Varieties of Transactions Considered Operating Activities

Operating activities span a diverse range of transactions, each vital in maintaining the business’s core functionality and financial health. These include:

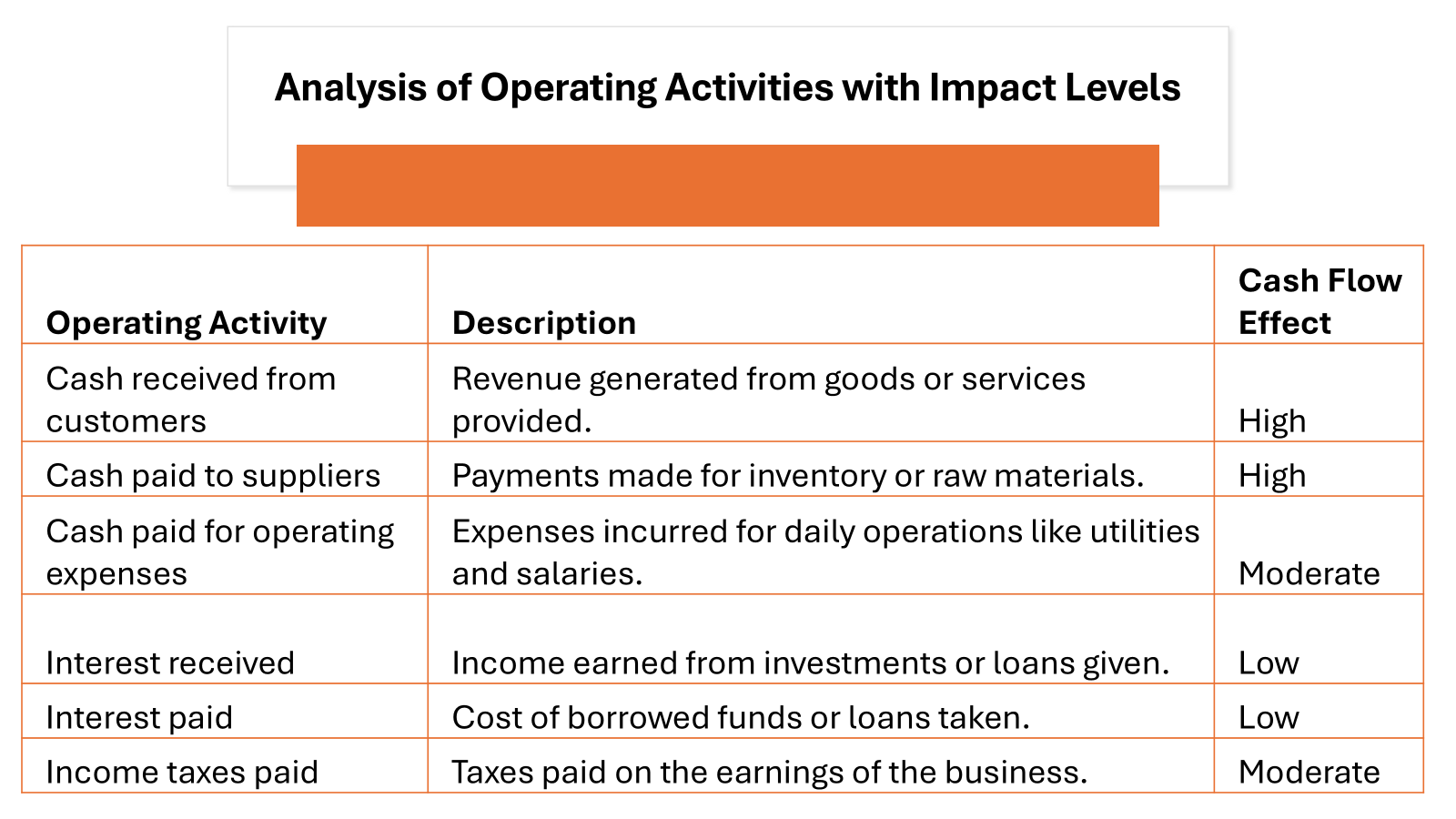

- Sales of goods or provision of services, which stand as the primary source of revenue for businesses across sectors.

