Key takeaway: They’re essentially holding onto the customer’s money while promising to provide the value at a later date. This is crucial for generating trust and ensuring customers that they will receive what they’ve paid for.

Importance of Understanding Deferred Revenue in Business Finance

Grasping the concept of deferred revenue is like having a secret roadmap to the health and promise of a business. It’s a beacon of a company’s obligations, showing that they must still deliver on services or products customers have splurged on in advance. Think of it as financial trail markers, reminding companies they can’t claim victory too early by recognizing this income straight away.

When you spot deferred revenue on a balance sheet, you’re peering into a business’s future workload and cash flow. It’s a real-time snapshot of the revenue that’ll be recognized down the line—once they’ve rolled up their sleeves and fulfilled their part of the deal.

Key takeaway: By understanding deferred revenue, businesses can strategically manage both their finances and operations, ensuring they don’t bite off more than they can chew. Plus, it paints a more trustworthy picture for investors seeking transparency in financial health.

KEY TAKEAWAYS

- Deferred revenue is considered a liability on a company’s balance sheet because it represents a payment received for goods or services that the company has yet to deliver, thus it reflects an obligation the company owes to its customers.

- Recognition of deferred revenue as actual revenue on the income statement only occurs once the related products or services have been delivered to the customer, adhering to accrual accounting standards.

- An increasing balance in deferred revenue can be indicative of a business’s growth, as it may show that customers are willing to pay upfront for services or products to be delivered in the future, but this also creates an obligation for the company to manage and meet customer expectations to sustain trust and satisfaction.

Recognizing Deferred Revenue in Financial Statements

Impact of Deferred Revenue on Income Statements and Balance Sheets

Deferred revenue wields a unique power to alter the landscape of a business’s financial statements. On the balance sheet, it’s like an IOU to customers that sits comfortably under liabilities. This spot is reserved for the profits they haven’t earned yet because they haven’t handed over the goods or services.

As time marches on and those promises are fulfilled, deferred revenue crosses over onto the income statement with a new identity: earned revenue. It’s a financial metamorphosis, transition from obligation to accomplishment. Picture it as an hourglass, with the grains of sand being the advance payments slowly trickling down to join the earnings as services are delivered.

Key takeaway: They need to keep a keen eye on this shift—from a liability that points to impending work to revenue signifying completed deals. It’s not just an accounting technique; it’s about keeping score the right way, reflecting a company’s genuine financial position and operational progress.

