considering a stock with a beta of 1. 2, reflecting its riskiness relative to the market, and the current risk-free rate (return rf) is 2%, while the expected market return is 8%, then by applying the Capital Asset Pricing Model (CAPM), one can calculate the required rate of return (RRR) for this stock. Here’s the formula:

RRR = return rf + beta (market return – return rf) = 2% + 1.2 (8% – 2%) = 9.2%.

This RRR calculation includes the equity risk premium (ERP), which represents the extra yield over the risk-free rate, compensating investors for taking on the additional volatility.