- Acquisition of inventory necessary for retailers and manufacturers to continue selling goods. A retail store, for example, might focus on buying the right mix of products to meet consumer demand.

- Payments to employees, pivotal for running the operations smoothly and maintaining an efficient payroll system.

- Payment to suppliers and service providers which ensures that the business does not run out of the resources it needs to operate; it’s essential to maintain good relationships with vendors to secure favorable terms.

- Collection of payments from customers, confirming that revenue is not only recognized but also received.

- Payments of taxes and interest, a legal obligation and the cost of borrowing capital respectively, both imperative to keep the business going without hiccups.

Each of these transactions directly impacts the net cash position from operations, which is critical for assessing the overall financial health of the company.

KEY TAKEAWAYS

- Operating activities are the core activities of a business that generate revenue and include processes such as manufacturing and selling goods in a manufacturing business, buying and re-selling goods in a retail business, and selling and providing services in a service-oriented business.

- Cash flows from operating activities are vital for determining the net income (loss) of a company and are reported in both the income statement and the statement of cash flows; they consist of inflows like revenue from sales and interest income, and outflows such as payments to employees, suppliers, and for interest and taxes.

- The health of a company’s operating activities, reflected in its operating cash flows, is crucial for assessing the entity’s going concern status; persistent negative operating cash flows might signal financial distress, whereas positive operating cash flows indicate good financial performance and potential for growth and reinvestment.

Deciphering Operating Activities through Real-world Examples

Revenue-Generators: Sales and Services

Revenue generation is at the core of any thriving business model, and it primarily flows from two sources: sales and services. Businesses that deal in products, from marketplace platforms to brick-and-mortar retail stores, rely on their sales as their major income stream. Whether they’re selling electronics, clothing, or cars, each unit sold contributes to the overall revenue picture. This process often involves careful stock management and competitive pricing strategies to ensure profitability in the buying and selling exchange.

On the other side, services define the revenue for enterprises like law firms, marketing agencies, or consultancy services, where the offering is centered on expertise and labor rather than physical goods. Many businesses leverage a mix of both, providing a synergistic model that balances the tangible and intangible. For instance, a tech company may sell devices but also offer support and maintenance services — aligning operating activities with the demands of dynamic market trends and customer needs.

These two revenue streams are critical because they represent not just the company’s ability to engage in constant buying and selling but also the firm’s skills in optimizing both product offerings and service solutions. This duality is a crucial indicator of sustainability and growth potential.