The Accounting Mechanisms Behind Deferred Revenue Recognition

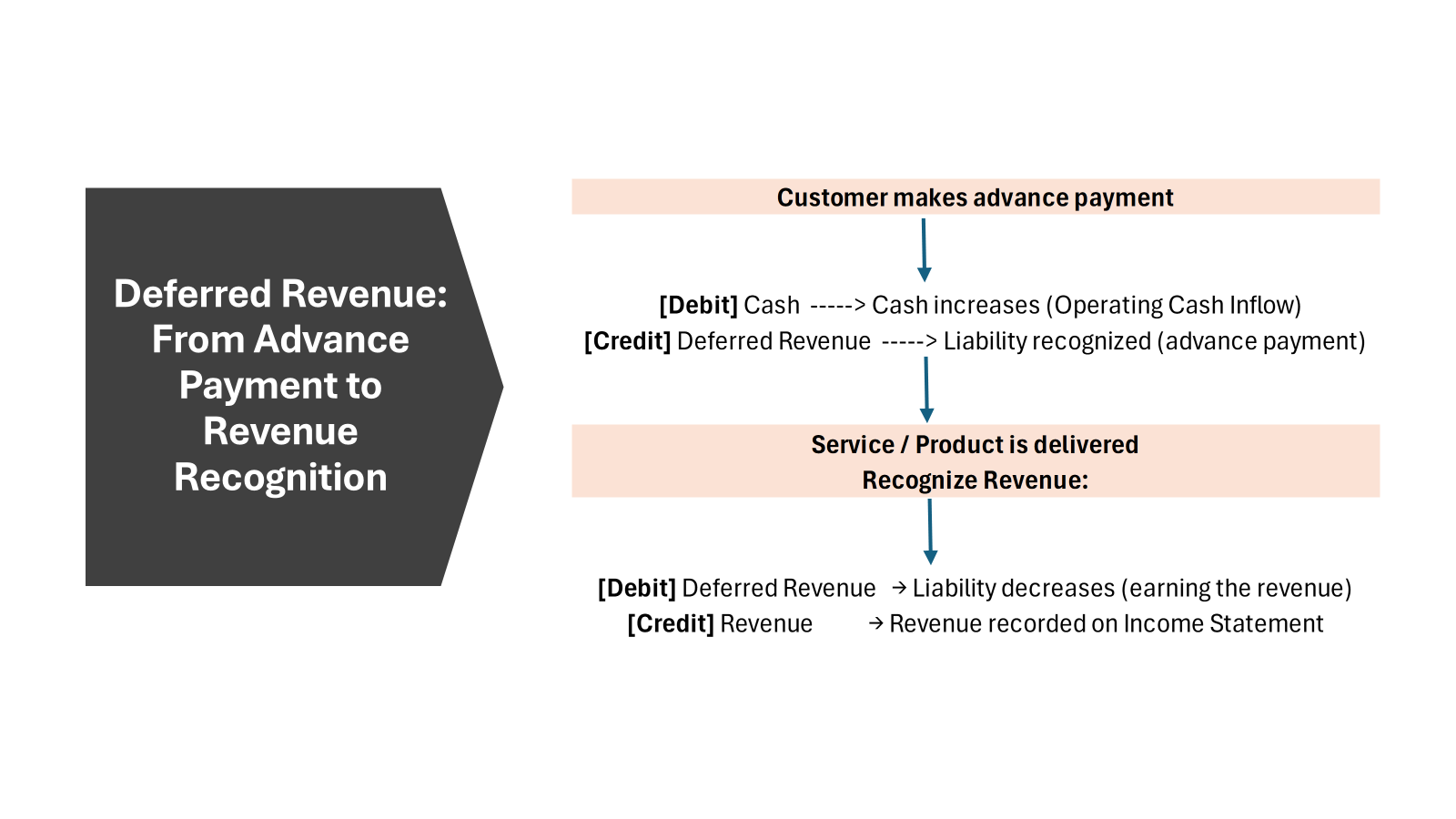

Unlocking the mysteries of deferred revenue recognition is akin to mastering a strategic financial dance. It all starts when they snag the payment in advance, which marks the entry into the balance sheet’s liability column as deferred revenue. No need to roll out the red carpet on the income statement just yet—this money isn’t ready for its debut.

Now, cue the gradual performance. As they serve up the product or dish out the service, they carve out portions of this reserve and shuffle it over to the income statement. This is the revenue’s grand entrance, and it’s orchestrated to match the exact slice of value they’ve provided, not a minute before.

Key takeaway: They must choreograph this process meticulously, with every step dictated by the principle that earnings are only recognized when they’ve truly earned them—keeping it all in tune with both legal and financial standards. This precision keeps them honest and their financial statements reflective of the real rhythm of their business operations.

Real-World Applications and Examples

Deferred Revenue in Different Business Sectors

Deferred revenue tiptoes into an array of business arenas, each with its unique flair. Subscription-based companies, such as those serving up monthly boxes of goodies or streaming services, often see their coffers swell with advance payments for services yet to be streamed or shipped.

Professional associations and private clubs collect membership dues upfront, promising to open the doors to exclusive benefits and events in the forthcoming periods. Meanwhile, insurance companies amass premiums with the vow of coverage over time, whereas real estate firms pocket rent, providing a roof over heads monthly.

Key takeaway: From tech companies with SaaS models to gyms pre-selling memberships, they all hold a stack of cash that’s not theirs to spend, at least not yet. They must deliver on their promises to convert that liability into earned revenue, making it crucial for each sector to handle deferred income with finesse. This ensures they fulfill their part of the bargain, maintaining customer satisfaction and legal compliance.

