KEY TAKEAWAYS

- Finance charges encompass various fees and interest that borrowers must pay when they choose to finance their purchase rather than pay with cash. These charges can include loan origination fees, mortgage broker fees, transaction fees, borrower-paid points, credit guarantee insurance premiums, and recurring fees for services like tax lien searches or flood insurance policy determinations.

- Certain charges, such as third-party fees, insurance premiums, and fees for debt cancellation/debt suspension coverage, and security interest fees, may not be included in the finance charge if they meet specific conditions. This underscores the importance of understanding the terms and conditions associated with borrowing to identify potential additional costs.

- The total finance charge is a critical concept for credit card users, as it includes all fees and purchases reflected on a credit card statement. This total can vary based on how the credit card company calculates it. Consumers should familiarize themselves with their specific credit card terms and calculation methods to manage their finances effectively and potentially avoid some finance charges.

Unraveling the Calculations

Understanding How Finance Charges Are Computed

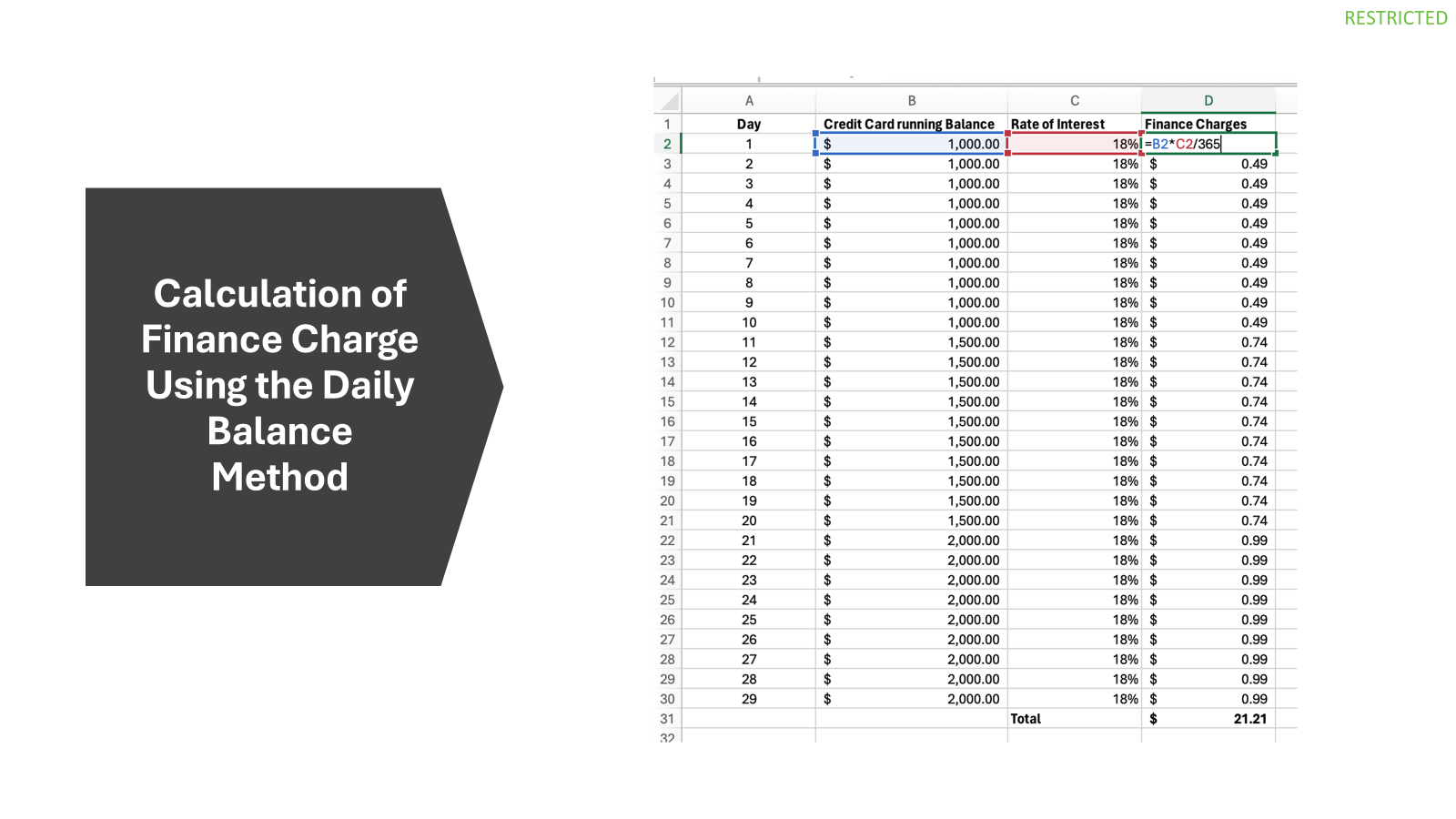

To navigate the world of finance charges, you’ll need a map and compass in the form of knowledge about how these fees are calculated. Typically, finance charges on credit cards are based on your annual percentage rate (APR) and the balance you carry. To break it down, they usually calculate your average daily balance throughout the billing cycle and multiply it by the daily rate (which is your APR divided by the days in the year).

For example, let’s say you have a series of daily balances over a billing cycle, like the oversimplified scenario provided in the research you’ve done. You’d add up those balances and divide by the number of days to find your average daily balance. Then, you apply the daily rate related to your APR, and finally, multiply by the number of days in the billing cycle to arrive at your total finance charge for that period.

Factors That Influence Your Finance Charges

Your finance charges aren’t set in stone; they can be as variable as the stock market, influenced by a range of factors related to your credit habits and market conditions. Here’s what can move the needle on the finance charges you incur:

- Credit Score & History: Lenders love a good track-record. The better your credit score, the more favorable terms you might secure, reducing potential finance charges.

- Outstanding Balances: The more you owe, the more you pay. High balances on loans or credit cards increase finance charges, especially if only minimum payments are made.

- APR: The Annual Percentage Rate directly factors into the calculation of finance charges. A higher APR means higher charges, and it can vary based on the type of credit.

- Payment Frequency: Regular payments can reduce the average daily balance, thereby lowering the finance charges.

- Type of Transactions: Cash advances and certain other transactions might come with higher finance charges compared to regular purchases.

Keep these in mind when you’re managing your credit and loans, as each of these factors plays a crucial role in the size of the finance charges that you’ll ultimately have to pay.