Necessary Evils: The Outflows that Keep Businesses Running

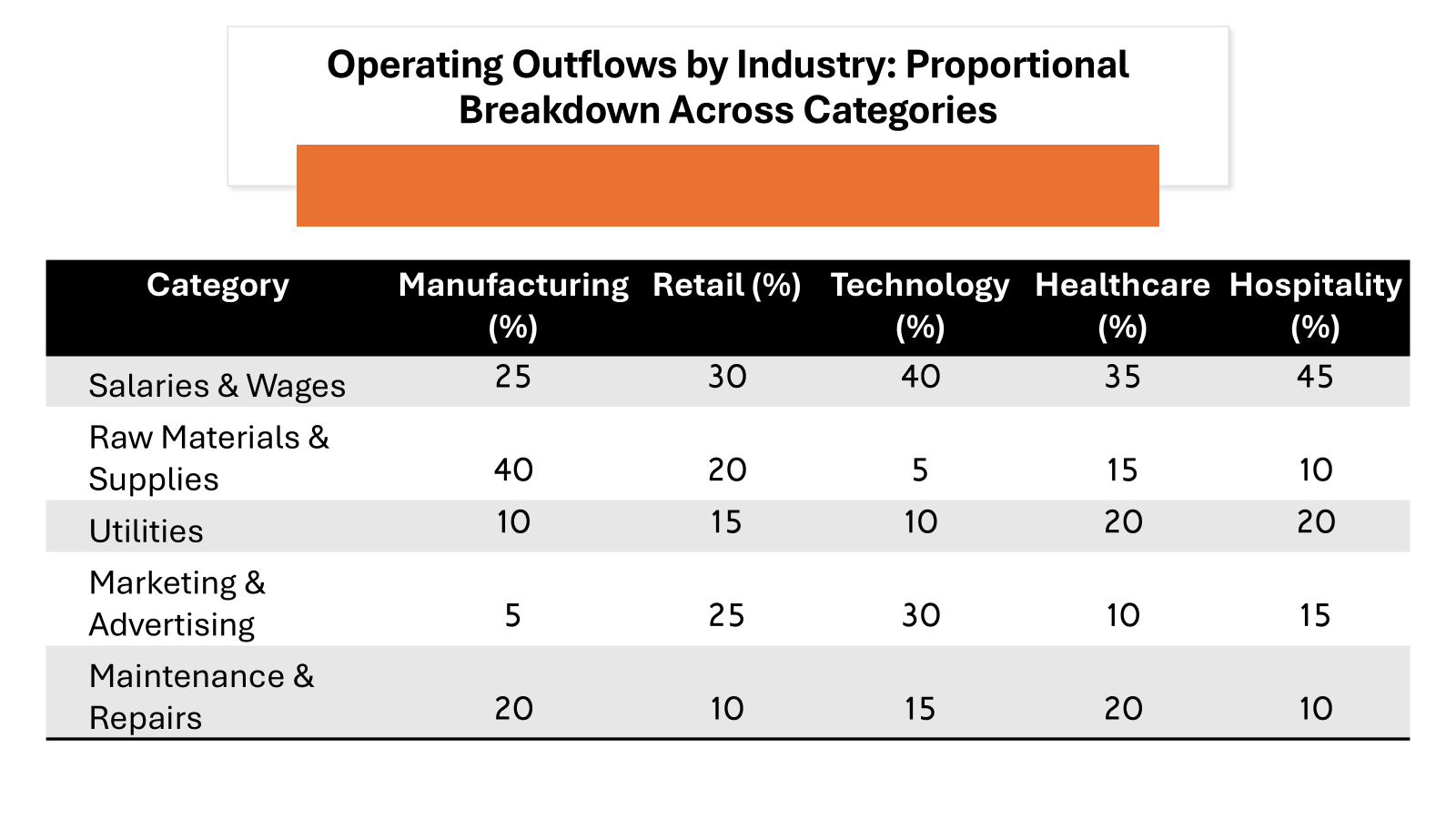

While cash inflows are celebrated, outflows are the ‘necessary evils’ of business operations that are needed to keep the wheels turning. They may not boost the bank balance, but without them, businesses wouldn’t be able to sustain their operations. These cash outflows include:

- Salaries and wages paid to staff, which are essential for maintaining a motivated and productive workforce. Effective payroll management can also contribute significantly to staff satisfaction and retention.

- Payments made to suppliers for raw materials without which products can’t be produced, or services can’t be rendered.

- Rent and utility bills, which are unavoidable as they pay for the physical space and utilities needed to operate.

- Tax payments and interest on debt, which are non-negotiable as they comply with legal obligations and facilitate debt repayment, a critical aspect of maintaining a company’s credit standing.

These outflows are critical in the cycle of business operations, ensuring that all gears are greased and functional, paving the way for generating the next wave of cash inflow. Balancing these outflows, including payroll and repayment obligations, with inflows is what keeps businesses solvent and financially healthy.

Calculating the Lifeblood: Methods to Measure Cash Flow from Operations

Navigating the Direct Method

Navigating the Direct Method in calculating cash flow from operating activities not only involves a detailed analysis but also the classification of all cash-based transactions according to the format prescribed by the “Statement of Cash Flows (Topic 230)“. This method involves tracking the actual cash that enters and exits a business, giving a transparent view of its liquidity. The steps include:

- Listing all cash receipts from customers, representing the sales revenue portion of the operating activities format essential for evaluating a company’s revenue generation.

- Detailing cash payments to suppliers and employees, giving a clear picture of the largest cash outflows, which is integral for analyzing a business’s expense bearing capacity.

- Recording cash paid for operating expenses, which can help identify areas to optimize spending.

