The Cardinal Rules for Applying the Equity Method

The equity method sets a framework for how you should account for investments where influence is significant, but control is not absolute. The rule of thumb states that if you own between 20% and 50% of the voting shares of another company, you’re likely to have the significant influence needed to apply the equity method. It’s not just about the percentage; actual influence over business decisions seals the deal. This method reshapes your investment from a passive number into an active participant, mirroring the ebbs and flows of the investee’s fortunes in your own financial statements. Remember, the equity method is a commitment from the get-go; you apply it from the moment you gain significant sway until you lose it, reflecting your share of profits or losses each step of the way.

To simplify the cardinal rules:

- Ownership interest is typically between 20% and 50%.

- Investments are on the books as associates or joint ventures.

- The investor’s share of post-acquisition profits or losses is accounted for in the financial outcomes.

- Received distributions lower the investment’s carrying amount on your balance sheet.

KEY TAKEAWAYS

- The equity method is utilized when an investor holds a significant influence in the investee company, typically defined as owning between 20% to 50% of the voting shares, leading to adjustments in the investment account to reflect the investor’s proportion of the investee’s profits and losses.

- An investor’s share of profits increases the investment account balance, whereas their share of losses decreases it.This method ensures the investor’s balance sheet and income statement better reflect the true nature of their investment in the investee compared to other methods such as the cost or fair value methods.

- Maintaining accuracy in equity method accounting involves careful tracking and adjustments for dividends received, the investor’s share of the investee’s income and losses, and changes in ownership percentages, which can be complex and require a detailed understanding of equity method journal entries and reporting.

Navigating the Pathways of Initial and Subsequent Measurements

Getting Started: Initial Measurement Essentials

When you first acquire an equity investment eligible for the equity method, the initial measurement is pretty straightforward: it is the amount you paid to buy into the company plus any direct costs that hitched a ride with the purchase. Imagine you’re buying a share of a company at $100,000 and spend an additional $3,000 on associated costs such as legal fees; right off the bat, your investment account balance starts at $103,000. This crucial first step lays the foundational stone upon which all subsequent measurements of income, loss, and even dividends will be carved. Recognizing these initial costs accurately is vital, as it sets the trajectory for how you will navigate through the nuances of equity method accounting in the future.

To get started right, make sure to account for:

- Purchase price of the investee’s stock.

- Direct acquisition costs like investment banking, legal, valuation, and accounting fees.

- Any other expenses directly attributable to the acquisition.

Beyond the Beginning: Subsequent Measurement Nuances

Once your investment is snugly accounted for on the balance sheet, the subsequent measurements weave a tale of continued engagement with your equity stake. This journey isn’t just a one-time calculation; it’s an ongoing process that reflects the investee’s business performance within your financial ecosystem. Each reporting period, you adjust the carrying amount of the investment to factor in your share of the investee’s profits or losses. Think of these as little financial postcards from your investee, telling you how well they’re doing—or not.

To navigate these nuances, you’ll whisk through a recipe of adjustments that includes:

- Allocating your share of the investee’s net income or loss, which will require vigilance and often a dash of judgment.

- Accounting for dividends received from the investee as reductions in the carrying amount of the investment, rather than income—like a financial diet for your balance sheet.

- Amortizing any basis differences in identifiable assets and liabilities over their useful lives, adding layers of complexity to the financial flavor profile.

