KEY TAKEAWAYS

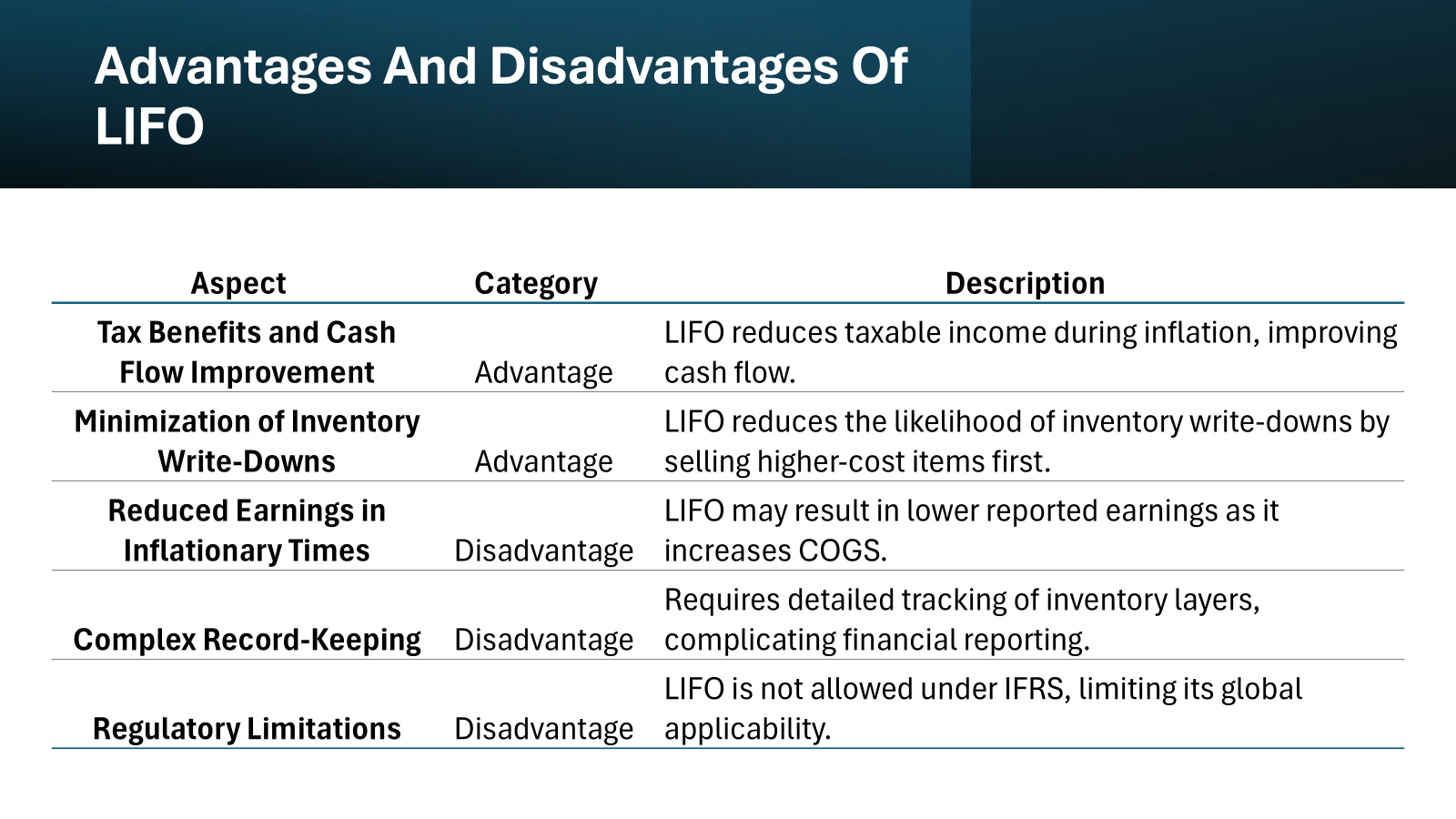

- The LIFO (Last-In, First-Out) method assumes the most recently purchased or produced items are sold first, which typically leads to a higher cost of goods sold (COGS) and thus, reduces taxable income, potentially resulting in significant tax savings for businesses.

