The Fixed Charge Coverage Ratio (FCCR) is a solvency ratio that evaluates whether a company’s cash flows are adequate to cover its interest expenses, mandatory debt repayments, and lease obligations.

KEY TAKEAWAYS

- The fixed charge coverage ratio is a crucial measure of a company’s ability to pay its fixed financial obligations, like interest and lease payments, using its operating income, where a ratio above 1.5 is generally viewed favorably, indicating a strong margin of safety.

- While financial leverage can boost profitability in good economic times, it can also exacerbate losses during downturns, making it essential to consider the fixed charge coverage ratio in conjunction with other financial ratios and qualitative factors for a complete assessment of a company’s financial health.

- The fixed charge coverage ratio is a dynamic indicator that must be regularly monitored for changes that could signal either an improvement or a decline in a firm’s financial condition, thus serving as an early warning system or identifying room for improvement.

Why Is Understanding FCCR Crucial in Finance?

Understanding FCCR is like having a financial compass—it guides lenders and investors in navigating the dim seas of financial risk. When you’re eyeing to put your hard-earned money into a new project, knowing the FCCR can help you judge if it’s a ship likely to sail or sink. It signifies how much cash flow is available to cover fixed costs such as loans or leases. A sturdy FCCR means a business isn’t just staying afloat; it’s capable of chasing growth while maintaining its fiscal obligations.

Businesses that boast a high FCCR reveal the luxury of having ample free cash flow, giving them the flex to make timely payments—which for lenders, is like a beacon of reliability. However, remember that FCCR isn’t a lone wolf—it roams in a pack with other financial metrics when evaluating a business’s health.

Crunching Numbers: The FCCR Formula

FCCR Calculation Step by Step

Calculating the FCCR might seem like unraveling an intricate math puzzle, but with a clear formula and a few company-specific figures, you’ll crack the code in no time. Let’s break it down:

- First, add any taxes saved from interest deductions to your EBIT.

- Then, aggregate all your fixed charges before tax.

- Next, add interest to the fixed charges for your denominator.

- Finally, perform the division, and voila! You’ve got your FCCR.

Remember, if math isn’t really your thing, or if you’re swimming in an ocean of numbers, online calculators or accounting software can come to your rescue!

Real-World Example of FCCR Application

Let’s take a dive into an example where FCCR isn’t just a theoretical concept but a practical tool that can steer a company’s financial decisions.

Imagine a company—let’s call them “Widget Inc.”—that has taken a snapshot of their financials. For the current period, Widget Inc. reports $100,000 in EBIT. They face $60,000 in fixed charges before tax, and they also have an interest obligation of $10,000. Now, let’s crunch these numbers within the FCCR formula:

[ FCCR = {EBIT + Fixed Charges Before Tax}{Fixed Charges Before Tax + Interest}

[ FCCR = {$100,000 + $60,000}{ $60,000 + $10,000} ]

[ FCCR = {$160,000}{ $70,000} ]

FCCR = 2.286

With an FCCR of approximately 2.29, Widget Inc. stands sturdy on the financial front, showcasing the ability to cover its fixed charges more than twice over. This signals investors that Widget Inc. has a robust financial health, able to afford its fixed costs and weather potential financial turbulence.

This real-world scenario exemplifies how FCCR can provide clarity into a company’s ability to uphold its financial commitments, influence investment decisions, or guide a business in strategizing for future growth.

A Deeper Dive into Fixed Charges

Identifying Fixed Charges in Your Business

When you’re playing detective with your company’s finances, pinpointing fixed charges is your first assignment. Think of fixed charges as the ongoing financial tune your business hums, the costs that don’t skip a beat no matter whether sales are hitting high notes or low ones. Here’s how to spot them:

- Lease and Rent Payments: Whether it’s office space or equipment, if there’s a lease contract in play, the payments you make are steadfast companions to your budget.

- Loan Repayments: Any loans on the books? Those monthly installments are as fixed as the north star.

- Insurance Premiums: Insurance might feel like a grudging necessity, but it’s a constant in the financial landscape; it keeps the same pace over the payment period.

- Salaries: Unless you’re into freelance or commission structures, the wages you dole out regularly are fixed to your cost structure.

- Utilities: While the usage might fluctuate, utility contracts often have a base charge that you’re honoring regardless of consumption.

Embed these into your financial framework, and you’ll have a clearer picture of the recurring costs that shape your FCCR. By doing so, you lay a solid base for robust financial planning and risk assessment.

Can Fixed Charges Affect Your FCCR?

