What’s more, the NCI is more than a mere entry: it signifies the value attributed to subsidiary shareholders outside of the majority interest. Thus, it effectively delineates the true proportion of assets and liabilities attributable to the parent entity, painting a clear picture of ownership stakes and earnings distribution for analysts and investors alike.

KEY TAKEAWAYS

- Non-controlling interest (NCI) arises when a parent company does not fully own a subsidiary, resulting in the need to identify and calculate the ownership percentage of external partners who have a stake in the subsidiary’s income and book value.

- It is essential to accurately calculate and report non-controlling interest in the consolidated financial statements, as NCI represents the share of equity and net income attributable to non-controlling partners which is usually presented either as non-current liability or as non-controlling equity under US GAAP or IFRS.

- When dealing with multiple non-controlling interests, subsidiaries with complex ownership structures, foreign currency translations, or disparate general ledgers, utilizing a purpose-built consolidation solution is recommended to ensure proper accounting treatment and to minimize the risk of errors in financial reporting.

The Genesis of NCI: When and How It Arises

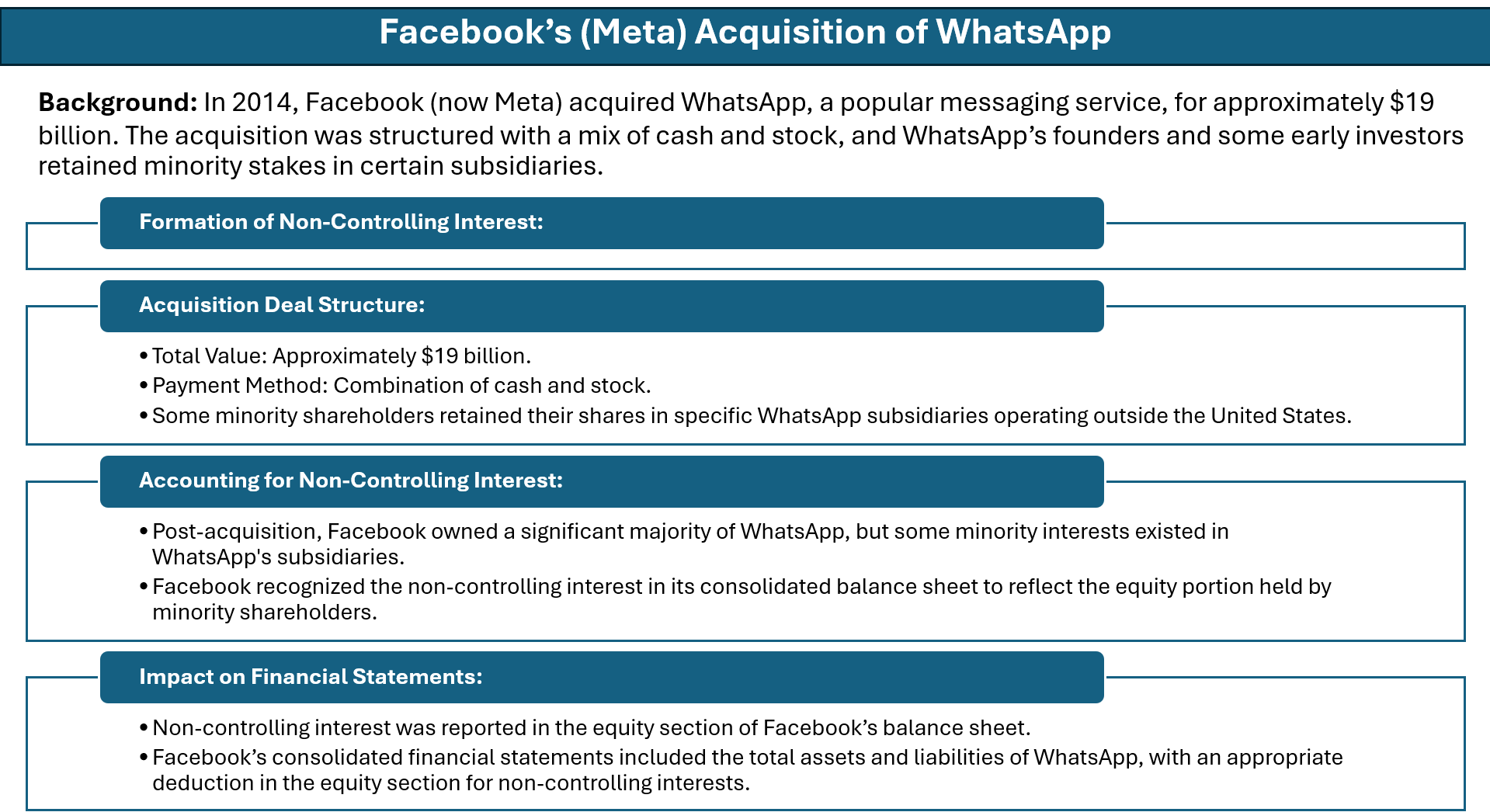

NCI typically comes to life during acquisitions when a parent company snaps up a controlling stake—but not full ownership—of another company. This leaves a portion of the company in the hands of other shareholders, giving rise to NCI. The percentage of ownership that the parent does not hold continues to maintain its separateness and is acknowledged in the consolidated financials as NCI. For instance, when Vodafone acquired a minority interest in Verizon Wireless, it held a significant ownership share yet did not seek full control, reflecting true non-controlling interest dynamics.

It can also arise in joint ventures or associate companies where control isn’t the goal, but significant influence is present. The meticulous dance of corporate control commences when a company purchases a slice of another, and NCI is that delicate line between majority rule and minority rights.

Breaking Down the Accounting Mechanics

Recognizing and Measuring Non-Controlling Interests

