KEY TAKEAWAYS

- Understanding the distinction between taxable income and gross income is fundamental to calculating Income Tax Expense; taxable income is what remains after all allowable expenses and deductions are subtracted from the business’s gross income.

- Small businesses can greatly benefit from mastering the calculation and management of Income Tax Expense, as it is not only a legal obligation but also a strategic tool that can be used for effective financial planning and decision-making to enhance profitability.

- Efficient management of Income Tax Expense involves staying abreast of tax laws and regulations, accurately computing taxes owed, and strategically planning finances with the objective of optimizing after-tax profitability, which can result in significant savings and improved financial outcomes for the business.

The Role of Income Tax Expense in Financial Planning

When it comes to managing your small business, anticipating Income Tax Expense is like setting the sails for smooth financial sailing. It plays a crucial role in navigating your fiscal responsibilities, as it directly affects net income and thus, any potential tax refund. A well-managed tax strategy not only impacts your tax liability but also guides you in making informed decisions about investments and operating expenses. Knowledgeable forecasting that includes estimated Income Tax Expense prepares you for any tax obligations, supporting optimized after-tax profitability. In essence, when you factor Income Tax Expense into your financial planning, you’re charting a path toward fiscal efficiency and proactive strategic growth.

The Essentials of Computing Income Tax Expense

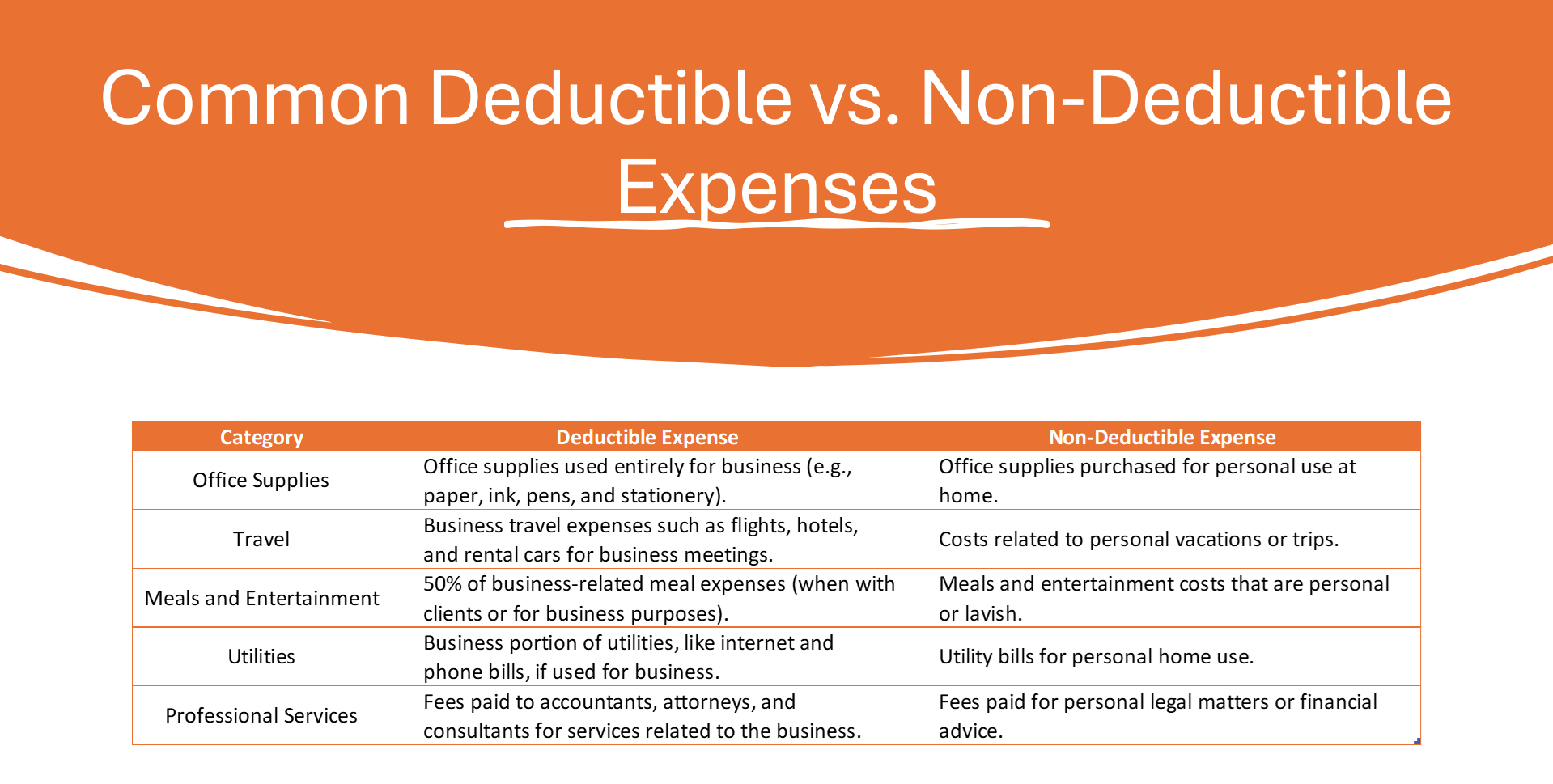

Deciphering Deductible vs. Nondeductible Expenses

Distinguishing between deductible and nondeductible expenses is not unlike the skill of itemizing—vital for maximizing your returns during tax season. Deductible expenses are those you can subtract from your income before tax is calculated, effectively lowering your taxable income and therefore your tax bill. Examples include a variety of outlays from mortgage interest to charitable donations. Conversely, nondeductible expenses, such as certain fines or personal entertainment costs, remain non-impacting on your fiscal responsibilities. To truly benefit, it’s crucial to keep precise records to itemize and document your deductible expenses; they could be your golden ticket to potential tax reductions.