Fixed charges don’t just affect your Fixed Charge Coverage Ratio (FCCR); they’re the linchpin. Without them, there’d be no FCCR to speak of. These charges are like the financial anchor of your ship; they keep you grounded in reality, reminding you of the ongoing commitments that need fueling, regardless of how the tides of business ebb and flow.

Here’s how they play their part:

- The Weight on Cash Flow: High fixed charges can weigh down your cash flow, making it tougher to achieve an FCCR that signals fiscal health.

- The Reflection on Solvency: A low FCCR, pulled down by heavy fixed charges, might suggest your business is skating on thin liquidity ice, potentially alerting creditors to tighten their purse strings.

It’s not all doom and gloom, though. A strategic approach to managing fixed charges can mean smoother sailing for your business’s financial voyage.

By keeping an eagle eye on these charges and perhaps renegotiating terms or optimizing operations, you can steer your FCCR into calmer waters, portraying resilience and reliability to lenders and investors.

Interpreting FCCR Values

What Constitutes a Good FCCR?

Navigating the financial seas, a ‘good’ FCCR is like a strong gust of wind in your company’s sails. It signals to the world that not only can your business handle its fixed costs with ease, it’s poised to outmaneuver any stormy economic weather. So, what numbers should you hoist up the flagpole?

- Above 1.0: Your business stays seaworthy, meeting its fixed charges with cash to spare.

- Between 1.25 and 2.0: You’re cruising comfortably, though waters may get choppy if earnings dip.

- 2.0 or Higher: You’re the captain of a ship likely to keep a steady course, even in strong financial gales.