Recognizing and measuring NCI is akin to a strategic chess move requiring careful thought and precision. When consolidating financial statements, NCI is recognized as a unique line item within equity, reflecting the ownership stake not held by the parent company. To measure NCI, companies have two choices: they may opt for fair value, which integrates goodwill accounting to encapsulate the full essence of the acquired entity’s worth, or they can measure it based on the proportionate share of the acquiree’s identifiable net assets. It is worth noting that under US GAAP, goodwill accounting always applies, but it’s a policy choice under IFRS. Though the fair value method offers a broader view of the subsidiary’s intrinsic value, the proportionate share approach sheds light on the tangible assets and liabilities pertinent to non-controlling shareholders. Effective purchase price allocation is critical here, as it requires a judicious split of the transaction cost over the acquired portfolio. Accurate measurement of NCI is crucial, as it ensures financial transparency and equitability, providing shareholders a clear depiction of their stakes.

Impact on the Consolidation Process and Financial Reporting

The consolidation process weaves a tapestry of financial data, integrating subsidiary and parent company figures into a single panoramic financial statement. The impact of incorporating NCI into this confluence is significant. Firstly, NCI ensures that the reported equity and net income amounts reflect the reality that a portion of the subsidiary is not under the parent company’s purview. This separation on the balance sheet and income statement offers transparency and a clearer picture of each party’s interests.

Furthermore, NCI affects how changes in ownership levels are accounted for. When a parent entity acquires additional shares or sells a portion of its interest, these transactions create shifts that are captured through equity accounts without hitting the income statement. As for financial reporting, NCI demands careful note disclosures that provide additional color regarding its size, changes, and impact on the overall financial health of the group.

The Valuation Quandary

Challenges in Determining Fair Value of NCI

The great conundrum in NCI accounting lies in pinning down its fair value, a task often rife with challenges. The goal is to capture the exact worth of the non-controlling shareholders’ slice of the pie. However, when market values aren’t readily available—perhaps because the subsidiary is not publicly traded—valuing NCI turns into an intricate puzzle. It may be possible to value NCI by reference to financial data related to the subsidiaries themselves using valuation multiples such as EV/EBITDA or EV/Revenue.

