Hawala Explained in Simple Terms

Imagine needing to send money to someone in a different country quickly and without the hassle of bank fees or paperwork. That’s where hawala comes in, as a nimble financial matchmaker. At its core, hawala is a method of transferring money based on trust and the extensive personal networks of money brokers called “hawaladars”. It thrives on simplicity and efficiency: you give your local hawaladar the funds you want to send, and almost like magic, your recipient on the other side of the world can collect the equivalent from their neighborhood hawaladar. To ensure reliability, the hawaladar meticulously records the transaction details, maintaining a log of these transaction records, which are often informal but honor-bound. The system is kept afloat by the honor and mutual agreements among its network, often backed by generations of trust and tradition. Add to that the perk of usually lower transaction costs compared to traditional banking, and it’s clear why hawlala has stood the test of time.

KEY TAKEAWAYS

- Hawala transactions provide rapid and lower-cost money transfer options, especially beneficial in areas with restricted access to formal banking services.

- The system offers flexibility and anonymity due to its trust-based and informal nature, often requiring minimal documentation.

- Despite the advantages, the lack of oversight and regulation within the Hawala network can make it susceptible to misuse by criminal entities for money laundering and other illicit activities.

Understanding the Mechanics of Hawala

The Basic Steps: How Hawala Transactions Work

Embarking on a hawala transaction is a journey of trust, steeped in an honor system centuries old. Here’s a breakdown of the essential steps that allow funds to invisibly shift across borders, enabling a sender to move a transaction amount to a carefully selected beneficiary:

- It all starts when someone decides to transfer money. They visit their local hawaladar and provide the transaction amount they wish to send along with a small commission. The details of the transaction, including the sender’s information and the intended beneficiary, help ensure the transaction’s accountability.

- This hawaladar reaches out to their counterpart near the recipient, communicating the amount and relevant information—such as the beneficiary’s name and location, usually over a call or even something as brief as a text message.

- A vital piece of the puzzle is the special code, or password, generated by the sender’s hawaladar, ensuring the transaction remains secure. This password is a unique identifier for the funds’ release at the other end.

- The beneficiary is given this password by the sender, which they present to their hawaladar to receive the funds. In some cases, as mentioned, the transaction amount may necessitate additional identity verification.

- If necessary, the recipient may need to prove their identity, adding an extra layer of security to the transaction. This step, while not always required, offers reassurance against fraud and mistakes.

- Ultimately, the hawaladars settle accounts, balancing out the money owed between them in various ways, relying heavily on trust to sustain the system.

This dance of digits and trust bypasses traditional banking pathways, offering a swift alternative to those needing a different method of remittance.

From Sender to Receiver: The Role of Hawala Dealers

Hawala dealers, or hawaladars, are the linchpins that hold the entire system together. Acting as financial conduits, they are responsible for both initiating and completing transactions. By entering into debt on behalf of their clients, hawaladars utilize their expansive network and expertise to ensure seamless business transactions across borders without entangling in the complexity of traditional banking systems.

For the sender, a hawaladar is someone they can trust to send their money without the bureaucracy of banks. They take the cash, note down the necessary details, and ensure the transfer begins as promised. Their role extends beyond mere transaction handlers; they often provide personalized advice and support, understanding the financial needs and contexts of their clients.

On the other end, the receiving hawaladar is equally crucial. They must verify the secure code transferred from the sender to the receiver, ensuring that the money reaches the rightful person. It’s their task to have the cash ready and to provide the service efficiently, often delivering the sense of familiarity and community that many clients value.

These dealers maintain a vast network of contacts and employ a range of informal methods to settle balances among themselves. Their relationship is built on trust, reputation, and sometimes even familial ties, with money often traversing the same networks for generations. While it is a system rooted in trust, those specializing in accounting within the hawala framework understand the importance of maintaining transaction records and carrying out due diligence to minimize the risk of their services being misused.