Credit Cards: A Double-Edged Sword

Common Pitfalls to Avoid in Credit Card Usage

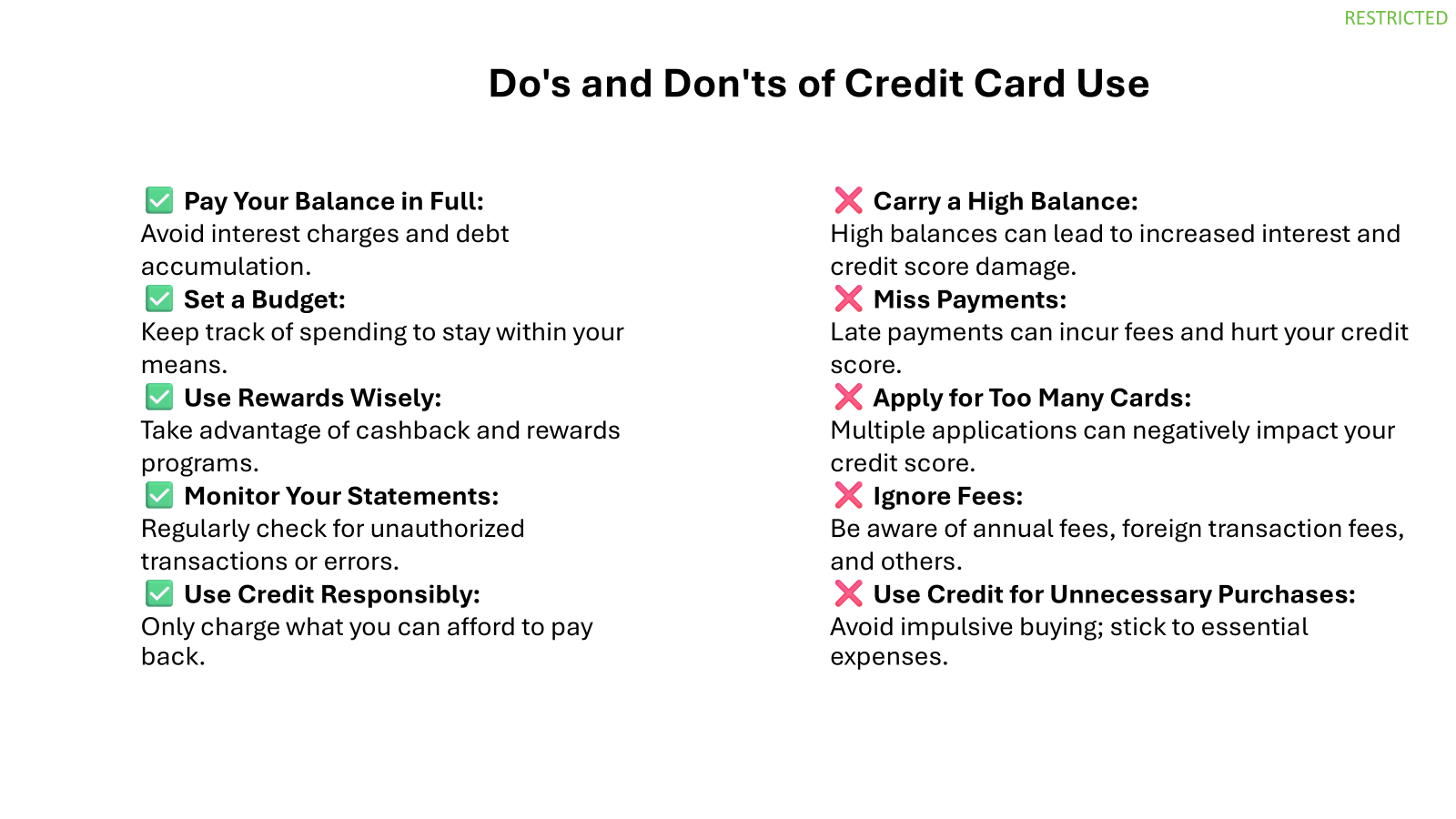

When using credit cards, it’s easy to fall into traps that can bulk up your finance charges. Here’s what you want to avoid:

- Paying Only the Minimum: It might seem manageable, but it extends your debt period and builds up interest.

- Late Payments: They not only damage your credit score but also result in hefty fees and increased finance charges.

- Cash Advances: Cash in hand comes with a price — higher APRs and no grace period mean finance charges start ticking immediately.

- Ignoring the Grace Period: If you don’t pay your balance in full before the grace period ends, your purchases start accruing interest.

- Exceeding Credit Limits: This can result in overlimit fees and increase your credit utilization ratio, affecting your credit score negatively.

By navigating these treacherous waters carefully, you can use credit cards to your advantage without falling victim to high finance charges.

Strategies to Reduce Financial Burdens

Tips to Minimize Credit Card Finance Charges

To keep finance charges on your credit card at bay, implement these tactics:

- Pay in Full: Make it a habit to clear your entire balance each billing cycle to avoid interest.

- Timely Payments: Pay on time to dodge late fees and penalty APRs.

- Zero Interest Promotions: Use cards with 0% introductory APR offers, but be sure to pay off the balance before the promotion ends.

- Avoid Certain Transactions: Stay away from cash advances and balance transfers that immediately accrue interest.

- Choose Wisely: Select credit cards with no or low annual fees, and those that offer grace periods.

By staying vigilant and applying these strategies, you can effectively reduce or even eliminate finance charges from your credit card bills.

Smart Moves for Loan and Mortgage Finance Charges

Leveraging Balance Transfers Effectively

Balance transfers can be a strategic move in your financial toolkit if used shrewdly. By transferring debt from a high-interest credit card to a card with a lower interest rate—or even a 0% introductory rate—you can save on finance charges. However, remember to consider balance transfer fees that might apply. The idea is to calculate whether the fee costs less than the interest you’d otherwise pay.