Appraisers may weave together a tapestry of valuations using income-based approaches, like discounted cash flows (DCF), or market comparable, which can be highly subjective and complex. For a more robust framework, some practitioners prefer enterprise value-based analyses, considering them superior for calculating valuation multiples.

Complications further churn around adjustments for control premiums or discounts for lack confidence. Valuations must be finely tuned to consider these nuances, as the value per share held by the parent company might differ from the value per share for NCI due to these factors.

These complexities underscore the importance of rigorous methodologies and disclosure, ensuring that the fair value of NCI communicates a faithful representation of economic realities to users of the financial statements.

Tools and Techniques for Accurate Valuation Practices

Achieving precision in NCI valuation is an art that harnesses various tools and techniques. Professional valuers often turn to the tried-and-true Discounted Cash Flow (DCF) method, which shines a light on the present value of expected future cash flows. For a market-oriented perspective, the Guideline Public Company method considers publicly traded companies that closely match the subsidiary’s profile, offering a comparative valuation canvas.

Other tools like the Cost Approach, which pegs value to the replacement cost of assets, or the Market Approach, akin to valuing a piece of real estate based on neighborhood prices, also come into play. For a closer look at the subsidiary’s own financial journey, the Adjusted Net Asset Method adjusts the balance sheet to fair market values.

Moreover, sophisticated valuation software can help navigate these diverse tools by providing analytical models and real-time market data, ensuring that the numbers crafted are not just estimates, but coherent narratives of value.

Real-World Examples and Case Studies

Navigating Complex Scenarios with NCI Accounting

Navigating the complex scenarios in NCI accounting is like steering through a maze with various pathways and outcomes. H3: Navigating Complex Scenarios with NCI Accounting

Navigating the complex scenarios in NCI accounting is like steering through a maze with various pathways and outcomes. Complexities arise when mergers, acquisitions, or accounting changes in ownership percentages occur. These business maneuvers necessitate re-measurement of existing NCI and can lead to recognition of gain or loss in the parent’s financials, which may not affect the subsidiary’s records. For instance, changes reflecting a shift in equity ownership percentage could realign a company’s investment status from the cost method to the equity method of accounting.

Additionally, when the parent company edges towards acquiring more control, perhaps moving from significant influence to full control, NCI has to mirror these changes convincingly. The accounting treatment pivots substantially, switching lanes from equity method, where ownership percentages might range from 21% to 49%, to full consolidation, with initial and subsequent measurements of NCI demanding sharp judgement calls.

Nevertheless, with a solid grasp of the underlying principles and guidance set forth by accounting standards, one can expertly navigate these complex situations, ensuring accurate and fair representation in the consolidated financial statements.

Lessons Learned from Prominent Corporate Case Studies

Analyzing prominent corporate case studies can be illuminating—they’re like cautionary tales or blueprints for success with real-world implications. For instance, mergers and spin-offs often shine a spotlight on the treatment of NCI, where over- or under-valuation can sway shareholder perception and market reactions. Learning from companies which navigated these choppy waters effectively, with transparent communication and robust accounting practices, offers invaluable insights.

Dissecting blunders where companies faltered in NCI handling could help others steer clear of similar pitfalls. Misaligned valuations or reporting discrepancies not only invite regulatory scrutiny but also rattle investor confidence. Therefore, diving deep into such case studies provides practical verges on the do’s and don’ts of NCI accounting, shaping better practices for the future.

Best Practices and Common Pitfalls

Key Takeaways for Flawless NCI Accounting

For flawless NCI accounting, there are a few key takeaways to keep in mind. One must embrace meticulousness in the initial recognition and subsequent measurement of NCI, carefully distinguishing it from the parent’s equity. Ensuring the use of consistent and appropriate valuation techniques, along with keeping a pulse on the evolving ownership interests, is vital.