- Including cash paid for interest and taxes, which are mandatory components of operating activities and essential for staying in good standing with creditors and the government.

- Noting any other cash received or paid that’s related to operating activities, ensuring a comprehensive calculation that adheres to the classification standards of the financial statements.

By applying the correct format in adding up all these cash movements, businesses ascertain the net cash from operating activities. Although more accurate, the Direct Method is less commonly used due to its complexity and the extensive record-keeping required.

Expertise of the Indirect Method

Command of the Indirect Method for calculating cash flow from operating activities is a skill vital for businesses, especially for those using accrual-based accounting. To apply the indirect method, one starts with the net income from the income statement and makes the necessary adjustments to arrive at the cash flow from operations. Here’s a streamlined guide:

- Begin with net income as reported on the income statement, which represents the company’s profitability.

- Adjust for non-cash expenses, such as depreciation and amortization. Since they don’t involve actual cash outflow, these are added back to the net income.

- Account for changes in working capital by examining the shifts in accounts receivable, inventory, accounts payable, and accrued expenses. These changes are crucial as they reflect the cash that is either consumed or released by everyday operational transactions.

- Compile the adjusted net income using the formula: Cash Flow from Operating Activities = Net Income + Adjustments for Non-Cash Items + Changes in Working Capital.

- Explore the financing section, where you analyze the cash flow from financing activities section to understand the business’s capital structure changes, such as equity or debt financing.

The summation of the adjusted net income and the changes in working capital will provide an insight into the actual operational liquidity. The Indirect Method is favored for its simplicity and connection to traditional financial statements, making it easier for stakeholders to see how net income translates into actual cash flow.

The Significance Unveiled: Impact of Operating Activities on Business Health

The financial health of a business is inextricably linked to its operating activities, a clear reflection of how well the company is managing its daily business practices to generate cash flow. Positive cash from operating activities indicates that a company is able to sustain and grow its operations internally, without resorting to financing activities such as the issuance of stock or seeking additional investors through the proceeds from bonds. A consistent generation of cash from operations points towards:

- A strong market position, suggesting that the company’s goods or services are in demand.

- Efficient operational management, signifying that the company maintains control over its costs and cash cycle.

- Financial stability and independence, showing that the company is less reliant on external financing to fuel growth.

- The ability to reinvest in the business, whether for expansion, innovation, or improving infrastructure, without necessarily tapping into the financing activities section of cash flows.

- Resilience during economic downturns, as companies with strong operating cash flow are better positioned to weather periods of uncertainty and do not have to depend solely on external financing activities.

For potential investors and creditors, healthy cash flow from operating activities reassures them of the company’s viability and profitability, fostering confidence for future endeavours and negating heavy reliance on the issuance of new stock or taking on debt to maintain solvency.