- By using the LIFO method, companies can better match current costs with revenues, as it reflects more recent inventory costs in the COGS calculation when prices are rising due to factors like inflation.

- Though LIFO can offer financial benefits, it also comes with drawbacks such as potentially distorted profit reporting and intricate accounting requirements, meaning businesses must weigh the pros and cons and understand the implications of adopting this inventory valuation method.

Basics of Last-In, First-Out Methodology

The Last-In, First-Out methodology is all about the sequence in which inventory costs are accounted for. When companies make sales, they use the cost of their most recent inventory purchases or productions as the basis for COGS. This is underpinned by the assumption that the newest items are the first to leave the warehouse when sales are made.

Imagine a stack of boxes, with each box representing a batch of goods received at different times. In LIFO, you’d be removing boxes from the top of the stack first, which are your most recent acquisitions.

An advantage of this methodology is its relevance in times of price inflation. When prices are rising, selling the most recently acquired inventory first matches the latest costs against current revenues, which can result in a lower taxable income due to the higher COGS.

The Mechanics of LIFO Accounting

Illustrating LIFO with Real-World Examples

To truly grasp how LIFO functions in practice, consider a bakery that buys flour each month at varying prices due to market changes. In January, they buy 10 bags at $30 each, but by June, the price has risen, and they purchase 10 more at $45 each. If they bake bread in July, under LIFO, they would use the cost of the June flour bags ($45) to calculate their cost of goods sold, not the January batch.

Another example would be a fuel company that stores fuel in large tanks. As they refill the tanks with new fuel at prevailing market rates, they’ll dispense the most recent addition to consumers. If fuel prices are climbing, the cost attributed to the fuel sold is based on the latest, more expensive supply.

These scenarios highlight one of LIFO’s critical features: aligning the cost of goods sold with the most recent market prices. This can be particularly potent during inflationary periods when costs are rapidly increasing.

Step-by-Step Breakdown: How to Calculate COGS Using LIFO

Calculating COGS using LIFO might seem daunting, but when you break it down, it’s quite straightforward. Whether you’re a small business owner or an accounting student, you’ll find these steps to be practical and easy to apply.

- Identify Recent Purchases: Begin by pinpointing which inventory items you’ve most recently acquired. These will form the basis for the COGS calculation.

- Track Sales and Usage: Maintain an accurate record of how many units you’ve sold over the period. Details are crucial; you’ll need both the quantity and cost at the time of each sale.

- Assign Costs to Sold Items: When a sale is made, allocate the cost of the newest inventory to those sold items, working your way back through the most recent purchases until each sold unit is accounted for.

- Calculate Total COGS: Tally up all the costs you’ve assigned to the sold units during the period. The sum will give you your COGS figure according to the LIFO method.

- Update Inventory Values: After the COGS are computed, adjust your inventory balance to reflect the costs of the older inventory that remains. These costs sit in the balance sheet until these older items are sold.

Remember, this method focuses on recent costs, which can help your business align with current market conditions amid inflation.

LIFO’s Influence on Business Finances

Tax Implications and Benefits Under LIFO

When you employ LIFO, you could find a silver lining in its tax implications, especially during inflationary periods. Since LIFO lets you record the latest, often higher, inventory costs against your sales, you typically end up reporting a lower profit margin. This might not sound ideal initially, but in the eyes of the tax authorities, lower profits translate to a lower tax bill, ultimately easing your tax burden.

In essence, the Internal Revenue Service will tax a smaller portion of your income because your expenses (the cost of goods sold) appear higher. This strategy can be particularly beneficial for companies experiencing rapid price increases for their products or raw materials.

LIFO Impact on Cash Flow and Net Income

The manner in which LIFO influences your cash flow and net income can’t be overstated. By assigning the most recent—and typically higher—costs to COGS, LIFO effectively lowers net income during inflationary periods. This might seem like a setback, but there’s a financial perk: because you’re taxed on net income, a lower profit on paper means you’re paying less in taxes now. This deferral frees up cash flow, giving you more liquid capital to reinvest in your business or cover other expenses.