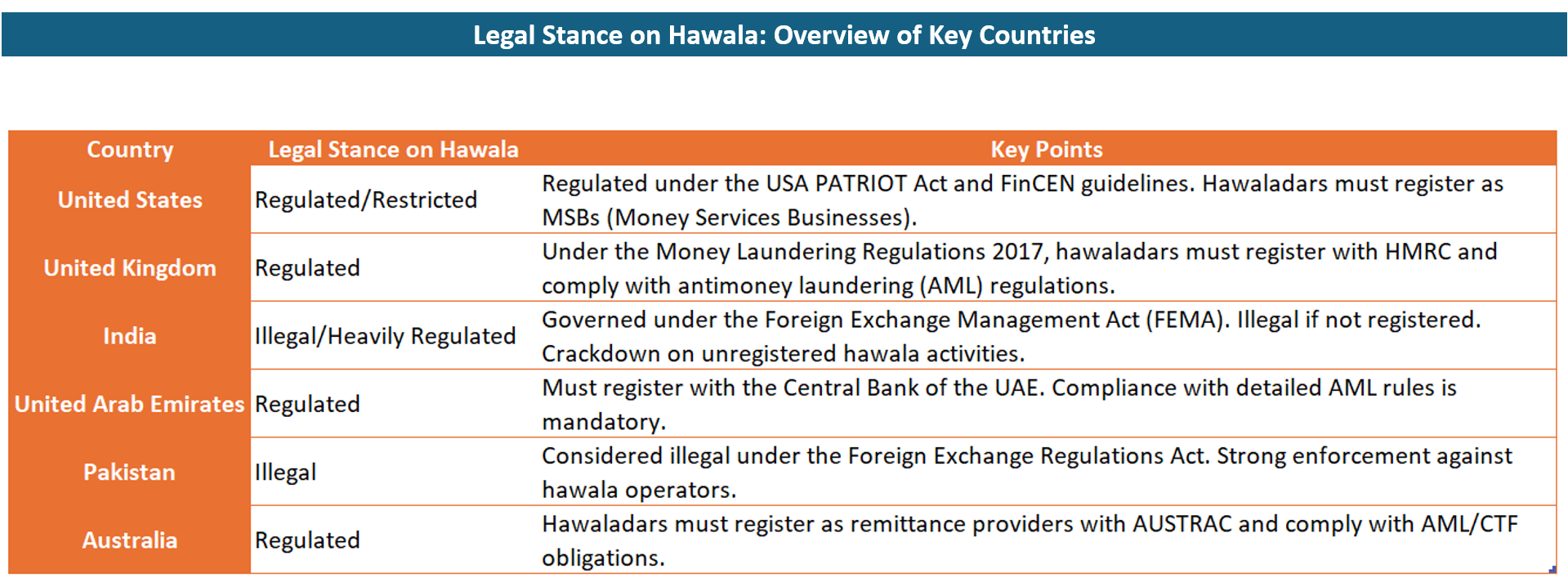

The Legality of Hawala Worldwide

Different Legal Stances on Hawala

Hawala’s presence in the world is a patchwork quilt of diverse legal stances, ranging from full acceptance to complete prohibition. Various countries have their unique perspective on the system, shaped by their domestic financial regulations, concerns about money laundering, and the need to manage financial crime.

In some nations, hawala operates in limbo, neither fully legal nor thoroughly outlawed, leading hawaladars to function in a shadowy half-world. Conversely, certain countries recognize its value for those without access to banking and have legalized and regulated the practice – a middle path that aims to curb illicit activities while acknowledging its importance.

However, some nations view hawala with suspicion, associating it with the financing of terrorism and organized crime due to its anonymity and lack of formal oversight. In these regions, engaging in hawala can carry serious legal repercussions, ranging from hefty fines to imprisonment.

Grappling with financial inclusion on one hand and security concerns on the other, the legal status of hawala remains a mosaic of global attitudes and laws, a testament to its complexity and the varying needs of countries’ financial systems.