The Tug of War: Changes in Ownership and Accounting Methods

Transitioning Between Methods: A Critical Analysis

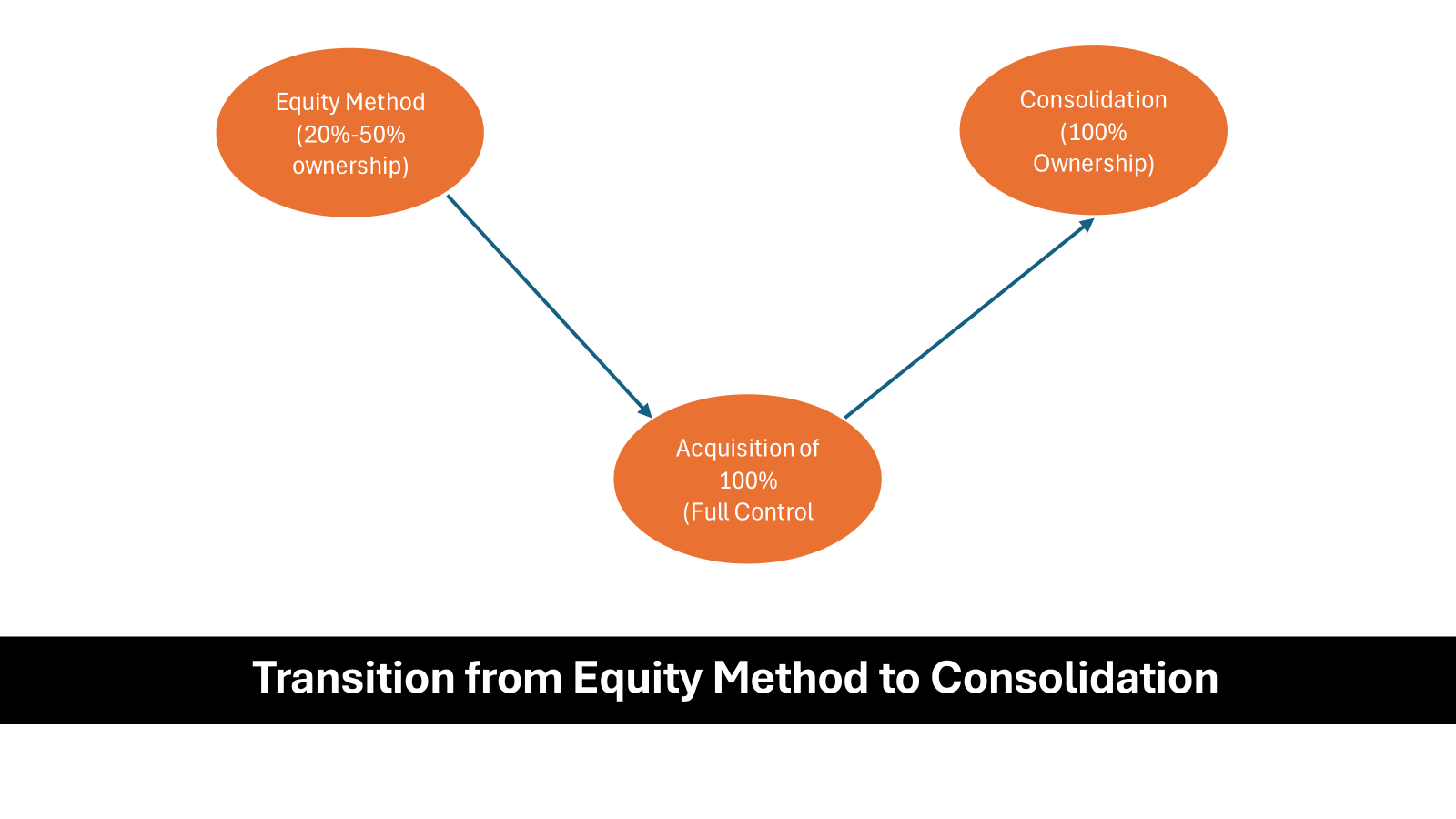

Imagine you’re on a financial seesaw; on one end is the equity method and on the other, different accounting treatments like the cost method or consolidation. Transitioning between methods is not child’s play; it demands critical analysis and precise maneuvering. This happens when there’s a significant change in your ownership interest, tipping the scales of influence or control.

For example, if you acquire enough additional shares to flip your significant influence into control, you’ll need to transition from the equity method to consolidation, where you combine the investee’s financials with your own. On the flip side, if you sell off part of your stake and your influence diminishes, you might shift to the cost method, dialing back your engagement with the investee’s financial performance.

To smoothly transition between methods, keep an eye on the following:

- The event triggering the change, such as acquisition or sale of shares.

- The date of the event, as this will determine when to apply the new accounting treatment.

- Any measurement adjustments required at the date of the change, which may include fair value considerations.