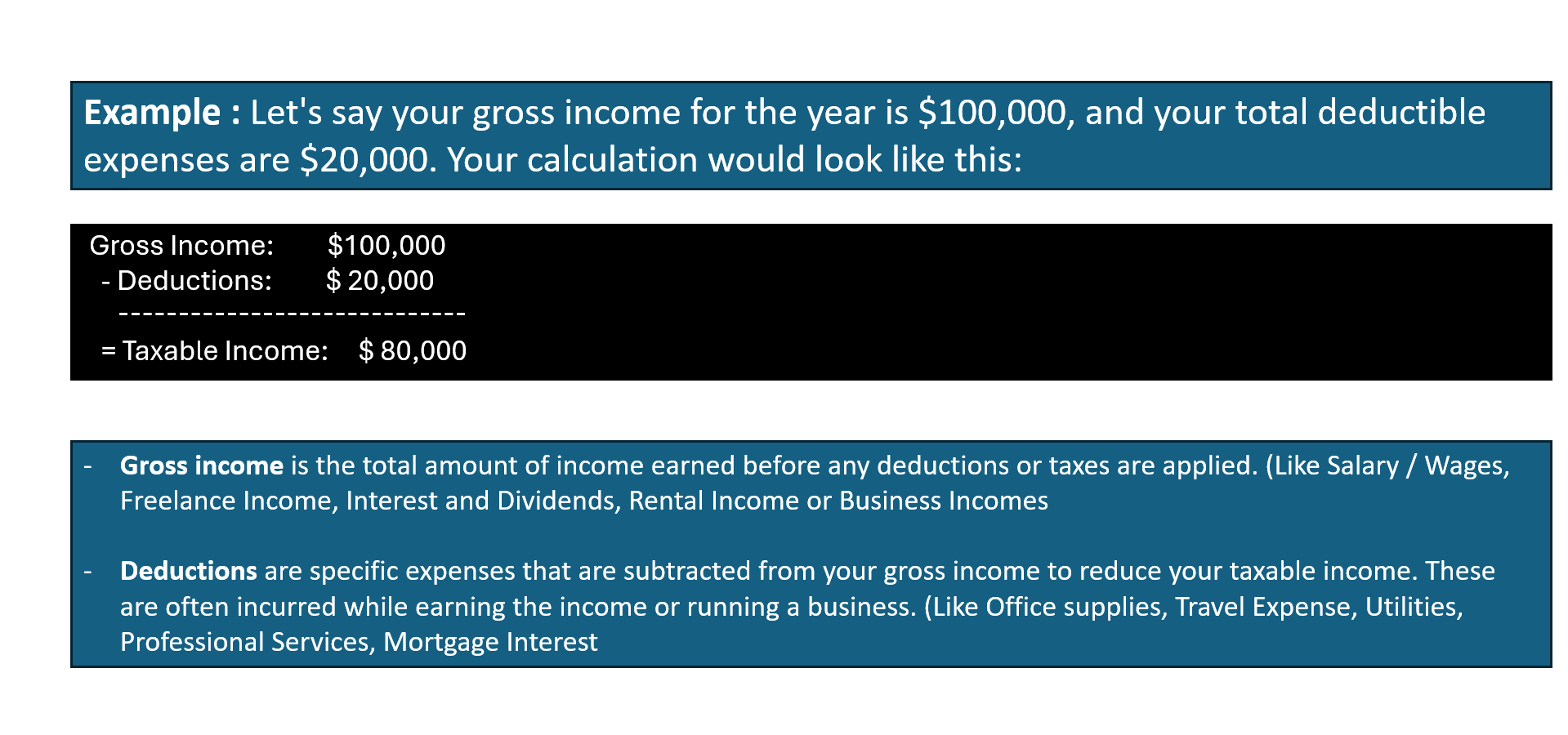

Key Formulas for Calculating Taxable Income

Unlocking the mystery of taxable income begins with a fundamental formula: Taxable Income equals your total income minus allowable deductions and exemptions. It’s all about crunching those numbers to figure out exactly what you’re working with before taxes bid their share goodbye. For individuals, this means subtracting specific deductions like mortgage interest or educational expenses from their gross income. Understanding how to navigate through tax rate calculation and brackets is crucial in this phase. Small businesses, on the other hand, will subtract their business expenses from their gross receipts. Once you deduce this net figure, you apply the current tax rates, and – voilà – you’ve got a clearer picture of your tax responsibilities.