A clear understanding of the reporting standards is also crucial, as NCD accounting can be quite nuanced depending on the governing accounting framework. All the while, transparency and disclosure play central roles; providing detail on the effects of NCI in the financial statements helps stakeholders make informed decisions.

Armed with these insights and a thorough approach, one can aim for airtight NCI accounting in their financial statements.

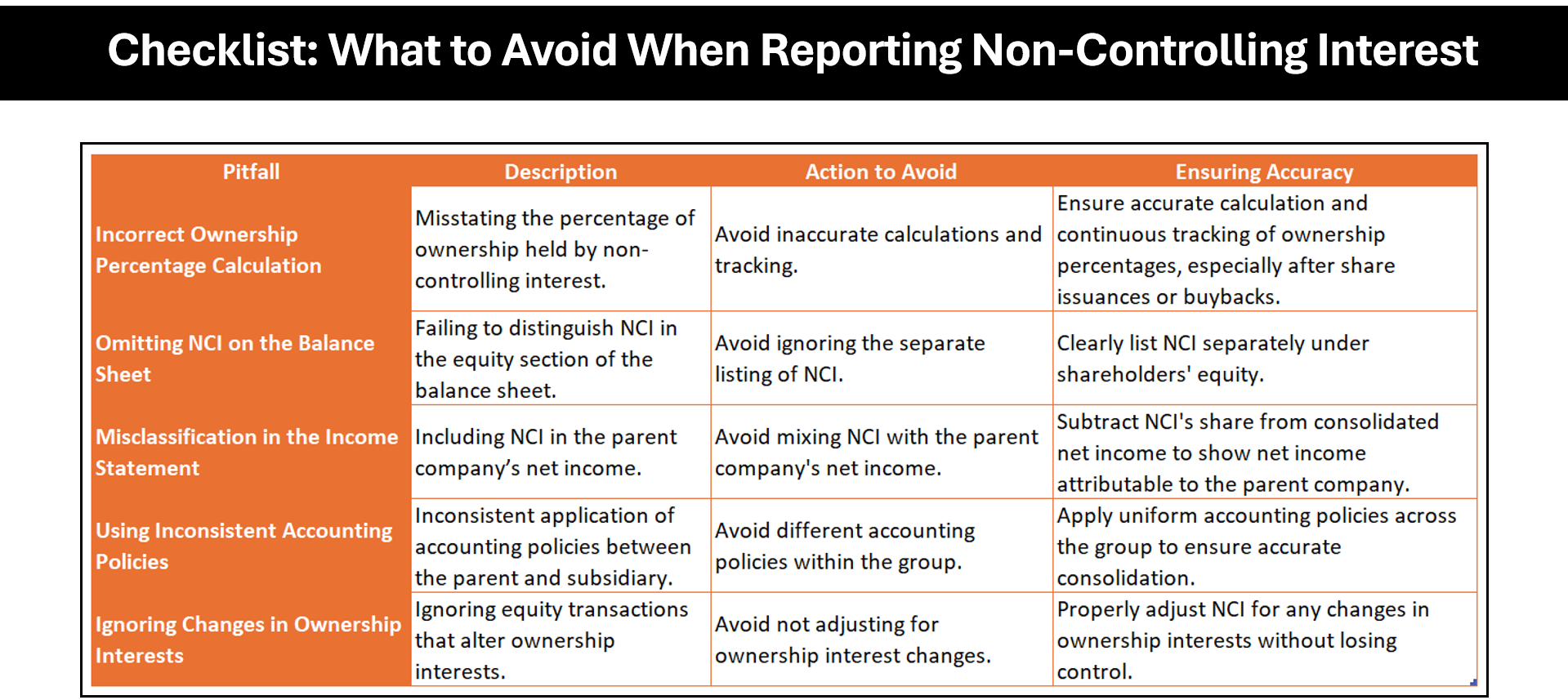

Avoiding Common Missteps in Reporting and Disclosure

When it comes to reporting and disclosure, avoiding common missteps in NCI accounting is crucial for accuracy and compliance. A frequent oversight involves insufficiently detailed disclosures that fail to satisfy the curiosity and needs of stakeholders necessitating clear delineation of NCI in financial statements.