- Retrospective application versus prospective application, understanding which changes will ripple back through past reports and which will only affect future numbers.

Percentage Ownership Dynamics and Financial Implications

Percentage ownership in an equity investment is like a volume knob for your influence over an investee’s operations and decisions. As you twist this knob – through buying or selling shares – the dynamics of your ownership reverberate through your financial statements. A crescendo above 20% typically ushers you into the realm of the equity method, while a decrescendo below might see you wave goodbye to it.

These changes aren’t just symbolic; they bear real financial implications. If you amp up your investment, expect to account for your share of the investee’s profits, losses, and even impairments. Dwindle down your stake, and you’ll trim down these financial reflections accordingly. It’s also not rare for a shift in the degree of ownership to warrant a reconciliation process, as you adjust your books to the new accounting tune.

Keep in mind the effects of:

- Increased ownership possibly leading to more profits but also more exposure to losses and impairment risks.

- Decreased ownership resulting in less influence on the investee and potentially a need to switch accounting methods.

- Ownership close to threshold percentages requiring keen attention as small changes can have big accounting consequences.

The Investor’s Perspective: Influence and Power Over Investees

Significant Influence: More Than Just a Numbers Game

In the dance of corporate synergy, significant influence is a step that goes beyond the simple sway of percentage points. It’s an intricate tango involving presence in boardrooms, a hand in shaping policies, and a say that echoes in the financial strategies of the investee. While holding 20-50% of voting power can be a clear sign of such influence, even a smaller slice of the pie can have weight if your voice carries across the table.

Consider significant influence as being part of a club with exclusive membership privileges, where your opinions hold sway. It’s not about pulling strings from a corner but about being in a place where your insights and expertise mold company trajectories. Accounting-wise, this influence means you’re sharing not just in the profits and losses but also in the risks and rewards, making for a complex yet rewarding financial partnership.

When assessing significant influence, focus on:

- Your representation on the board and participation in policy-making processes;

- The presence and complexity of material transactions and dependencies between entities;

- The extent of your ownership and tethers through management personnel.

Investor Strategies to Watch in Equity Method Accounting

Investors wielding the equity method like a financial instrument often adopt strategies that reflect their long-term visions and risk appetites. Whether you’re gearing up for influence or bracing for impact, they adjust their approach in sync with the market’s rhythm and their investee’s performance. Engaging in frequent discussions with management, suggesting operational improvements, or steering strategic financing—these are just a few moves in an investor’s playbook.

The seasoned investor will also keep their eyes on the horizon, looking out for significant downturns that might send ripples across their investment value, requiring impairment testing. It’s all about balance, ensuring their investment is nurtured for growth while being prepared to make tough calls when the storm clouds gather.

Key strategies include:

- Active involvement in operational and financial decision-making processes;

- Regularly evaluating the investee’s performance and potential for synergistic outcomes;

- Strategically timing the entry and exit of investments, keeping a watchful eye on impacts that could require swift changes in accounting methods or impairment assessments.

Real-World Insights: Case Studies and Practical Examples

From Theory to Practice: Equity Method Illustrated

Putting the equity method into action is like translating a complex recipe into a mouth-watering dish. It may seem a bit overwhelming at first, with all the different ingredients—income, losses, dividends, and impairments—but once those financial flavors start to blend, the results can be truly satisfying. Real-world examples paint a vivid picture of this: a company buys a 30% stake in a business and begins to see their portion of the investee’s profits enhancing their own bottom line each year. And when the investee declares a dividend, they subtract it from the carrying value of the investment, keeping the balance sheet calibrated.

These practical illustrations reveal the beauty and intricacy of the equity method—every entry tells a story of intertwined businesses, each dependent on the other for financial accuracy and success.

To understand the equity method in practice, consider:

- A step-by-step breakdown of acquiring a significant influence investment and reflecting its results in financial reports.

- Examples where investor decisions significantly affect the investee, illustrating the depth of influence held.

- Diving into annual reports to identify how adjustments due to profits or dividends from equity method investments show up in real-world financial statements.