However, while LIFO can spruce up cash flow short-term, it’s essential to understand that this accounting method may depict a less robust picture of your financial health than reality, as it reports systematically lower earnings over time.

Situations Favoring the LIFO Method

Advantages During Inflationary Periods

When inflation hits and costs start to climb, the LIFO method shines. It adeptly matches your current costs of purchasing or producing goods with your revenues. This means that the COGS on your financial statements reflects the higher prices you’re currently paying, rather than those of cheaper, older inventory which FIFO might use.

This alignment doesn’t just give you a realistic snapshot of your expenses; it also tactically lowers your taxable income by increasing your COGS. In doing so, it positions your business to retain more cash in-house during these challenging economic times, cash that’s pivotal for maintaining operations or investing in growth opportunities.

Matching Current Costs with Revenue

The beauty of LIFO lies in its ability to sync up your costs with your revenue, essentially by making sure the price you’re paying for inventory today is set against the revenue from sales happening now. This approach is especially beneficial in a changing economy, as it helps you assess profitability in the current fiscal landscape, not by the standards of yesteryear’s prices.

By doing so, LIFO provides you with a more accurate and current cost of sales, allowing for a better understanding of true profit margins during periods of shifting prices. It’s an honest and transparent way to present your financial situation to stakeholders, making clear how the business performs under the latest economic conditions.

Controversies Surrounding LIFO

Why LIFO is Not Universally Accepted

While LIFO can be a savvy choice for some businesses, it’s not globally embraced, primarily due to concerns about its reflection of true inventory costs. Under the International Financial Reporting Standards (IFRS), LIFO is prohibited because it can lead to an outdated valuation of inventory, potentially skewing a company’s financial health.

Furthermore, LIFO’s advantages are usually inflation-dependent. In a stable or deflationary economic environment, LIFO’s benefits may wane, and the method could even disadvantage a business financially.

Since IFRS is used by a vast majority of countries, businesses operating internationally often avoid LIFO to maintain consistent financial reporting standards across borders, opting instead for methods like FIFO which are more universally accepted.

The Great LIFO vs. FIFO Debate

The LIFO versus FIFO debate is a classic in accounting, with staunch proponents on each side. FIFO proponents argue that it better matches the actual flow of inventory for most businesses, keeping balance sheet values up-to-date with the market. LIFO supporters, on the other hand, stress its tax benefits and how it matches current costs with revenues, which can be a boon during inflationary times.

Still, FIFO is often seen as more straightforward and less likely to complicate a company’s financial picture. Yet, when prices are on the rise, LIFO’s appeal grows as it can markedly reduce tax liabilities and align bookkeeping with current economic reality.

Deciding between LIFO and FIFO isn’t just an accounting preference—it’s a strategic choice that impacts a business’s financials and tax liabilities, and each method carries its implications for financial reporting and operational management.

Conclusion

The Last-In, First-Out (LIFO) inventory method is a widely recognized accounting strategy for managing inventory. It operates on the principle that the most recently purchased or produced items are sold or used first, leaving the older inventory costs to remain on the books. This approach is particularly beneficial in industries like electronics, auto dealerships, and sectors affected by rapid price fluctuations.

Implementation in Different Sectors

In regions such as Greater Richmond, businesses utilize LIFO for accurate inventory management systems, particularly where cost control is critical. Industries like electronics and retailers gain from this system as it aligns well with managing inventory write-downs and improving gross income calculations. Countries like Russia and Japan, which deal with high levels of inventory quantities, also adopt LIFO to mitigate the effects of inflation on reported profits.

Cost and Valuation Systems

LIFO plays a crucial role in cost accounting purposes by aligning costs with revenues in an inflationary environment, helping businesses avoid the understatement of costs. Coupled with an effective valuation system, LIFO ensures businesses can maintain compliance with accounting rules and standards. This is particularly useful during audits, as it ensures transparency and accurate documentation of closing inventory metrics.