How Software Companies Treat Deferred Revenue

Software companies, especially those in the SaaS sphere, are masters of the deferred revenue game. They often reel in customers with annual or multi-year subscriptions, pocketing the cash upfront. But don’t be fooled — these aren’t instant gains. They must tiptoe along the tightrope, recognizing revenue as they gradually deliver software updates and support over the subscription period.

It’s like a promise etched in their ledger, with each software patch or customer support call chiseling away at the deferred revenue block. As they chip off bits of obligations and turn them into real, delivered services, they move from the liability column to the top-line revenue on the income statement, month by painstaking month.

Key takeaway: It’s a meticulous balance for software companies to maintain, ensuring they don’t overstate their financial performance while still showcasing the robust customer commitment they’ve secured. Proper treatment of deferred revenue ensures sustainability and demonstrates the company’s long-term commitment to fulfilling its contractual promises.

Navigating Deferred Revenue Challenges

Mitigating Risks Associated with Deferred Revenue

To nip potential pitfalls with deferred revenue in the bud, businesses must adopt a mix of vigilance and strategy. They need to ensure that their service and product delivery pipeline is as solid as a rock since any hiccup can erosion customer trust and potentially lead to refund demands, staining their reputation.

Tightening up internal controls is key—you might think of it as a financial immune system, guarding against errors and accidental revenue recognition. They also need to make sure their forecasting muscles are strong, allowing them to accurately predict when revenues will shift from deferred to earned, keeping their financial statements in tip-top shape.

Key takeaway: The goal is to have a clear view of their earning horizon, with systems in place to ensure no promised offering falls through the cracks. With this, they not only dodge risks but also stand as beacons of trust and reliability, crucial for sustaining good customer relationships and a robust business reputation.

Auditing Trials – Steering Through Deferred Revenue Hurdles

During audits, deferred revenue often transforms into a strenuous obstacle course. It’s an intricate web where every thread—the timing of revenue recognition, the exactitude of matching payments to services, and the clarity of records—must align flawlessly. Otherwise, they could be in for a nerve-wracking slog through documentation and backtracking.

To smooth out potential kinks, technology solutions like Stripe offer a golden lifeline. They bring traceability to the forefront, letting auditors connect every dollar of recognized or deferred income to the appropriate customer invoice and agreement. It’s a move that can shave hours off the audit process and inject peace of mind into what’s often a stress-laden endeavor.

Key takeaway: It’s absolutely essential for companies to handle deferred revenue with precision and transparency. This approach not only simplifies audits but also fosters a culture of accountability and diligence—a winning ticket for any business under the discerning eye of an auditor.

Revenue Recognition Standards and Guidelines

Staying Compliant with ASC606, IFRS15, and GAAP

Diving into the alphabet soup of accounting standards, ASC606, IFRS15, and GAAP stand as towering guides in the realm of revenue recognition. Companies need to get comfy with these guidelines as they dictate the ‘when’ and ‘how’ of turning promised future services into today’s revenues.

ASC606 and IFRS15, though with some differences, are like twins in their core principle: income must be recognized only when control of the goods or services passes to the customer. And the GAAP? That’s the sturdy fence keeping U.S. companies on the straight and narrow, ensuring every financial statement tells the unvarnished truth.

Key takeaway: It’s a complex dance, no doubt, but staying in step with these guidelines isn’t just about legal tick marks—it’s a trust pact with stakeholders. Companies wielding clear-cut policies and automated systems to manage these standards signal stability and integrity, crucial currencies in the realm of business finance.

Key Principles for Recording and Recognizing Deferred Revenue

When documenting deferred revenue, several fundamental principles come into play. First, it’s paramount to never jump the gun by including unearned income in their financial scorecard. They need to methodically record payments as they enter the scene, earmarking them as liabilities, signifying a promise to the customer that they are yet to fulfill.

Revenue recognition shouldn’t happen in a flash. It waits for the precise moment when they’ve delivered enough value to the customer to reasonably claim that cash as theirs. They must carefully quantify the progress in providing the service or delivering the product, giving them the green light to gradually shift funds from ‘deferred’ to ‘earned’ status.