Lessons from the Frontline: Notable Equity Accounting Scenarios

The equity accounting battlefield is riddled with stories of tactical maneuvers and lessons learned—the victories and cautionary tales that emerge when companies engage with the equity method. Notable scenarios pull back the curtain on when a company’s reporting reflects not just their triumphs but also their trials, such as recognizing impairment losses when an investee underperforms, or recalibrating investments following a substantial shift in ownership percentage.

These tales from the frontline provide invaluable insights, such as the importance of transparent reporting and vigilant oversight to avoid the pitfalls that can accompany complex financial entanglements. They emphasize the value of foresight—being able to anticipate and act upon the effects of market changes and investee performance on one’s financial health.

For a comprehensive understanding, examine scenarios where:

- A company needed to report significant losses due to an investee’s downturn, highlighting the risk and reward dynamics of equity investments.

- Shareholdings straddle the line of significant influence, prompting critical reassessments of investments.

- Changes in investee corporate governance or strategy led to substantial accounting adjustments for an investor.

Challenges and Critiques: Understanding Potential Pitfalls

Pinpointing Problems and Solutions in Equity Method Accounting

Navigating the equity method’s winding road can lead to unexpected bumps, but with every challenge comes a chance to find a solution that keeps you on track. Pinpointing these problems early—like inconsistencies in measuring influence or interpreting joint control—helps you steer clear of possible missteps. The remedy might lie in more rigorous financial due diligence or enhanced communication with the investee to make sure that all parties are on the same page.

Accounting standards evolve to iron out these kinks, striving for clarity and comparability across financial landscapes. They aim to offer a map that leads away from ambiguity and towards a common understanding of what it means to have significant influence and how it should be reflected in your accounts.

Problems and solutions often revolve around:

- Recognizing and measuring the initial investment and subsequent profits, losses, and dividends.

- Ensuring consistent application of the equity method for subsidiaries, associates, and joint ventures, despite complex partnerships or fluctuating ownership percentages.

- Adhering to evolving accounting standards that seek to simplify and refine equity method reporting.

Equity vs. Cost: Choosing the Right Method for Your Investments

Choosing between the equity and cost methods is like picking a route on a financial road trip: each has its own scenery and speed limits. The equity method puts you on a dynamic highway, with your investment’s value changing in tandem with the investee’s fortunes. Each bump or climb in their profits reflects in your financial position. In contrast, the cost method is more of a scenic, steady route; your investment sits calmly on the balance sheet at its original cost, with only dividends to mark occasional milestones of income.

Understanding when each method should take the wheel comes down to the level of influence your investment commands: significant influence calls for the equity method, while a more hands-off approach sticks to cost accounting. Whichever path you choose, the destination is the same: a true and fair view of your financial involvement with another entity.

The choice hinges on:

- The degree of influence or control you wield over the investee.

- Financial reporting goals and the need for transparent reflection of your investment’s performance.

- Regulatory compliance and the appropriateness of each method based on your circumstances.

To recap, the equity method mirrors ongoing changes in investment value, while the cost method keeps it steady on the books. Considering both the pros and cons, each approach is best suited for different investment climates and objectives.

Best for the equity method:

- You have significant influence but not control over the investee.

- You seek a more accurate reflection of your financial performance tied to the investee’s outcomes.

- You’re ready to handle a more complex accounting process.

Top 5 features:

- Dynamic recognition of investee profits and losses.

- Dividends received reduce the carrying value rather than recognize income.

- Influence on the investee’s operational and financial policies.

- More rigorous application and disclosure requirements.

- Potential for enhanced investor decision-making and financial forecasting.

Five benefits:

- Provides a real-time financial picture aligned with the investee’s business cycles.

- Encourages active engagement and oversight in investee’s strategic direction.

- Improves the quality of financial information for stakeholders.

- Can lead to a more nuanced understanding of underlying asset values.

- May influence financial synergy and return on investment through strategic alignments.

Two cons:

- May introduce complexity and volatility into financial statements.

- Requires regular access to detailed financial information from the investee.

Best for: Investors seeking to materially influence an investee’s policies and decisions while getting a more precise view of their investment’s impact on financial performance. This method is not for the faint of heart—it demands diligent tracking and deep dive analyses.