Comparing and Contrasting: Operating vs. Other Types of Activities

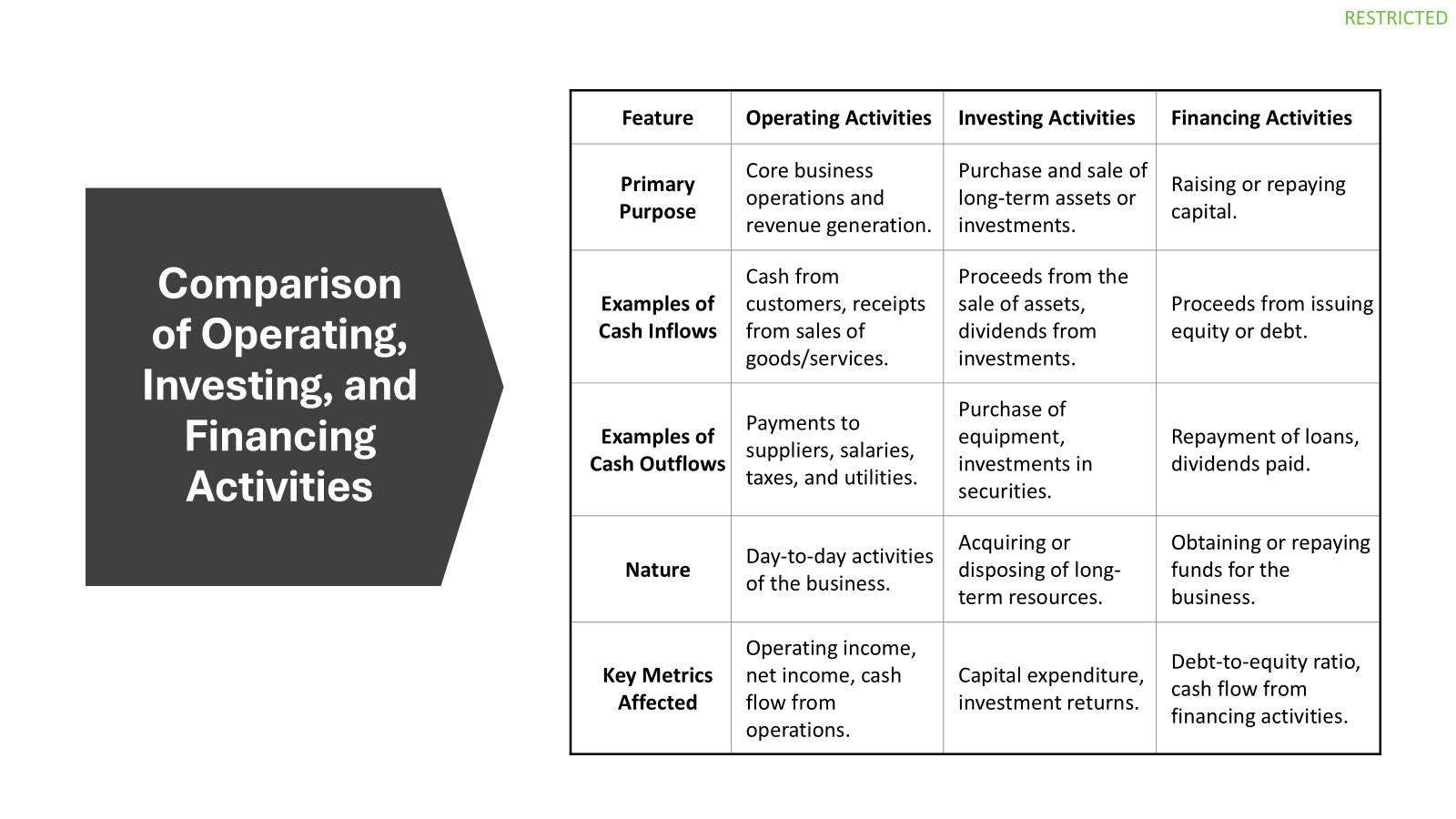

When comparing operating activities with other types of business activities, namely investing and financing, it’s like comparing the heart, brain, and muscle of a company. They all have distinct roles but are essential for survival and growth.

Operating activities are akin to the heart, pumping the lifeblood which is cash through the business on a daily basis. They are associated with the principal revenue-producing activities of the company.

Investing activities represent the brain, where the company’s future growth and expansion are strategized. This includes the purchase and sale of long-term assets and other investments not included in cash equivalents.

Financing activities are the muscle, providing the strong support needed for the company’s structure and operations. They entail transactions that involve receiving capital from or returning capital to shareholders and creditors, such as issuing stocks or taking on loans.

While operating activities track the cash flow within the core business dynamics, investing activities give insight into the company’s growth strategy and financing activities outline how the company funds its operations and manages its capital structure. Balancing all three is crucial for a company’s long-term success and stability.