Pinpointing the Punishment for Illegal Hawala Operations

Where hawala is against the law, the penalties for illegal operations can be stiff, intended to deter and disrupt this unauthorized financial system. In a country like India, for instance, the punishment for engaging in unauthorized hawala transactions is severe, reflecting a tough stance on shadow banking activities.

Offenders may face a monetary penalty that could climb up to three times the involved sum, with a hard stop at 200,000 Indian rupees. Additionally, there’s the prospect of the authorities seizing any currency, securities, or property associated with the infringement. Should the monetary penalty remain unpaid, the individual responsible could even confront imprisonment.

These stiff penalties underscore the difficulties law enforcement faces in tracking and prosecuting hawala dealings. Given the clandestine and decentralized nature of hawala networks, pinning down illegal operations and imposing sanctions presents significant enforcement obstacles.

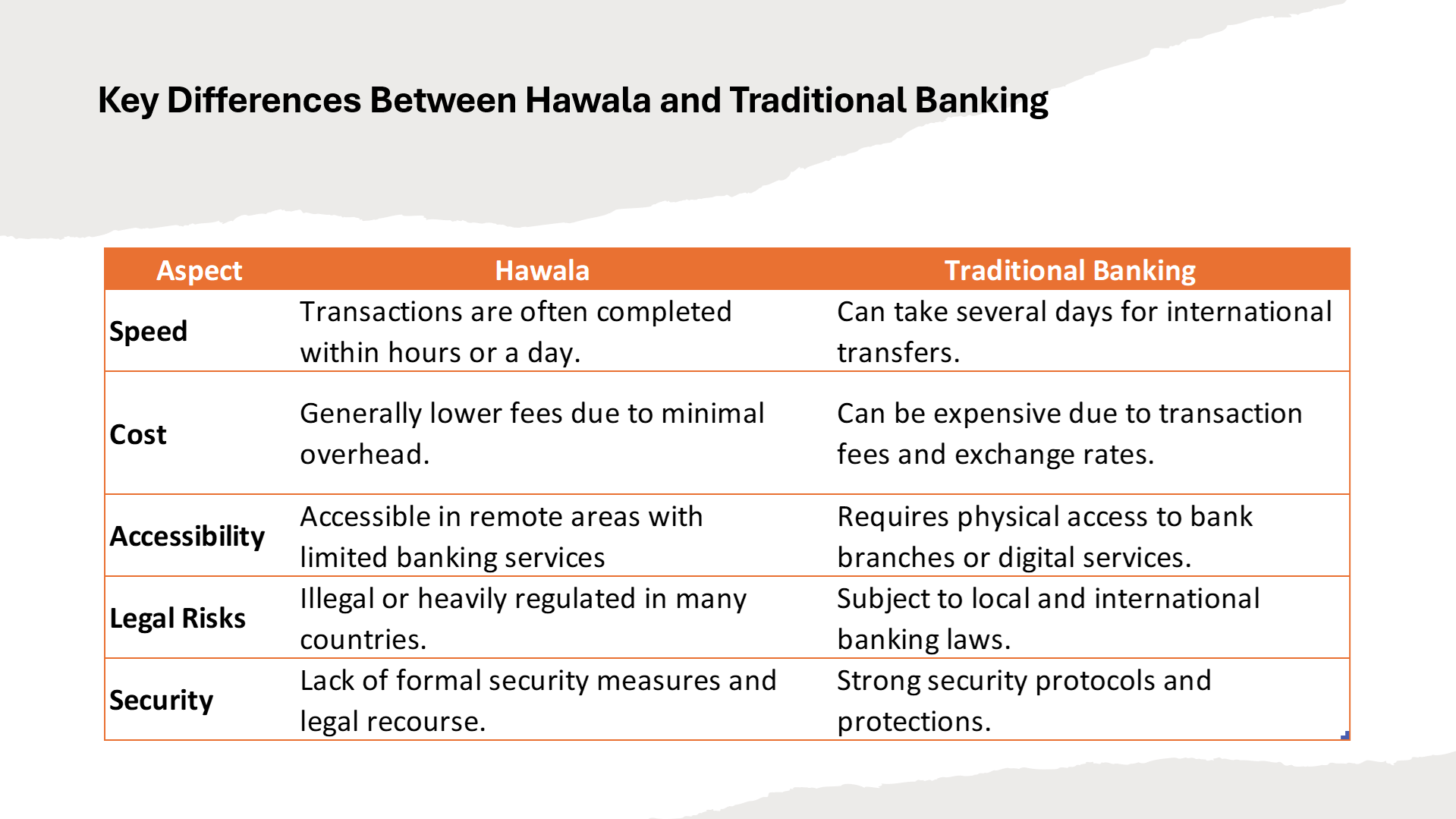

Hawala vs. Traditional Banking: A Comparative Study

When one compares hawala to traditional banking, the contrasts and similarities highlight a complex relationship between ancient practices and modern finance.

For speed, hawala transactions are often lightning-fast, as the absence of bureaucratic processing leads to near-instantaneous transfers. Traditional banks, meanwhile, may take several days for international transactions, slowed by verification processes and interbank communications.

Costs form another battleground – hawala usually offers lower fees, primarily due to its informal structure and lean operation. Banks, bearing the weight of compliance, staff, and administrative expenses, often charge higher fees, particularly for cross-border transactions.

Anonymity is offered by hawala, appealing to those who prefer to move money without leaving a paper trail. Traditional banking, bound by stringent Know Your Customer (KYC) regulations, demands thorough identity checks and transaction tracking, thus forfeiting anonymity for security.

Yet, traditional banks shine with their ability to offer consumer protections, something hawala can’t match. With insured deposits and regulated recourse options, banks provide a safety net that hawala, with its reliance on trust and personal connections, cannot.

Lastly, while traditional banking’s innovation is steered by technological advances and competitive markets, hawala’s change is often reactive, shaped by the pressures to circumvent detection and adapt to the ever-tightening global regulatory environment.