Best for the cost method:

- You have a passive investment with no significant influence over the investee.

- You prefer simplicity and stability in financial reporting.

- You’re looking for a method that aligns with a hands-off investment approach.

Top 5 features:

- Investment recorded at historical cost.

- Dividends received recognized as income.

- Lesser ongoing paperwork and adjustments.

- Easier to apply and understand for those who are not accountants.

- Stability in investment carrying value unless impaired or sold.

Five benefits:

- Simplifies accounting procedures, making for a more straightforward reporting process.

- Offers stability in balance sheet presentation.

- Reduces the need for constant monitoring of the investee’s performance.

- Decreases the administrative burden associated with complex accounting.

- Makes for easier forecasting and financial analysis when influence is not a factor.

Two cons:

- Does not reflect the underlying economic realities of fluctuations in the value of the investee.

- Provides limited information about the potential upside or downside of the investment.

Best for: Investors who prefer a hands-off or diversified portfolio approach, prioritize accounting simplicity, and do not exert significant sway over the company in which they are investing.

By carefully weighing these considerations, you can effectively choose the accounting method that best fits your investment strategy and financial reporting objectives.

The Future Roadmap: Updates and Evolving Standards

Staying Ahead: Anticipated Changes to Equity Method Guidelines

As the financial terrain evolves, so do the norms that govern the accounting for equity investments. Staying updated on anticipated changes is not an option but a necessity for those who want to be ahead in the game. Professional bodies and regulatory agencies periodically revisit and revise the guidelines to bring more clarity and relevance to the equity method, aiming for a set of rules that echo with current business practices and investor needs.

Future updates may reflect a continuous push towards global harmonization of accounting standards, allowing for more consistent and comparable reporting across borders. They could also address common pain points, such as complexities in recognizing and measuring the initial cost and subsequent adjustments, or in identifying what exactly constitutes significant influence.

To be prepared for these anticipated changes:

- Keep tabs on discussions and publications from standard-setting bodies like the IASB and FASB.

- Attend seminars and webinars focused on recent and pending accounting updates.

- Engage with professional communities, joining forums and networks where changes and their implications are debated and demystified.

Global Perspectives: International Equity Accounting Considerations

When you step into the arena of international equity accounting, you’re playing on a global chessboard with various rules and moves. It’s a realm where the equity method is seen through the lens of different reporting standards, like IFRS or GAAP, and where one size doesn’t fit all. Accounting for international investments demands a nimble approach, as standards may dictate diverse treatments for recognizing influence, measuring investments, and responding to changes in the value of an investee.

Companies operating internationally must wrangle with conversion between different currencies, understanding local tax implications, and navigating cross-border regulatory landscapes. They must also be clued in on how political and economic factors in an investee’s home country could impact their investment and, accordingly, their accounting approach.

For a truly global perspective, consider:

- Differences between IFRS (International Financial Reporting Standards) and other domestic standards, like the US GAAP, and their impact on equity method application.

- Currency translation complexities and their effects on financial reporting.

- The influence of cross-border tax structures on dividends and profits from international equity investments.

Additional Tools for Expertise: Resources and Learning Aids

Expanding Knowledge: Further Reading and Educational Opportunities

Diving deeper into the intricacies of the equity method is akin to embarking on a learning odyssey. There’s a wealth of resources out there that can illuminate the path and turn complex accounting jargon into digestible insights. From in-depth books written by accounting gurus, scholarly articles unpacking the latest research, to online courses offering bite-sized lessons—the learning landscape is rich and varied.

Expanding your knowledge doesn’t just keep you compliant and informed; it sharpens your financial acumen, equipping you to make more strategic decisions. And in today’s rapidly changing business environment, continuous learning is your best buffer against the unknown.

Kick off your learning journey by exploring:

- Accredited accounting and finance courses that delve into equity method accounting.

- Webinars and workshops by professional bodies.

- Articles and newsletters offering updates on accounting standards and best practices.

Engaging with Experts: Conferences and Professional Development

Mingling with the mavens of accounting at conferences and seminars is not just about the coffee and canapes—it’s an investment in your professional development. These gatherings offer a platform to rub shoulders with experts and peers, where you can engage in rich dialogue, exchange ideas, and stay abreast of the latest trends and challenges in equity method accounting.