Keep an eye out for balance transfer offers with long promotional periods, giving you more time to pay down your balance without accruing interest. Just make sure to have a plan for paying off the balance before the promotional period ends, as the standard APR will kick in afterward.

Opting for Zero-percent Interest Rates When Possible

Zero-percent interest rates are the unicorns of the credit world — rare, but remarkable when found. Often offered as introductory promotions on credit cards, they allow you to carry a balance without accumulating interest, providing considerable savings on finance charges.

Here’s how you can benefit from these offers: transfer a balance from a high APR card to a zero-percent card, or plan large purchases that you can pay off during the promotional period. Beware, though — when the promotional offer expires, standard rates apply, which can skyrocket. Timing and discipline in repayment are key to ensuring you don’t trade short-term gain for long-term pain.

Practical Tactics for Account Holders

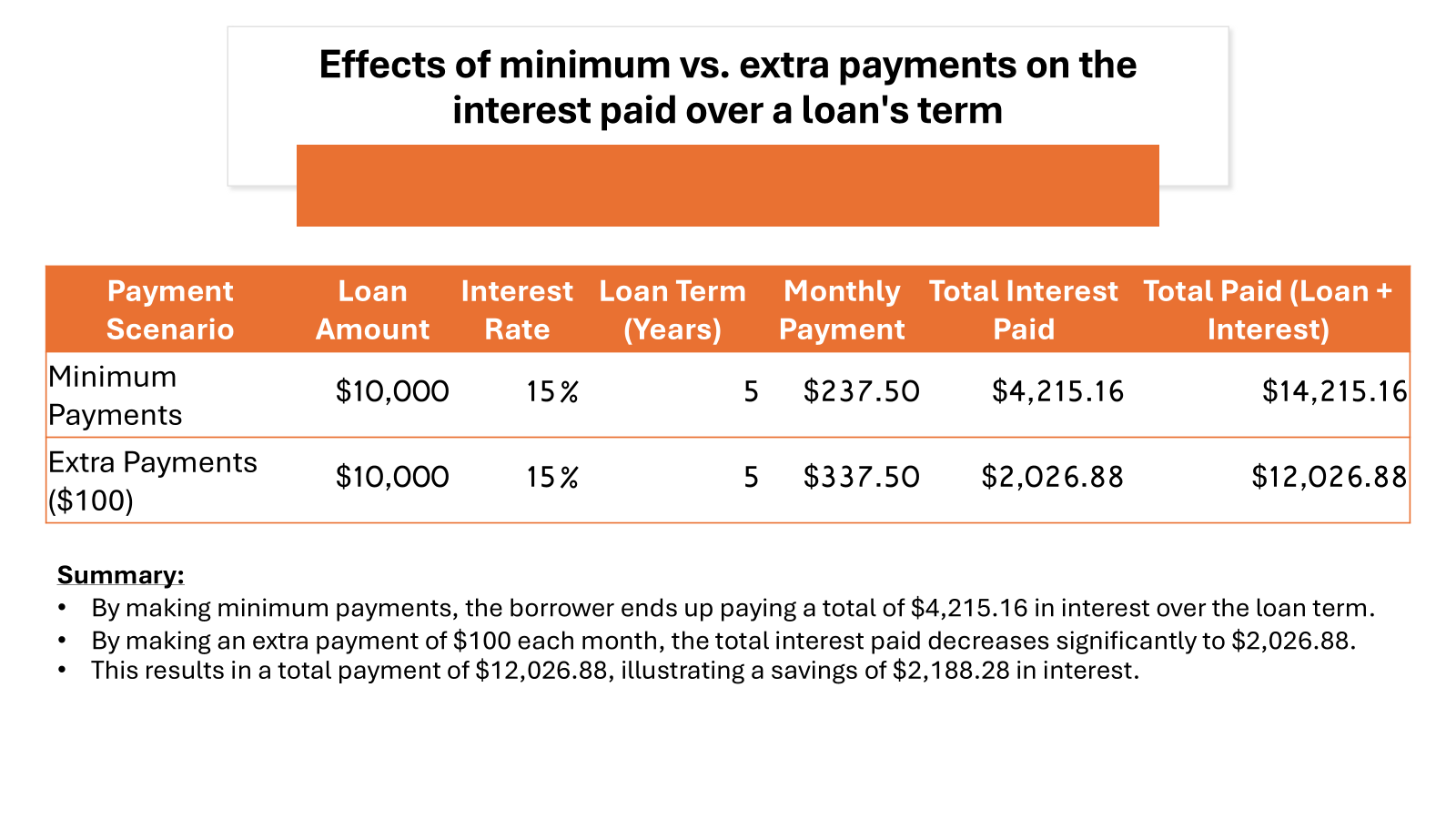

Benefits of Paying More than the Minimum Due

Paying more than the minimum due on your debts, particularly on credit cards and loans, is a great way to fast-track your path to financial freedom. By doing so, you chip away at the principal at a faster pace, reducing the total interest accrual over the life of your loan. This can mean substantial savings in finance charges and a shorter debt repayment period.

Consider these benefits:

- Less Interest Paid: Each additional dollar goes toward the principal, reducing the amount subject to interest.

- Shorter Debt Timeline: Decrease the lifespan of your debt, freeing up funds for other financial goals sooner.

- Credit Score Improvement: Lowering your credit utilization can boost your credit score, potentially leading to better rates in the future.

To reap these benefits, revisit your budget to find extra money that can be directed toward your debts. Remember, even small additional payments can lead to big savings over time.

Mastering the Art of Full Monthly Payments

Conquering credit card debt is no small feat, but mastering the art of full monthly payments puts you in the winner’s circle. When you pay off your balance in full each month, you say goodbye to finance charges on your purchases thanks to the grace period—a timeframe between the end of your billing cycle and the payment due date when no interest is charged.

The advantages are twofold: you avoid costly interest, and you maintain or even enhance your credit score by showing lenders your superb financial management. To ensure success, track your spending to avoid charging more than you can pay off, set up automatic payments to never miss a due date, and stay within a budget that supports your full payment strategy.