Another common pitfall is the incorrect classification of NCI, either as a liability or within the wrong equity category. Both can lead to misleading interpretations of a company’s financial position. Additionally, inconsistencies in applying the valuation method or failing to update the valuation for significant changes in subsidiary operations can skew the reported NCI.

By staying vigilant and adhering to the proper reporting requirements, such as those detailed in ASC 810 and IFRS 10, entities can steer clear of these common reporting missteps and ensure more faithful financial disclosures.

The Evolving Landscape of NCI Accounting Standards

Staying Ahead of Regulatory Changes and Updates

Keeping up with regulatory changes and updates is like sailing in open waters; one must be watchful of the shifting tides. Regulatory bodies, such as the Financial Accounting Standards Board (FASB) in the U.S. or the International Accounting Standards Board (IASB) internationally, continually refine and issue updates that could impact NCI accounting.

To stay ahead, regular engagement with professional accounting resources, subscribing to updates from standard-setting bodies, or attending industry seminars can be incredibly beneficial. Embracing a culture of continuous learning within an organization helps ensure that when the winds of change blow, they’re navigated with dexterity and knowledge.

By actively monitoring and adapting to these changes, a company can uphold the integrity of its financial reporting and maintain the confidence of investors, analysts, and other stakeholders.

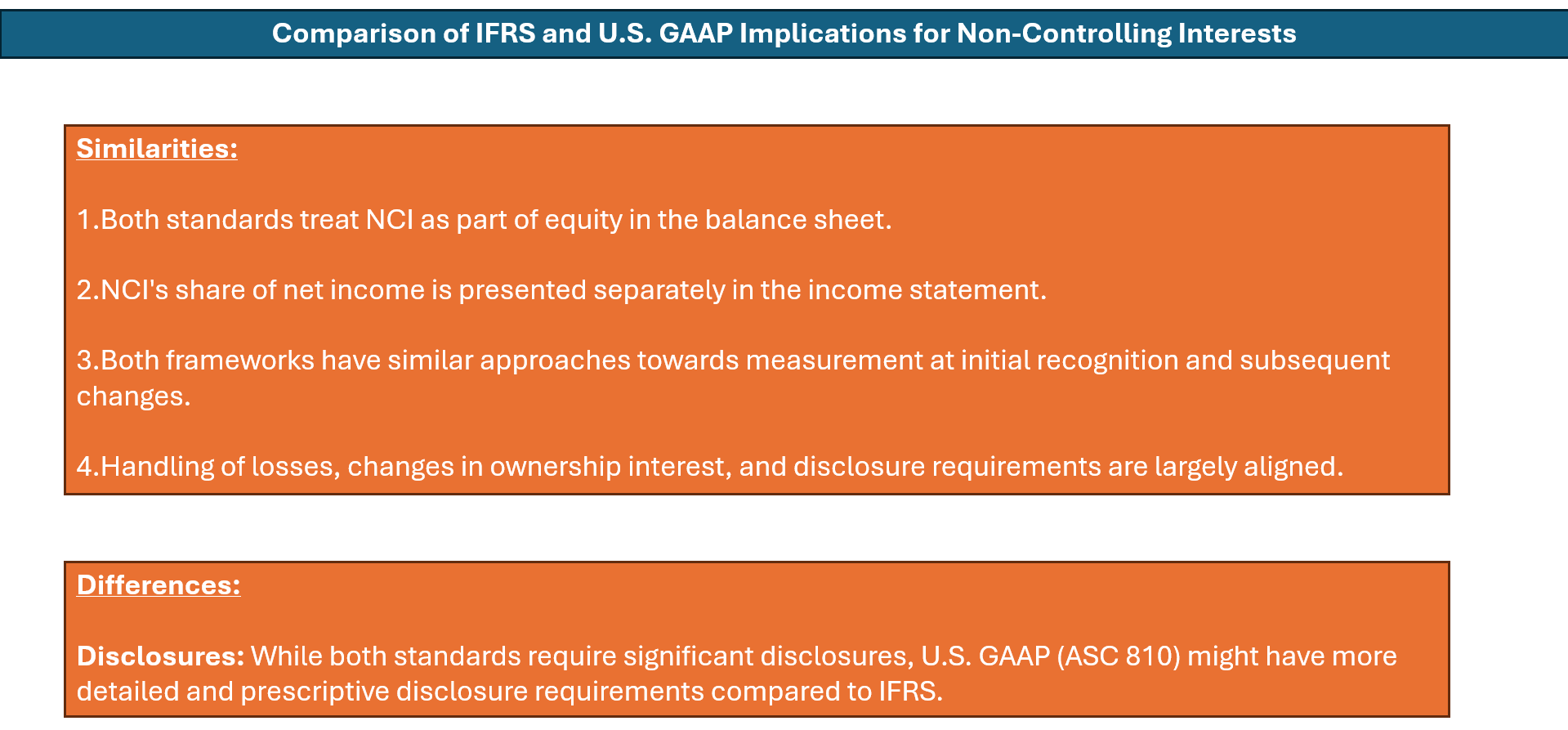

Understanding the Implications for International and U.S. GAAP

Grasping the implications of NCI for both International Financial Reporting Standards (IFRS) and U.S. Generally Accepted Accounting Principles (GAAP) is key to harmonizing global accounting practices. While the essence of recognizing and measuring NCI is shared across both standards, the devil is in the details.

Under IFRS, for instance, NCI is measured either at fair value or at the non-controlling interest’s proportionate share of the subsidiary’s identifiable net assets. In contrast, U.S. GAAP mandates the use of the latter approach. These subtle distinction influence how acquisitions and disposals involving NCI are recorded and can result in different figures being reported under the two frameworks.