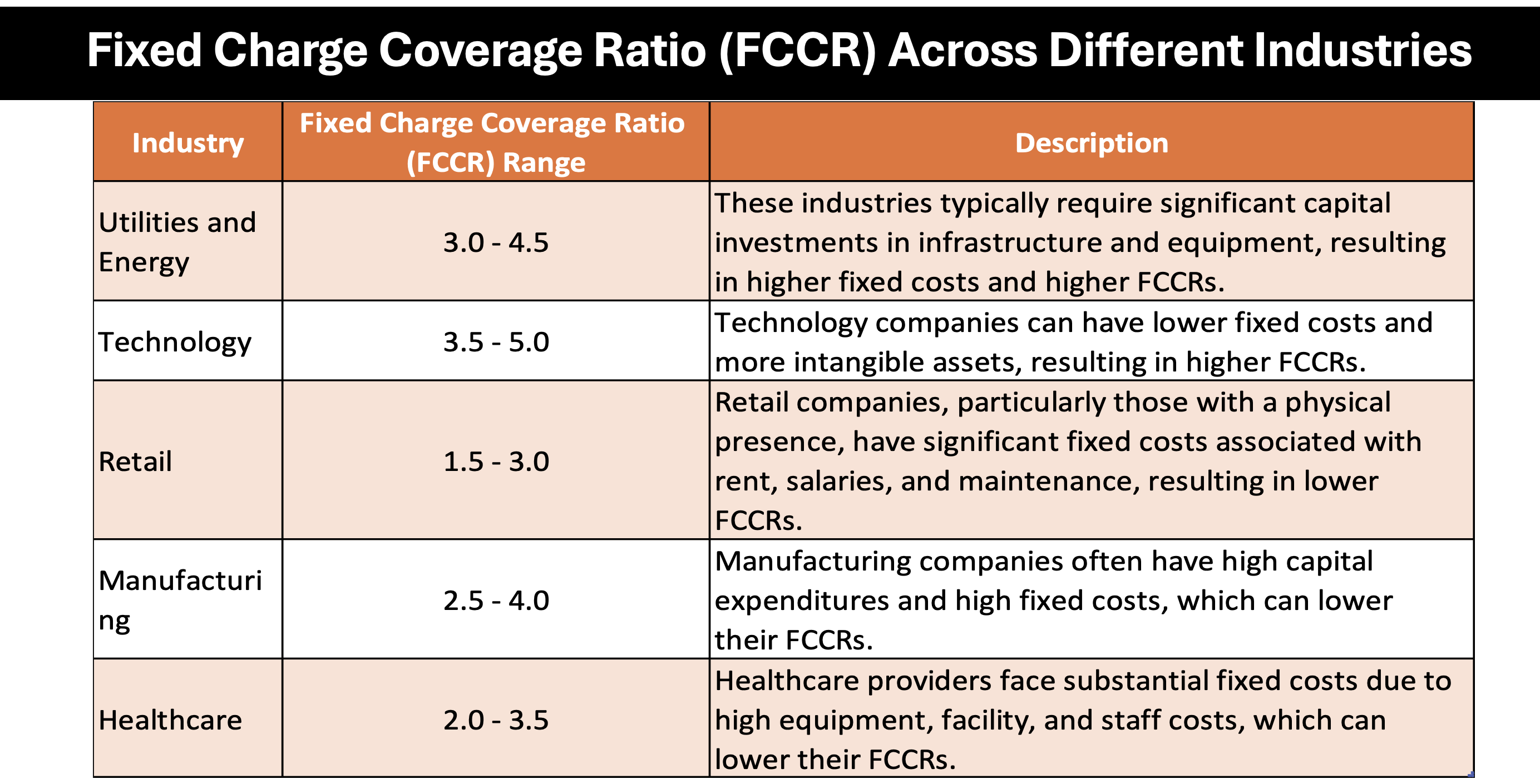

Keep in mind, these figures are a compass, not a map; sector benchmarks and historical data are crucial to charting your true fiscal position.

Remember, it’s not just about hitting that 2.0 star in the sky; make sure you adjust for the specific winds and currents of your industry for the most accurate navigation.

The Implications of High and Low FCCR Ratios

Navigating the world of FCCR, you’ll find that high and low ratios each tell their own tales about a company’s journey. Let’s explore what these different ratios suggest:

High FCCR Ratios:

- They reveal that a company is cruising with a healthy buffer between its earnings and fixed costs. It’s an open ocean of opportunities for them, with plenty of room to maneuver and invest in growth.

- It’s like a beacon of trust for potential investors and lenders, signaling stability, and the likelihood the company can weather economic storms.

Low FCCR Ratios:

- On the flipside, a low FCCR ratio can flash warning lights, indicating that your business’s earnings are too tightly lassoed to fixed charges. It raises questions about financial flexibility and the ability to take on new endeavors or debts.

- They could also hint at an investment in growth or a strategic move, such as a payout to shareholders, which, while temporarily lowering the FCCR, may pay off in the long-term voyage.

Analyzing the implications of your FCCR requires a telescope to your unique business landscape. Be aware of industry norms and your own historical performance to truly understand the message in the ratio.

FCCR in Action: Practical Uses for Businesses and Investors

Assessing Financial Health with FCCR

When you measure your business’s FCCR, you’re essentially taking its financial pulse. A robust FCCR usually means your business has a strong heartbeat and a clean bill of financial health. Here’s how it’s a handy diagnostic tool:

- Debt Payment Assessment: A high FCCR indicates your company has ample cash flow to cover fixed charges and is more likely to meet debt obligations without breaking a sweat.

- Investment Opportunities: Turning a magnifying glass on FCCR can reveal how much cash can be safely invested in growth opportunities without jeopardizing the company’s financial stability.

With a regular check-up on FCCR, not only can you reassure lenders and investors about the vitality of your finances, but you can also plot a strategic course to maintain or improve this vital sign.

How Lenders Evaluate Companies Using FCCR

Lenders use FCCR as a flashlight to illuminate a company’s fiscal landscape. It helps them see how comfortably a business can cover its fixed charges with its earnings. Here’s a peek into their evaluation process:

- Financial Solvency Check: A solid FCCR suggests solvency—that there’s enough cash flow to handle fixed costs and interest, which reflects creditworthiness.

- Loan Security: Before securing the loan, lenders look for an FCCR that comfortably exceeds 1.0, often preferring a 2.0 minimum, as it indicates a buffer against unforeseen challenges.

Lenders don’t view FCCR in a vacuum; they’ll weigh it alongside other indicators to get a panoramic view of a company’s financial health. It’s one part of a toolkit they use to make informed lending decisions.

Enhancing Your Business’s Financial Position

Strategies to Improve Your FCCR

If you’re aiming to pump up your Fixed Charge Coverage Ratio (FCCR), consider these strategic maneuvers:

- Boost Revenue: Channel efforts into refining your business’s sales pitch or customer experience to amplify earnings without piling on the marketing costs.

- Smarter Cost Management: Like trimming the sails for optimal performance, keep a keen eye on operational expenses and trim where you can without sacrificing quality or productivity.

- Refinance Debt: If high-interest debts are holding you back, look into debt consolidation to reduce the interest burden and increase your FCCR.

- Negotiate Leases: Dialogue with landlords could result in lower rental Expenses. A longer lease term might be the key to unlock a win-win situation for both parties.

Common Traps to Avoid in FCCR Management:

- Overcutting Costs: Slashing costs too deeply could impact the quality of your product or service, leading to reduced revenues down the line.

- Incurring More Fixed Costs: Taking on additional fixed charges without a clear increase in revenue can quickly torpedo your FCCR.