Key takeaway: Adhering to these principles keeps their accounts balanced and truthful. It ensures every penny of revenue on their books has truly been made, not just anticipated. This meticulous tracking and recognizing of deferred revenue underscore their commitment to transparency and accountability in their financial dealings.

Illustrations: Journal Entries and Calculation Examples

Step-by-Step Deferred Revenue Journal Entry Example

Let’s break down a deferred revenue journal entry, step by step, with an example. Imagine Cloud Storage Co. bags a cool $1,200 from a new client for a one-year contract on August 1. Since they’ll dribble out the cloud storage services over 12 months, they can’t book the whole sum as revenue right away.

On day one, they cheerfully debit their cash account because their bank balance just got a boost. Simultaneously, they credit the deferred revenue account, acknowledging there’s work to be done before it’s really theirs to celebrate.

Each month’s end brings a mini celebration—another $100 of revenue earned. They debit the deferred revenue account, shrinking that liability, and credit the revenue account, finally shining a spotlight on the fruits of their labor.

Key takeaway: This systematic approach keeps their financial statements in sync with reality. They’re acknowledging their progress and painting an accurate picture of their earnings throughout the year. It demonstrates a keen grasp of the nuances of revenue recognition and sets them up for long-term financial health and credibility.

Calculating Deferred Revenue in Practice

Calculating deferred revenue is like piecing together a financial jigsaw puzzle, where each advance payment is a piece that doesn’t quite fit into the earnings picture yet. Here’s how it works: Imagine Premier Web Design Co. receives $6,000 for a project they’ll work on over 6 months. It’s not all about the immediate cash celebration—they need to divide that payment into parts that correspond with their progress.

With each passing month, as they weave their web design magic, they recognize $1,000 as earned revenue, dialing down the deferred revenue account by the same amount. It’s a linear process, ensuring no money is prematurely celebrated as income.

Key takeaway: Pinpoint accuracy in calculating deferred revenue keeps their financial statements honest and their decision-making grounded. It’s about being clear-eyed regarding their cash position versus actual earnings, which reflects their genuine financial pulse. This clarity is essential, particularly when planning for the future or discussing performance with stakeholders.

Tools for Effective Management

Leveraging Technology for Accurate Deferral Tracking

Embracing tech for deferral tracking is like trading a sundial for a smartwatch — the precision and efficiency leap is monumental. Automated deferred revenue software, like ScaleXP, snaps neatly into their accounting systems. Whether they’re using QuickBooks, NetSuite, or another platform, they’re getting a high-tech sidekick that does the heavy lifting.

These tools work tirelessly, helping close the month faster and generating automated, error-proof revenue recognition schedules. They’re not just about slashing time on mundane tasks; they unlock the ability to make sharper, data-driven choices and can turbo-boost company growth.

Key takeaway: For finance teams both small and mighty, investing in deferred revenue technology is like adding rocket fuel to their efficiency. It grants them a real-time, singular truth hub that catapults their decision-making from good to exceptional and cleans the slate of manual tracking errors.

The Role of Templates and Software in Simplifying Deferred Revenue Accounting

Templates and software in deferred revenue accounting act as the tireless sous chefs in the kitchen of finance, prepping the ingredients so they can focus on the gourmet meal — the bigger financial picture. They serve up pre-designed spreadsheets and automated systems, cutting down on the possibility of human errors that can scramble the financial eggs.

Templates are the starting blocks, guiding them through the correct accounting format and calculations. But software? That’s the jetpack, propelling their efficiency skyward. It syncs with bookkeeping systems, streamlines month-end closings, and makes adherence to revenue standards a breeze.

Key takeaway: By implementing these tools, finance teams can not only slice through complexity but also dish out spot-on financial statements with minimal fuss. It’s about applying simplicity and ensuring that even the novice bookkeeper can navigate the twists and turns of deferred revenue. It’s a no-mess, no-fuss approach to a typically messy part of accounting.