Scrutinizing the Risks and Criticisms

Scrutiny of hawala centers on its risks and the criticisms it attracts from various quarters, particularly financial regulatorsand law enforcement agencies. Key among its vulnerable aspects is its susceptibility to misuse for money laundering, terrorist financing, or even evading taxes, given the system’s inherent lack of a paper trail. This cloak of invisibility raises red flags for those who champion financial transparency.

Critics also point out the risk to consumers inherent in the system. Without formal safeguards and regulatory oversight, users potentially put their funds at the mercy of hawaladars’ honesty and financial stability. If a hawaladar defaults, the sender or receiver may have little recourse to recover their funds.

Another critique focuses on the system’s effect on national economies. Hawala’s informal nature means that these money flows bypass local banking systems and, therefore, are not accounted for in a country’s financial statistics or tax base. Such a scenario could lead to significant distortions in a country’s economic data and financial policy formulation.

However, proponents argue that hawala provides essential services where formal banking systems fail or are inaccessible. They contend that the system is not inherently negative, rather it’s the potential abuse which must be curtailed.

The challenge lies in balancing the needs of financial inclusion with the imperatives of global security and financial integrity, which continues to incite debate and shape policies around the world.

Navigating Through Regulatory Perspectives

As hawala continues to bridge financial divides across the globe, regulators are tasked with the complex mission of navigating its informal channels. This undertaking is critical but challenging, given hawala’s reliance on trust and informal agreements that stand apart from the procedural rigor of formal systems.

Compliance looms large on the horizon for hawala, with regulators pushing for transparency to ensure these transactions don’t become a conduit for illegal activities. The lack of a transparent audit trail and Hawala’s sheer adaptability further complicate the regulatory monitoring efforts.

Education and awareness among hawala operators about the importance of compliance are key. Instilling an understanding of the potential legal consequences and the societal harm that comes from facilitating illicit money flows is essential.

More so, as hawala transcends borders, international cooperation is imperative. Regulatory perspectives and strategies must align to overcome the fragmented approach that currently allows hawala networks to exploit the gaps.