Streamlining the Calculation Process

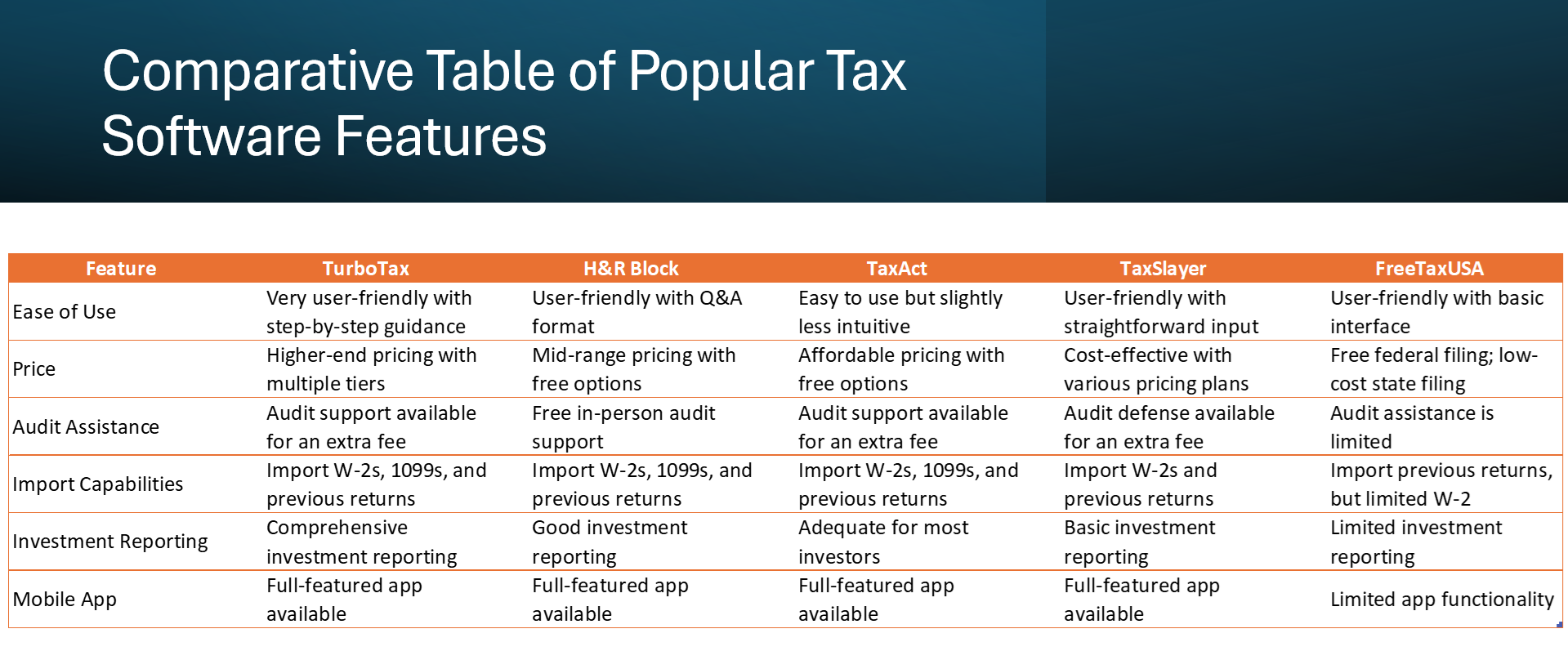

Tools and Software for Efficient Tax Calculation

The right tools can transform a taxing process into a breeze, and when it comes to tax calculations, software can be a game-chaser. No need to wrestle with complex spreadsheets or risk human errors; tax calculation tools offer precision and ease. Aim for software that can import your financial data, sort deductible from nondeductible expenses, and apply current tax laws seamlessly. Plus, with real-time updates, you can ensure compliance with the latest tax regulations. Names like Thomson Reuters ONESOURCE™ Tax Provision stand out for these reasons, promising accuracy and efficiency.

Tips for Maintaining Accurate Financial Records

Keeping spotless financial records isn’t just good practice; it’s the linchpin of stress-free tax calculations. Start with organizing receipts and invoices meticulously, and this chore will pay dividends at tax time. Invest in a reliable bookkeeping system or software that tracks expenses and income as they occur. Regularly update financial records, and reconcile bank statements. Always cross-check entries and back up your data to guard against losses. Remember, when your financial records are in tip-top shape, preparing for taxes is less of a headache and more of a structured, predictable routine.