Advanced Insights for Finance Professionals

The Interplay between Deferred Revenue and Cash Flows

Deferred revenue and cash flows are like dance partners in the financial ballet of a business. Cash from advance payments might make their bank account seem flush, but don’t be misled — this isn’t a green light to spend freely. They must remember there’s an invisible string attached to that money, pulling it towards future obligations.

What they see as a cash flow surge today could be a drought tomorrow if not managed wisely. It’s not sprinting to the bank, but more of a measured marathon, where they need to keep pace with revenue recognition over time.

Key takeaway: Through disciplined monitoring of cash-to-revenue ratios and the magic of tools like revenue waterfall charts, they can sidestep the gauntlet of cash mismanagement. By locking in onto the long game, they can invest and spend in lockstep with their commitment to deliver to their customers, ensuring financial sustainability.

Strategies for Optimizing Deferred Revenue Reporting

Sharpening the deferred revenue reporting process is like tuning an instrument to hit the perfect note. One strategy is rolling out cloud-based accounting software, which streamlines reporting and updates in real time, keeping your finger firmly on the pulse of financial health.

Diving deeper, segmenting deferred revenue by product or service lines enhances visibility and helps in making more informed decisions. It’s also wise to set up reminders or triggers within their accounting system to review and recognize revenue, ensuring they avoid falling behind and misstating financials.

Key takeaway: Regular internal reviews and reconciliations fortify accuracy, strengthening their defense against compliance hitches. By embedding these strategies into their routine, they ensure that their reporting sings in harmony with business activities and financial commitments, hitting every note with precision.

Conclusion

Deferred revenue, often recognized as a liability on a company’s balance sheet, represents payments received for goods or services that have yet to be delivered. This concept is crucial within the realm of profitability and revenue recognition, as it directly impacts the way financial statements are prepared and analyzed. Commonly associated with prepayments and deposit deposits, deferred revenue requires careful attention from the accounting team to ensure accurate tracking and compliance with generally accepted accounting principles (GAAP). For instance, when a retail business receives cash inflow from sales invoices or retainer agreements for future services, this income is not immediately recognized as revenue but instead classified under deferred accounts until fulfillment.

Adopting the accrual method of accounting, firms allocate deferred revenue to actual revenue only when the associated goods or services have been provided. This practice not only aligns with GAAP but also aids in accurate business valuation, influencing overall corporate profitability. For instance, in scenarios such as newspaper subscriptions or rent payments, where prepayment terms are standard, understanding how to manage and transition from deferred revenue to recognized revenue is vital. Modern solutions, like revenue automation solutions, can streamline this process, helping businesses navigate the complex landscape of deferred accounts. Proper handling of deferred revenue supports a company’s long-term financial strategy by allowing for more precise valuation and robust financial health analysis.

FAQs: Answering Common Queries on Deferred Revenue

What is the meaning of deferred revenue?

Deferred revenue refers to payments received by a company for goods or services not yet delivered or performed. It’s booked as a liability because it represents an obligation to the customer and is recognized as revenue over time as the product or service is provided.

What are deferred revenues?

Deferred revenues are advance payments a company receives for products or services that it will provide in the future. They’re recorded as liabilities until the service or product is delivered and the revenue can be recognized.

Is Deferred Revenue an Asset or a Liability?

Deferred revenue is a liability because it represents a company’s obligation to deliver goods or services in the future for which it has already been paid. It remains a liability until the obligation is fulfilled and the revenue is earned.

Can You Have Deferred Revenue in both Accrual and Cash Basis Accounting?

In accrual accounting, you can have deferred revenue when you receive advance payments for services or products to be provided later. However, under cash basis accounting, deferred revenue isn’t applicable as revenue is recognized when cash is received, not when earned.

How Should a Company Record Deferred Revenue before Receiving Cash?

A company typically records deferred revenue upon receipt of cash as a liability. If the cash hasn’t been received yet but an agreement is in place, an accounts receivable would be recorded instead, until the cash is received and then transferred to deferred revenue.

What is the Difference Between Deferred and Recognized Revenue?

Deferred revenue is payment received for services or products yet to be delivered, recorded as a liability, while recognized revenue is earned income from delivered goods or completed services, reflected on the income statement as part of the company’s earnings.