The push from regulatory bodies is to do more than just police; they aim to integrate hawala within a broader, more inclusive financial system without stripping away its efficiency and accessibility. This delicate balance of regulation without stifolding is the goal that policy-makers, law enforcement, and financial experts continue to strive toward.

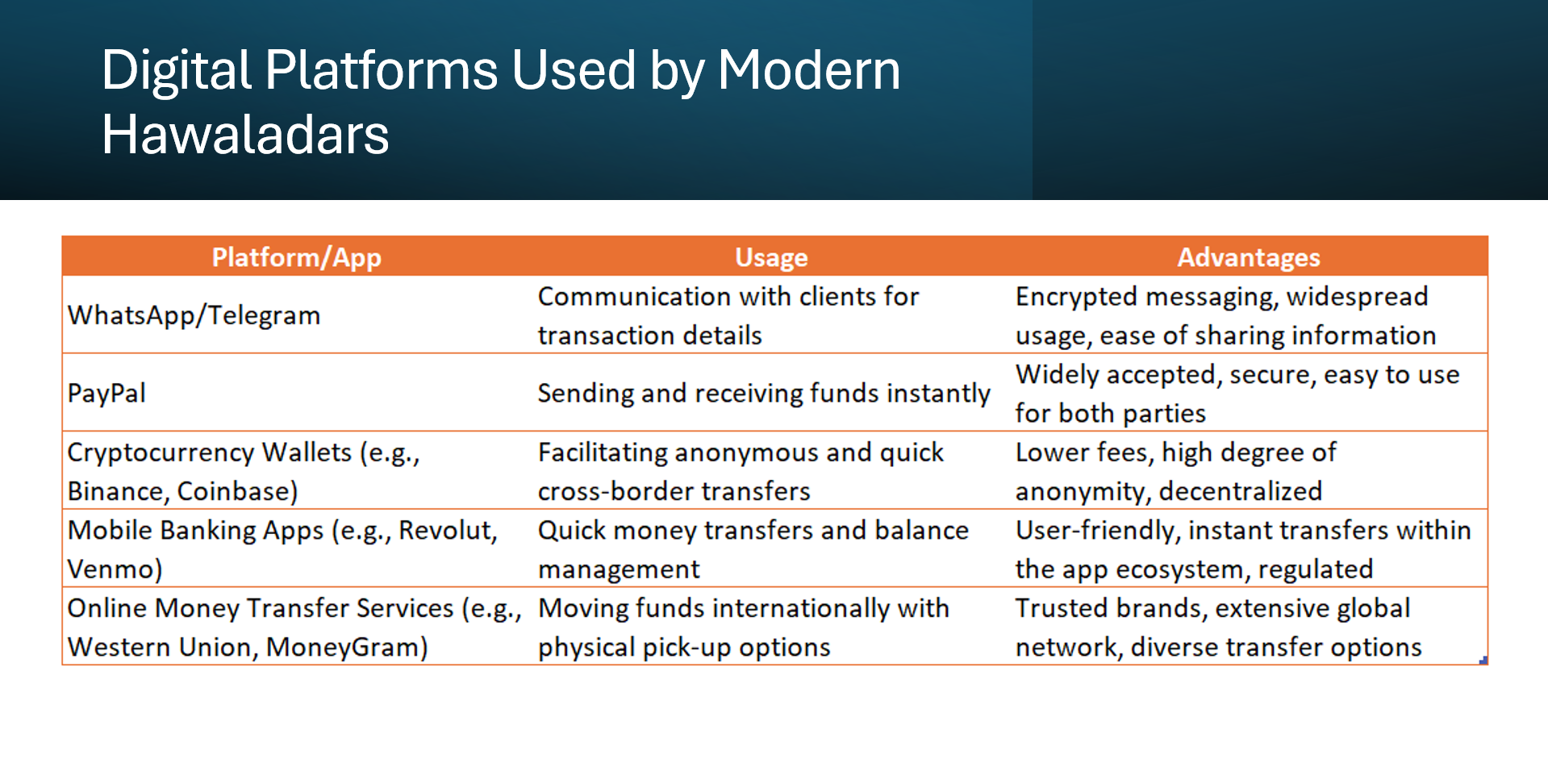

Hawala’s Modern Evolution

Hawala’s journey through the centuries has seen it evolve, adapting to the modern world while maintaining its core principles. Technology has begun to leave its mark on the ancient system, providing new means for hawaladars to communicate and transfer funds more efficiently while retaining the system’s trademark speed and cost-effectiveness.