By understanding these nuances, accountants and finance professionals can ensure compliance with the appropriate standards, facilitating cleaner audits and smoother interactions with international stakeholders.

FAQs on Non-Controlling Interest Accounting

What Exactly Constitutes a Non-Controlling Interest?

Non-Controlling Interest (NCI) refers to the ownership stake in a subsidiary that is not owned by the parent company – typically, when the parent owns more than 50% but less than 100%. NCI shareholders have a claim to a portion of the subsidiary’s earnings and assets yet do not hold controlling power.

How Is NCI Reflected on the Income Statement and Balance Sheet?

On the income statement, NCI is presented as a deduction from consolidated net income to arrive at the net income attributable solely to the shareholders of the parent company. On the balance sheet, it is shown within equity, separate from the parent’s equity, reflecting non-controlling shareholders’ claim on the subsidiary’s assets.

Can You Explain the Differences Between NCI and Minority Interest?

NCI and minority interest essentially refer to the same concept but from different vantage points. ‘Minority Interest’ is an older term that focuses on the ownership percentage that is less than a majority stake, while ‘NCI’ emphasizes the lack of control despite ownership. Both represent the equity stake in a subsidiary not held by the parent company.

What Are the Typical Challenges Faced During NCI Valuation?

Valuing NCI can be challenging due to the lack of market value for non-public entities, determination of discounts for lack of control, and projecting future profitability and cash flows especially when there is limited financial information available from the subsidiary.

Where Can I Find Reliable Resources for Deepening My Understanding of NCI Accounting?

Reliable resources for NCI accounting include official documentation from the FASB and IASB, accounting textbooks, reputable online accounting platforms, and professional accounting organizations offering webinars, courses, and publications on the subject.