Advanced Strategies for Income Tax Estimation

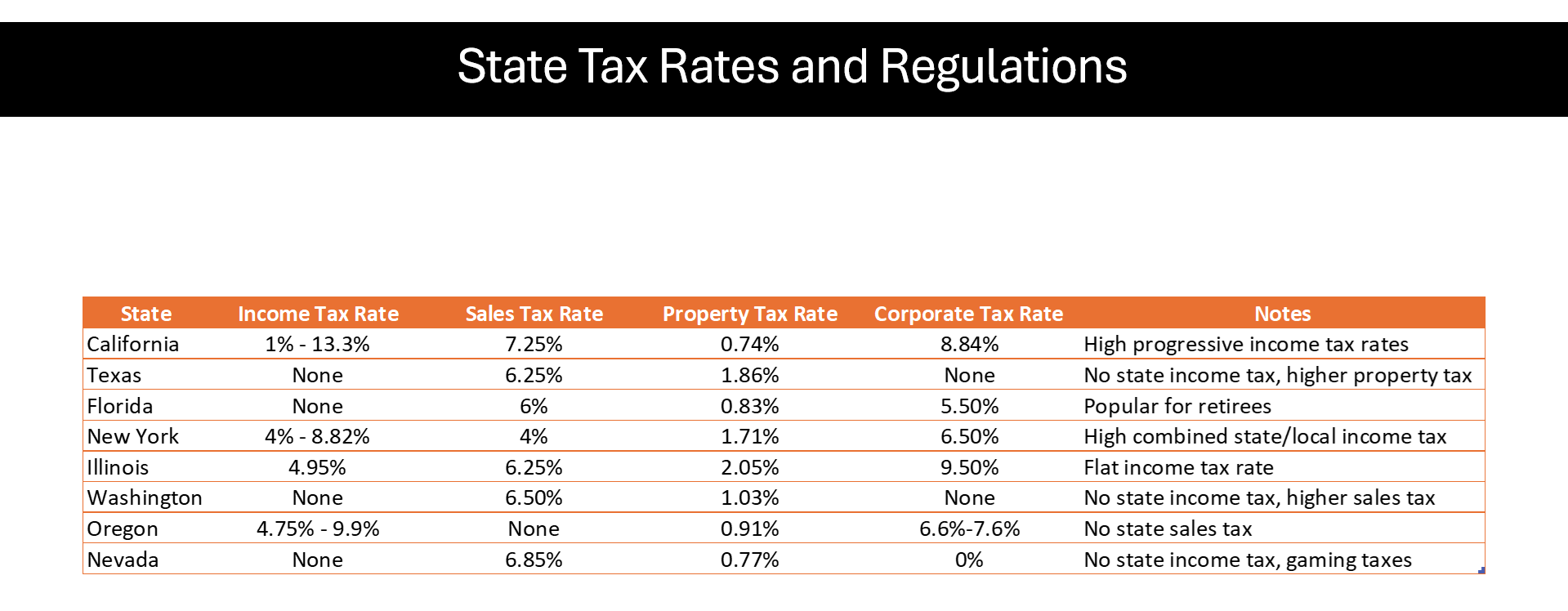

Considerations for State and Local Taxes

When you’re navigating the maze of income tax, don’t overlook the twists and turns of state and local taxes. Your total tax expense isn’t just about what you owe the federal government. Depending on where your business hangs its hat, you might need to set aside funds for state and local income taxes or opt for general sales taxes instead. Tallying these up can be less straightforward, as rates and regulations may vary widely by jurisdiction. Factoring in both state and local tax obligations ensures your calculations are comprehensive and accurate, safeguarding against unexpected liabilities.

Incorporating Credits and Deductions into Your Estimates

Injecting tax credits and deductions into your tax estimates can be like applying a discount code to your shopping cart. Tax credits are particularly potent, as they directly reduce the tax you owe dollar for dollar. Ranging from energy-efficient appliances to education, these incentives can significantly lower your tax expense. Deductions, while not as direct, lower your taxable income and can result in substantial savings. When mapping out your tax strategy, be sure to scour the tax landscape for every credit and deduction your business is eligible for—this proactive approach could translate to a leaner tax bill and a happier bottom line.

Common Pitfalls to Avoid

Steer clear of these common tax pitfalls to keep your financial ship afloat: missing deadlines can lead to penalties and interest, so mark your calendar; overlooking deductions or credits is tantamount to leaving money on the table; and miscalculating expenses could invite the ire of tax authorities. Failing to keep meticulous records can result in a nightmare during an audit. Avoid these slip-ups by staying organized, keeping abreast of tax law changes, and considering professional assistance for complex situations. They are easily preventable mistakes that can save your business time and money.

Real-World Applications