Interestingly, hawala is beginning to undergo a form of institutionalization in some regions, where hawaladars register with the government, embracing some degree of oversight to gain legitimacy. This evolution is a dance between maintaining the cultural and operational essence of hawala and meeting contemporary regulatory demands.

Digital currencies and mobile payments are also becoming part of the hawala landscape, introducing a new layer of complexity and modernity. Hawaladars adept at leveraging these technologies can further streamline transactions, although this comes with an increased need to manage digital security risks.

Through its evolution, hawala demonstrates a robust resilience, showcasing its ability to morph and integrate within the fabric of today’s diverse, digital, and regulated financial world while still serving those who need it most.

Closing Thoughts on Hawala’s Impacts

The impact of Hawala resonates far beyond the interactions between senders and receivers, rippling through the complex currents of global finance. It’s a bridge for communities straddling borders, a lifeline for those shut out from the formal banking sector, and an asset for people looking for rapid cross-border transactions.

But hawala’s sway is also measured by the concerns it sparks in terms of financial oversight and legality. With global security and economic stability in mind, the informal system stands at the crux of heated debates on how to embrace its utility while controlling its vulnerabilities.

The enduring existence of hawala is a testament to its ability to fulfill a need in the market. Its tale is one of adaptation and persistence, and as the financial landscape continues to transform, so too will the narrative of this traditional yet remarkably adaptable system.

The conversation around hawala will likely continue to evolve, balancing the scales between financial inclusion and oversight, and keeping this ancient system relevant in the unpredictable stage of global finance.

FAQ About Hawala Simplified

What exactly is the Hawala money transfer system?

Hawala is an informal value transfer system known as hawala, providing an alternative method of transferring money without any physical money actually moving. Recognizable as both a traditional practice and a key player in the modern financial landscape, it’s an alternative or parallel remittance system that operates outside of, or parallel to, traditional banking or financial channels. It relies on a network of brokers, known as hawaladars, who are sometimes official hawala providers, ensuring that hawala businesses work based on mutual trust, affiliation, family ties, or business relationships. Moreover, the system has raised concerns for regulators due to the potential concealment of hawala activity, which could be exploited for illicit purposes.

Is Hawala legal and how is it regulated in different countries?

The legality of hawala varies by country. In some places, it operates within a legal framework where hawaladars must register and adhere to anti-money laundering regulations. However, across various jurisdictions, registration and regulatory compliance for hawala service providers can be inconsistent. Especially in jurisdictions that allow such services, many do not secure a license, leading to legal ambiguity. In others, it’s entirely illegal due to concerns about money laundering and a lack of transparency. Even in areas where hawala is considered legal, the changing landscape of financial regulation means these service providers are often subject to stringent regulations to prevent financial crimes.

Can Hawala be used for legitimate purposes, or is it always illicit?

Absolutely, hawala can be used for legitimate purposes and often is. It’s a popular means of sending money for individuals who may not have access to traditional banking services, especially in remittance corridors between countries with significant migrant worker populations. It’s important to note though, while hawala itself isn’t illicit, like any financial system, it can be exploited for illegal activities.

How does the Hawala system impact global banking and finance?

Hawala has a dual impact on global banking and finance. On one hand, it offers competition to traditional financial institutions, potentially diverting customers with its lower fees and convenience. On the other hand, it can complement banking by providing services in regions where banks are scarce. However, due to its informality, it also poses challenges for regulators in monitoring for illicit activities and ensuring financial stability.