Beyond the Basics: Advanced Cost-Cutting Measures

Examining Rewards Credit Cards and Their Advantages

Looking at rewards credit cards, they’re not just about the bells and whistles — they come with tangible benefits that can sweeten the deal of your spending.

Best Product: Rewards Credit Cards

Why it’s great: Rewards credit cards enhance the value of each dollar you spend by offering points, miles, or cash back on your purchases. They often come with additional perks like sign-up bonuses and exclusive deals.

Top 5 Features:

- Cash Back Rewards

- Travel Miles

- Points for Purchases

- Sign-Up Bonuses

- No Foreign Transaction Fees

Benefits:

- Get money back on everyday expenses.

- Save on travel with miles and travel insurance benefits.

- Points can be redeemed for goods, services, or statement credit.

- Large bonuses can offset costs or fund a whole vacation.

- International purchases don’t carry extra charges.

Cons:

- Rewards can tempt overspending.

- High-interest rates if balances aren’t paid in full.

Best for: Consumers who pay off their balance each month and want to maximize the value of their purchases.

By choosing the right rewards card and using it responsibly, you can enjoy a diverse range of benefits without falling into common credit pitfalls.

How Debt Consolidation Can Lead to Sizeable Savings

Debt consolidation can be a life raft in a sea of high-interest debts. It works by rolling multiple debts into a single, new loan, usually with a lower interest rate and more manageable monthly payments. If they’re feeling strained by various high-interest accounts, they might find their monthly outflows trimmed and their financial stress eased with a consolidation loan.

For example, consolidating high-interest credit card debts into a single low-interest personal loan means they often pay less over the life of their debt. While this strategy simplifies payments and may improve your credit utilization ratio, it’s essential they avoid accumulating new debt in the process, which could defeat the purpose of the consolidation.

Key advantages of debt consolidation include:

- Potential for lower interest rates and finance charges

- Simplified finances with a single monthly payment

- The opportunity to pay off debt faster

- May improve credit score by lowering credit utilization

- Possible lower monthly payments to improve cash flow

However, they must watch out for potential pitfalls such as costs related to balance transfer fees or closing costs on a new loan. The key to success is to compare the total costs and benefits carefully.