Beyond Theory: Case Studies and Examples

Journey Through a Retail Giant’s Cash Flow Statement

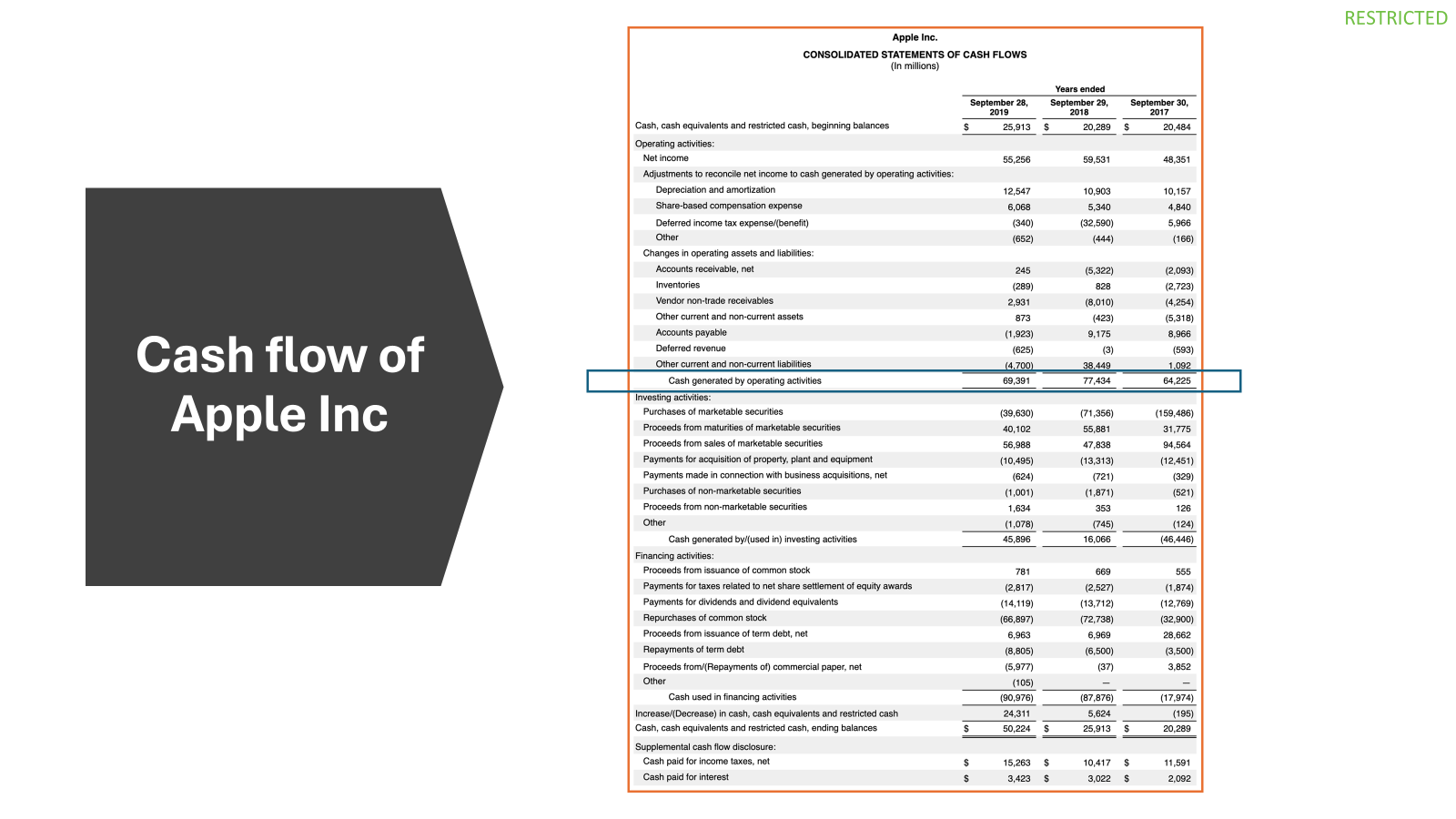

Let’s take a hypothetical retail giant, “SuperStore Inc. ,” and trace their journey by analyzing their cash flow statement. SuperStore Inc., much like real-world retail leaders such as warehouse giant Costco or Walmart, provides a snapshot of how operating activities propel its cash flow.

- Net Income: The starting point reflects SuperStore Inc.’s profitability after all expenses—in a retail store, this would also include costs relating to store maintenance and inventory management.

- Adjustments: Here, non-cash expenses like depreciation are added back in, as they don’t affect the cash—key for a business with significant physical assets such as a warehouse or a large number of retail locations.

- Changes in Working Capital: The cash flow effects of inventory changes, accounts receivable, and accounts payable are considered, essential for retail operations where inventory turnover is a sign of efficiency.