Impact of Capital Expenditures on Fixed Charge Coverage Ratio (FCCR)

Reduction in Cash Flow: Capital expenditures reduce the available operating cash flow, which could lower the FCCR since there is less cash to cover fixed charges like interest, debt repayments, and lease obligations.

Long-term Investments: While CapEx represents long-term investments in the company’s growth, they can temporarily strain cash flows, potentially making it harder to meet immediate fixed charge obligations and thus negatively affecting the FCCR.By adopting these strategies while steering clear of pitfalls, you’re setting the course for a stronger FCCR, revealing a business that’s on an even keel.

Common Traps to Avoid in FCCR Management

In the quest to achieve a stellar FCCR, it’s easy to fall into a few common traps. Here’s what you should be vigilant about:

- Overleveraging: Beware of borrowing more to improve cash flow in the short term at the expense of a higher long-term interest burden.

- Cost-Cutting Quicksand: Reducing expenses can improve FCCR, but cut too deep, and you might impair your company’s ability to generate revenue in the future.

- Neglecting Growth: An exclusive focus on FCCR might lead to missed investment opportunities that could fuel growth and sustainable long-term cash flow.

By dodging these snares and maintaining a balanced approach, you’ll be in command of both your FCCR and your company’s financial destiny.

Comparing Ratios: FCCR Vs. Other Financial Metrics

Is a High or Low Fixed Charge Coverage Ratio Better?

When weighing anchor on FCCR, aiming for ‘high’ is your guiding star. A high ratio suggests your business’s earnings are more than adequate to cover fixed charges, touting financial resilience. This indicates a shipshape balance sheet, ready to sail through economic headwinds with less risk of defaulting on debts.

Conversely, a low FCCR can signal storm clouds on the horizon—earnings might barely meet or fall short of covering obligations, hinting at potential cash flow squalls that could capsize growth or even lead to insolvency.

Maintaining an FCCR that’s comfortably aloft from the minimum threshold is typically a sign of a healthy financial posture, equivalent to a buoyant life vest for your business.

FCCR vs Times Interest Earned Ratio (TIE)

When charting the course of financial metrics, FCCR and TIE might seem like parallel streams but they do diverge. While both ratios gauge a company’s ability to meet certain obligations, FCCR includes all fixed charges like leases and insurance, whereas TIE is laser-focused on interest expenses alone.

FCCR: A More Comprehensive Metric

- It gives a full picture of a company’s obligations, beyond just interest, making it a more conservative and complete gauge of fiscal health.

- It’s a go-to for risk-averse lenders because it shows the company’s ability to sustain operations and service debts even with multiple fixed costs.

TIE: A Narrower Scope for Quick Insights

- TIE is swifter to calculate, offering a rapid snapshot of how many times a company can cover its interest expenses specifically.

- Common in loan covenants, the TIE ratio is like a specialized tool in a financial toolkit, zeroing in on debt serviceability.

In calm seas or stormy weather, employing both FCCR and TIE can give you a 360-view of a company’s ability to meet its financial obligations.

FAQs on Fixed Charge Coverage Ratio

How Do You Calculate the Fixed Charge Coverage Ratio?

Calculating the Fixed Charge Coverage Ratio (FCCR) is a straightforward process:

- Determine your company’s Earnings Before Interest and Cash Taxes (EBIT).

- Identify all fixed charges your company is obligated to pay regularly.

- Add EBIT and fixed charges together for the numerator.

- Sum up fixed charges and interest expenses for the denominator.

- Divide the numerator by the denominator to find your FCCR.

Remember, a ratio above 1 means you’re in a good spot to cover your fixed charges with earnings.

What is the benchmark for fixed charge coverage ratio?

The benchmark for a Fixed Charge Coverage Ratio (FCCR) varies by industry, but generally, companies should aim for an FCCR above 1 to indicate they can cover their fixed charges. Many creditors prefer a ratio of at least 1.2 as a sign of strong financial health.

What Is the Minimum Acceptable FCCR for Loan Agreements?

The minimum acceptable FCCR for loan agreements typically hovers around 1.0x to 1.25x. This reflects a company’s ability to cover fixed charges while maintaining a positive cash flow. However, it can vary based on industry norms and specific lender requirements.

Are FCCR and DSCR the Same Thing?

No, FCCR and DSCR are not the same thing. While both ratios assess a company’s ability to cover fixed expenses, FCCR includes a wider range of obligations beyond debt, making it a broader measure of financial health.

What Can Company Management Do to Optimize FCCR?

To optimize FCCR, management can focus on increasing revenue without proportionally increasing fixed costs, refining cost controls to reduce expenses, and strategically managing debt amortization through refinancing or renegotiation of terms. It involves balancing growth initiatives with smart financial planning.