In the real world, grasping income tax expense calculation can lead to tangible benefits for businesses and individuals alike. For instance, a company can leverage this understanding to forecast its financial health and make informed decisions for future investments. Entrepreneurs who factor tax expenses into their pricing models can maintain healthier profit margins. Individual taxpayers can use these skills to optimize their returns and increase their savings. Whether by enabling more precise financial planning or identifying strategic opportunities for tax savings, the practical applications of this knowledge are both diverse and impactful.

FAQs: Answering Your Income Tax Questions

How Can I Ensure Accuracy in My Income Tax Expense Calculations?

For pinpoint precision in your tax calculations, double-check every figure and use reputable tax software or a professional accountant. Keep steadfast with your record-keeping throughout the year, and stay updated on tax law changes that could affect your calculations. Accuracy is your ally, helping you avoid costly errors or audits.

What Are the Consequences of Inaccurate Income Tax Expense Reporting?

Inaccuracies in reporting income tax expense can land your business in hot water, leading to penalties, interest charges, or even an audit. It’s a clear-cut case of honesty being the best policy—errors, whether intentional or not, can have serious implications for your business’s financial integrity and reputation.

How do you account for income tax expense?

To account for income tax expense, tally up your taxable income and apply the tax rate. Then, distinguish between the current tax expense and deferred tax expense based on timing differences between accounting and tax rules. Record the expense in your financial statements, ensuring compliance and transparency.

What is a provision for income tax and how do you calculate it?

A provision for income tax refers to an estimate set aside for future tax payments. To calculate it, assess your current income, apply estimations of tax rates, and consider potential differences between book and taxable income. It’s a forecast, not a final figure, prepping you for future payments.