Strategic Benefits and Considerations

For industries dependent on inventory turnover, like marketplaces, LIFO helps in addressing inventory obsolescence by accounting for the most recent purchases. It also facilitates better financial planning by incorporating LIFO equations for detailed tax calculations, especially in sectors like business taxes and government data reporting. However, adopting LIFO comes with its complexities, requiring skilled advisors to manage the intricate calculations and ensure compliance.

The adoption of LIFO has significant implications for managing inventories in diverse environments. Whether it’s tackling challenges in inventory turnover management or leveraging benefits for gross profit calculations, LIFO stands out as a method tailored for tax LIFO calculations and aligning with modern-day business needs. With careful implementation and a focus on transparency, businesses can achieve operational efficiency and financial clarity.

FAQs

Is LIFO Legal and Where Is It Prohibited?

LIFO is perfectly legal within the United States and is fully supported under the Generally Accepted Accounting Principles (GAAP) which govern accounting practices domestically. However, it’s not a globally accepted practice. The International Financial Reporting Standards (IFRS) does not permit the use of LIFO, arguing that it can sometimes lead to less accurate inventory valuations and exaggerate earnings, particularly during periods of inflation.

Countries that adhere to IFRS, such as those in the European Union, Canada, and many others around the world, require businesses to use other inventory accounting methods, like FIFO or the weighted average cost method.

What Are Common Criticisms of LIFO Accounting?

Opponents of LIFO often point out that it can lead to distorted inventory figures that don’t necessarily reflect the true economic value, especially in times of high inflation. They argue that LIFO provides an unfair tax advantage by reporting lower net income and thus, lowering a firm’s tax liabilities. Critics also highlight the challenges it poses for comparing financial statements, as LIFO’s reliance on historical costs can differ significantly from current market values.

Moreover, detractors assert that LIFO adds complexity to accounting practices and may not represent the actual flow of goods, particularly in industries where items are not easily interchangeable or distinguishable by purchase date.

How Can a Company Transition to or from LIFO?

Transitioning to or from LIFO requires thorough planning and adherence to IRS guidelines. To adopt LIFO, a company needs to file Form 970 with their tax return for the year of the change. If they decide to switch from LIFO to another method, they must submit Form 3115 to obtain IRS approval. Any change in inventory accounting must also be consistent in subsequent financial reporting to maintain accuracy and comply with the IRS’s consistency requirement.

It’s crucial to evaluate the long-term financial and tax implications of such a switch, as changes in inventory accounting can significantly impact a company’s reported income and tax liability.

Who Stands to Benefit Most from LIFO Accounting Practices?

Businesses that deal with products whose prices rise consistently and predictably stand to benefit most from LIFO accounting practices. This typically includes industries such as supermarkets, pharmacies, and convenience stores selling items like fuel and tobacco whose costs are subject to frequent increases.

These businesses can strategically align their revenue with the cost of goods sold, recording recent, higher-priced inventory against their sales to present a lower profit and, by extension, a reduced tax expense.

In an inflationary economic climate, companies find LIFO particularly advantageous as it allows them to defer tax payments and improve cash flow, which can be critical in sustaining operations and funding growth.

What Is the Definition of LIFO in Accounting?

In accounting, LIFO stands for Last-In, First-Out, and it’s one of several methods used to manage and value inventory. It’s based on the principle that the most recent items added to your inventory are the first ones used or sold. With LIFO, the cost of these recently acquired items is the first to be recognized in the calculation of COGS, leading to specific profit and tax implications.

What Does LIFO Mean in Inventory Management?

In inventory management, LIFO means that the items you most recently stocked or manufactured are the first ones moved out of inventory when sales occur. It’s a method that businesses might choose if they are looking to align their revenue with the current cost of goods, which can fluctuate frequently in certain industries.

Essentially, LIFO is about inventory turnover – offering a strategic way to account for fluctuating prices and maximize cash flow by potentially decreasing current tax expenses.