Real-world Examples and Success Stories

Case Studies: How Ordinary People Have Reduced Charges

Across the globe, ordinary people are finding inventive ways to reduce their finance charges, providing us with valuable case studies that inspire and educate. For instance, consider Alex, who juggled multiple credit cards with high interest rates. By transferring their balances to a single card offered by credit card issuers with a zero-percent introductory offer and paying it down aggressively, they slashed their finance charges dramatically.

Then there’s Sam, who noticed their credit score was holding them back from getting lower mortgage rates. They focused on improving their credit health by paying bills on time and reducing debt. Six months later, they refinanced their mortgage at a significantly reduced rate, cutting down the total finance charges payable over the life of the loan.

These real-world examples prove that with some savvy decisions and disciplined financial practices, it’s possible to diminish the impact of finance charges and keep more money in your pocket.

Testimonials: Triumphs in the Face of High Finance Costs

The tales of those who’ve tamed their towering finance charges are not just uplifting; they are testaments to financial tenacity and ingenuity. Take Jamie, for example, who grappled with steep finance charges across multiple cards. By devising a strategic repayment plan that targeted the highest-interest debt first while maintaining minimum payments on others, they eventually emerged victorious against the tide of interest.

Or consider Jordan, whose entrepreneurial spirit led them to negotiate a lower APR directly with their credit card company. Armed with an impeccable payment record and the prospect of transferring their balance, they successfully persuaded the issuer to reduce their rate, ultimately lowering their finance charges.

These testimonials underscore a powerful message: with determination and the right approach, triumph over high finance costs is within reach.

Preemptive Steps to Safeguard Your Finances

The Role of Emergency Funds in Preventing Finance Charges

An emergency fund is your financial buffer against unexpected life events that could otherwise lead to taking on high-interest debt. By having a reserve of cash, you avoid the need to use credit cards or loans for unexpected expenses, which can accrue high finance charges.

A healthy emergency fund should cover three to six months of living expenses, providing peace of mind and protection. When you tap into this fund instead of credit options in an urgent situation, you save money by avoiding additional interest that would accumulate from finance charges.

Building a Budget That Keeps Finance Charges at Bay

A well-crafted budget is your best defense against the relentless creep of finance charges. It’s your strategic approach for judiciously allocating funds, ensuring you can cover all your bills without delay, including credit payments. This vigilance keeps finance charges low since, according to the Truth in Lending Act (TILA), credit terms must be transparent, helping you to avoid the unseen costs of credit transactions. By prioritizing debt repayment and avoiding carrying a balance, you can sidestep hefty interest charges that often accompany credit transactions.

Start by meticulously tracking your income and expenses to gain a granular understanding of where your money goes. Then, set realistic spending limits in each category, ensuring that you allocate enough funds toward debt reduction. According to TILA stipulations, paying off credit transactions promptly avoids additional finance charges that may not apply to similar cash transactions. Remember to include savings—it’s not just about clearing what you owe, it’s also about building a financial cushion that can secure your future and provide peace of mind.

The Future of Finance Charges

Trends That Could Influence Finance Costs

The landscape of finance charges is not static; it’s shaped by broader economic trends and legislative changes. Recently, there’s been a focus on more consumer-friendly credit terms with increased transparency. Technological advancements have also introduced more dynamic pricing models, where finance charges can vary based on real-time risk assessments.

Interest rate trends set by central banks directly influence finance charges on credit products. In a low-rate environment, finance charges are generally more affordable, stimulating borrowing and spending. Conversely, when rates rise, finance charges increase, potentially slowing down consumer spending and borrowing.

Keep an eye out for emerging fintech innovations too, as they could revolutionize the way finance charges are assessed and collected, potentially passing on savings to you.

Innovations in Credit Terms and How They Affect You

In a constantly evolving financial industry, innovations in credit terms aim to cater to consumer needs and competitive markets. Lenders are adopting more user-friendly platforms and terms, like customized credit limits and repayment plans based on individual financial situations. There’s also a trend towards more rewards and benefits to encourage on-time payment and loyalty, which can help offset finance charges indirectly.