This engagement can help unravel complex issues, provide exposure to diverse perspectives, and foster relationships that can grow into valuable networks. Walking away from these sessions, you may find that you’re not only more conversant in equity accounting but also equipped with a broader toolkit to navigate its intricacies in your daily work.

For optimal professional development, seek out:

- National and international accounting conferences with dedicated sessions on equity method accounting.

- Specialized workshops and roundtables focusing on the latest developments in investment accounting.

- Continuing Professional Education (CPE) credits through structured courses and seminars.

Conclusion

The equity method is a crucial accounting approach used when an investor entity holds substantial influence or control over an investee, typically through significant stock ownership or equity interest. In circumstances where an interest surpasses 20%, the equity method becomes particularly relevant, allowing the investor to record their share of the investee’s profits or losses on their income statement. This accounting method requires meticulous alignment with current accounting principles and IFRS accounting standards, ensuring that asset acquisition and equity method work intertwine seamlessly within the transaction cycle. Proper guidance and consulting services can provide clarity on the nuances involved, such as the treatment of equity securities and goodwill.

Throughout the implementation of the equity method, accounting guidance is paramount to address challenges like basis differences or when equity method losses impact the investor’s financial position. Advisors often assess business valuation through the method’s lens, providing insights into potential amortization needs or the elimination of excess values. Moreover, when jurisdictions vary in their regulatory requirements, understanding the intricacies of any consultation or viewpoint becomes essential, with CPA journals frequently offering expert perspectives. Organizations must navigate tax accounting issues and the substitution of applicable methodologies where needed, ensuring compliance and aligning with stakeholder interests.

Advisor firms and entities using the equity method frequently engage in the interchange of best practices, maintaining license content availability to enrich understanding. Given the indicators of financial performance, such as earnings and liabilities, stakeholders can make informed decisions regarding asset disposition or investment realignment. Specialists in accounting principles advocate for the practical application of equity method guidance, emphasizing that investor entities should regard their equity interest as a significant asset within their financial strategy framework. This nuanced understanding highlights the importance of a comprehensive accounting guide on equity investments, enhancing decision-making across diverse transaction cycles.

FAQ Section

When Should the Equity Method Be Applied in Accounting?

The equity method should be applied when you have significant influence over an investee, typically interpreted as owning 20-50% of the entity’s voting rights. This approach is necessary for reflecting your share of the profits, losses, and changes in the investment’s value in your financial statements. It’s a method that suits an investor who isn’t merely a spectator but an active participant in the investee’s operational and financial policies.

How Does a Change in Ownership Percentage Affect Equity Method Accounting?

A change in ownership percentage can lead to a switch in accounting methods. If your stake surpasses the 20% threshold, you may need to start using the equity method, suggesting significant influence over the investee. Falling below that level could see a shift to the cost method, signaling a reduction in your sway. It’s all about whether your influence is deemed significant or not.

What Are Common Misconceptions About the Equity Method?

A common misconception about the equity method is that it reflects cash earnings from the investee, but it actually represents your share of their profits or losses, regardless of cash distributions. Another is that mere ownership of 20% of an investee automatically leads to equity method accounting, when significant influence must also be present. Additionally, some may wrongly assume that this method applies to control situations, which are actually handled under consolidation.

Where Can I Find Updates on Equity Accounting Practices?

Updates on equity accounting practices can be found through the websites of accounting standard-setters like the Financial Accounting Standards Board (FASB) or the International Accounting Standards Board (IASB). Publications, newsletters, and updates from professional accounting organizations, as well as accounting and finance journals, are also good sources for the latest information.

How does the equity method apply to investment in a subsidiary?

The equity method doesn’t typically apply to investments in subsidiaries. In accounting terms, a subsidiary is an entity over which the parent company has control, usually indicated by owning more than 50% of the voting rights. Such investments are accounted for using the consolidation method, where the parent company combines its financial statements with those of the subsidiary. The equity method is reserved for associate companies, where there’s significant influence but not control.