- Net Cash from Operating Activities: This is the culmination of the aforementioned steps, showcasing the actual cash that SuperStore Inc. generated from its core operations.

Looking at SuperStore Inc.’s cash flow from operations, one can discern how effective they are at selling goods and managing their inventory, supplier payments, and collections—crucial aspects in both the retail store and warehouse settings for covering expenses and fueling expansion.

A Service-Based Startup’s Path to Positive Operating Cash Flow

Imagine a budding service-based startup, “Innovate Solutions,” beginning its journey in the competitive tech industry. Tracking Innovate Solutions’ path to positive operating cash flow unveils a story of strategic management, adaptability, and keen attention to their financing section on the cash flow statement. Initially, Innovate Solutions might have struggled with cash outflows for salaries, rent, and business development efforts exceeding the slower inflows from their service contracts. But as they refined their service offerings and improved their client acquisition strategy, their cash receipts began to climb.

They focused on quickening the turnover of their accounts receivables, ensuring timely customer payments. This move, strategic in affecting the cash flow from operating activities, steadily projected them towards financial stability. Innovate Solutions also optimized their operational expenses, such as negotiating better terms with suppliers or automating certain tasks to reduce labor costs. Through meticulous attention to operating efficiency, they tweaked their business model until the cash flowing in from their services consistently surpassed their operational spending, marking their successful path to a sustainable positive cash flow.

FAQ: Everything You Need to Know About Operating Activities

What Defines an Activity as an ‘Operating’ One?

An activity is considered ‘operating’ if it’s central to the primary business activities of a company—basically, anything that has to do with producing and delivering the company’s goods or services. From selling products to paying the rent for the office space, if it’s a transaction necessary for the day-to-day running of the core business, it’s an operating activity. These activities are essential for maintaining the business’s earning power and are reported in the cash flow statement under operating cash flow.

How Can a Company Improve its Cash Flow from Operating Activities?

To enhance its cash flow from operating activities, a company can focus on increasing revenue and managing expenses more effectively. By optimizing revenue through measures that may involve reviewing pricing strategies and exploring new markets or product lines, firms can greatly impact their operating cash flow. Similarly, on the expenditure side, improving inventory turnover and streamlining operations to reduce costs, along with negotiating better payment terms with suppliers, can be key moves. Companies should also engage in rigorous follow-ups on receivables to accelerate cash collections, possibly negotiating quicker payments or even refunds from suppliers. Ensuring efficient capital expenditures by setting appropriate capitalization thresholds helps in preventing unnecessary depletion of resources.

Why is cash flow from operating activities important in financial analysis?

Cash flow from operating activities is crucial in financial analysis as it provides a clear picture of the liquidity and day-to-day financial health of a company. Considering factors like depreciation, changes in current assets and liabilities, and other adjustments, this measure is more indicative of a company’s financial resilience. For instance, an increase in liabilities such as accounts payable or accrued expenses may inflate the cash flow from operating activities, showing more cash at hand than net income alone would suggest. This measure reveals whether a company can generate enough positive cash flow to maintain and grow its operations without relying on external financing. Financial analysts consider cash flow from operating activities a more reliable indicator of a company’s economic stability than net income alone, as it accounts for actual cash transactions rather than non-cash accounting entries.

What are the three types of cash flows?

The three types of cash flows presented in the statement of cash flows are operating, investing, and financing activities. Operating activities involve the cash inflows and outflows directly related to the production and delivery of the goods and services your business trades in. This includes everyday transactions like employee salary payments, interest expense to creditors, and the revenue from the sale of goods and services.

Investing activities, on the other hand, pertain to the purchase and sale of long-term assets or investments. These transactions could range from acquiring plant, property, and equipment to proceeds derived from selling off some of these fixed assets.

The financing activities section showcases movements in cash related to the company’s equity and debt. Here, you’d see activities such as the issue of stock, the repayment of debt, and importantly, dividends paid to shareholders. These actions speak volumes about a company’s capital structure strategy and overall financial sustainability.

Each category within the statement of cash flows provides crucial insights into different aspects of a company’s financial health and performance, shining a light on its operational efficiency, investment acumen, and financing prowess.