Financial tech startups are disrupting the usual credit terms with features like early salary access and zero-interest credit offerings. However, always read the fine print to gauge how these alternatives stack up against traditional credit products when it comes to long-term finance charges.

When engaging in any financial transaction, especially when borrowing money or making investments, understanding finance charges is crucial. Finance charges encompass a range of costs associated with borrowing or financial transactions, including interest payments, fees, and penalties. Here, we unravel the complexity of finance charges by discussing several key terms that frequently emerge in this space.

1. Discounts and Price Differentials:

Discounts represent reductions in the purchase price or interest rate. Understanding price differential is essential, as it can significantly impact the total cost of a financial transaction, such as a mortgage transaction.

2. Taxes and Currency Impact:

Taxes are mandatory contributions to state revenue, impacting financial decisions due to their direct effect on transaction costs. When performing transactions in foreign currencies, exchange rates can alter the net amount received or paid.

3. Debt Cancellation Coverage and Suspension Charges:

Debt cancellation coverage provides protection by canceling the remaining debt under specific conditions, like job loss, while debt suspension charges temporarily halt payments without canceling the debt.

4. Loan Origination Fees and Mortgage Broker Fees:

A loan origination fee or mortgage broker fees are upfront costs paid for processing a new loan application. Such fees contribute to the cost of obtaining a mortgage or another type of loan.

5. Collateral, Deeds, and Subrogation:

Collateral acts as security for a loan. If the borrower defaults, creditors might claim the collateral. Deeds are legal documents representing the rights to property. Subrogation involves a third party, such as an insurer, stepping into the shoes of another to claim reimbursement.

6. Escrow Agents and Transaction Account Charges:

An escrow agent holds and manages funds or assets until specific conditions are met. Additionally, transaction account charges include fees incurred for maintaining accounts and executing transactions.

7. Insurance Premiums and Insurance Disclosures:

Insurance premiums are payments made to maintain various forms of insurance coverage, such as health or credit insurance. Insurance disclosures provide crucial information regarding the terms and conditions of an insurance policy.

8. Credit Insurance Premiums and Debt Suspension Charges:

These premiums help cover loan payments in events like illness or unemployment. Debt suspension charges can arise if payments are temporarily halted under specific circumstances.

9. Lending Disclosure Statements:

These documents offer borrowers detailed information regarding the terms of their loan, including interest rates, fees, and penalties, thereby fostering transparency.

10. Dividends and Interest in Time Deposits:

Dividends are returns on investments distributed from profits, while time deposits are bank deposits held for a fixed term, accruing interest over time.

11. Occurrence of Default and Its Consequences:

A default occurs when a borrower fails to make payments as agreed. This can lead to severe repercussions, including foreclosure or repossession by the lender.

12. Pest Infestation Concerns in Property Deals:

Unanticipated issues, such as pest infestations during property transactions, can affect the property’s value and lead to unexpected financial burdens. Understanding these terms will help individuals navigate the complexities of finance charges, ensuring more informed decision-making in their personal and professional financial endeavors. Whether dealing with a mortgage, investment, or insurance, being knowledgeable about these components is vital for financial well-being in the United States and beyond.

Frequently Asked Questions

Is It Possible to Completely Avoid Finance Charges?

While it’s nearly impossible to completely avoid finance charges if you use credit cards or take out loans, you can minimize them significantly. Pay your credit card balance in full each month, choose cards and loans with the most favorable terms, and if you’re taking advantage of a promotional zero-percent interest rate, ensure you pay off the balance before the promotion ends. Proactive financial management is your best ally in keeping finance charges to a minimum.

Do All Financial Institutions Charge the Same Rates?

No, financial institutions do not charge the same rates. They vary based on the institution’s policies, the type of financial product, and individual creditworthiness. Shopping around and comparing offers is essential to find the most competitive rates and can lead to significant savings over the lifespan of a loan or credit balance. Always read the fine print and consider both the short-term and long-term costs when evaluating your options.