KEY TAKEAWAYS

- Maintain a consistent approach by performing closing entry steps at the end of each accounting period—monthly, quarterly, or annually—to reduce the likelihood of errors and to ensure that financial records accurately reflect the company’s financial status.

- Streamline and scrutinize intercompany transactions, ensuring that revenues and expenses between related entities or departments are either eliminated or properly consolidated to avoid misrepresentation in consolidated financial statements.

- Utilize modern accounting software to automate and facilitate the closing entry process, which helps in carrying out accurate calculations, generating precise reports, and executing the steps of closing entries reliably.

Temporary vs. Permanent Accounts: The Accounting Cycle Contingent

Grasping the difference between temporary and permanent accounts is key to understanding the accounting cycle. Temporary accounts are like gusts of wind, present only for a season. They include revenues, expenses, and dividends, and their purpose is to track the financial comings and goings within a specific period. These categories are crucial for the process of identifying potential deductions during the financial year. Once that period concludes, these accounts are emptied, ready to capture fresh data with the start of a new cycle.

Permanent accounts, in contrast, are the sturdy oaks, steadfast year after year. They consist of assets, liabilities, including ignored accrued expenses as a form of permanent liability account, and most equity accounts entries that show the ongoing financial state of an entity. Their balances carry over into the next accounting period, providing a continual financial narrative. This highlights the inherent stability of equity account entries, which remain unaffected by closing entries and ensure the equity accounts reflect the long-term financial health of the business. By resetting temporary accounts and retaining the balances of permanent ones, businesses ensure that each period’s books begin with a clean slate while tracking the progress of cumulative deductions over time.

Navigating Through the Steps of Making Closing Entries

Starting with Income and Expenses: The Role of the Income Summary Account

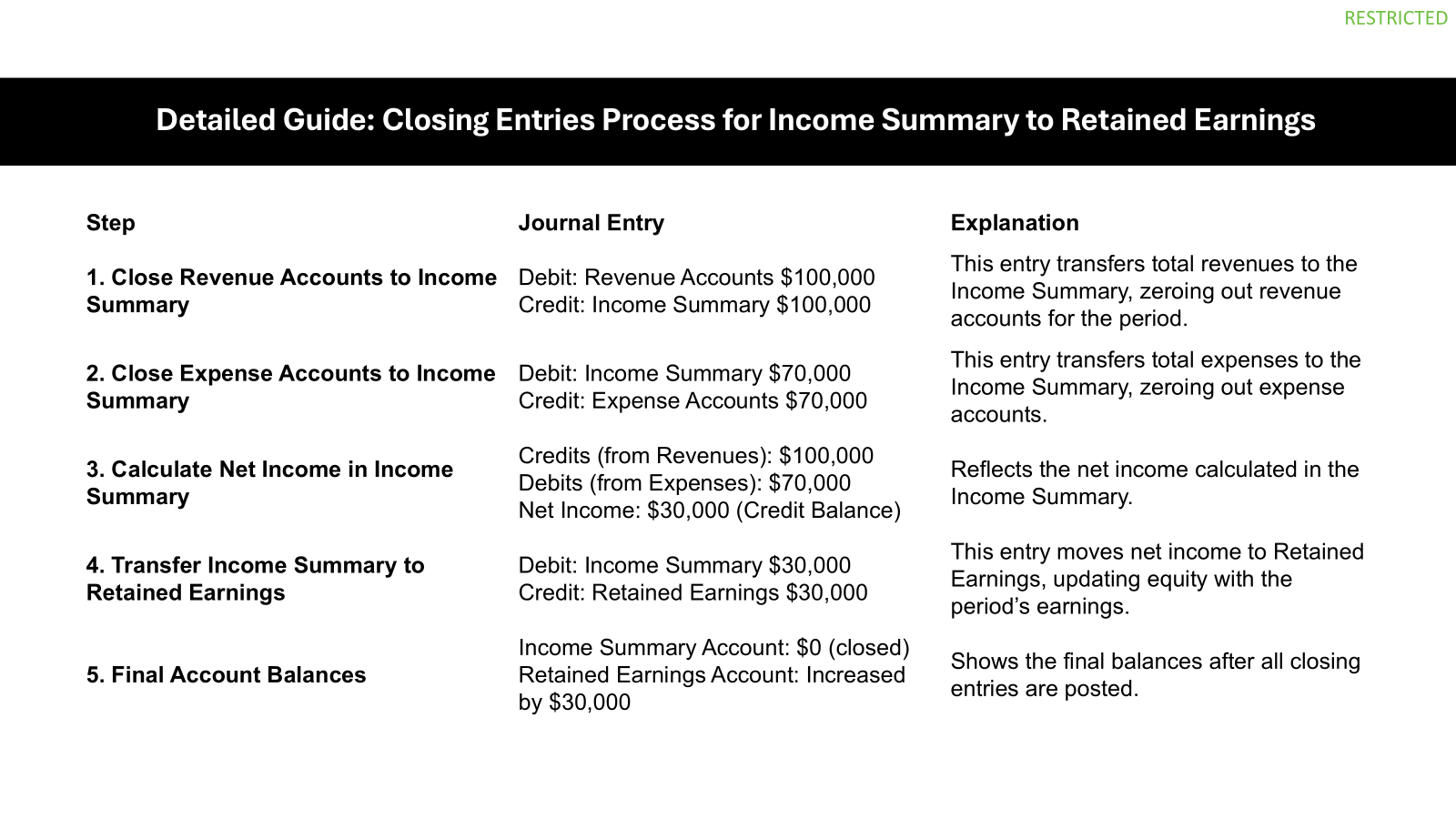

The Income Summary account is the unsung hero in the world of accounting. It’s not often mentioned outside of the closing process, but it plays a crucial intermediary role. Imagine a vessel, collecting the essence of an entire period’s worth of buzzing activity – every sale, every expense. To ensure your financials accurately represent your business activity, the Income Summary account is essential. This is where you’ll transfer all the revenues and expenses, a process that simultaneously resets your income and expense accounts to zero for the new period, similar to taking a snapshot of your financial health.

Why is this important, you ask? The contents of the Income Summary reflect the net performance of the business – essentially, they spotlight whether you’ve grown your debit revenue and turned a profit, or incurred a loss during the period. It’s the moment of truth that not only closes out temporary accounts but also sets the stage for transferring this net balance into the grander realm of the balance sheet – specifically, into the Retained Earnings account, a symbol of the company’s cumulative vigor. By examining a post-closing trial balance snapshot, all temporary accounts such as revenue and expenses can be confirmed reset to zero, providing a clear and accurate starting point for the new period.

The Shift to Retained Earnings: Completing the Circle

The finale of the closing entries saga is the transfer from the Income Summary to the Retained Earnings account. If your company has been successful, and expenses haven’t swallowed up your revenues, you’ll see a net profit looking back at you from the Income Summary account. It’s a triumph, and where does this victory march? Straight into the Retained Earnings account, reinforcing the financial foundation of the company. Keep in mind, one of the practical takeaways is consistency in this process to maintain accuracy in your financial records. The retained earnings are calculated after taxes have been accounted for, which are a critical financial consideration for any business.

But it’s not always a victory parade. Sometimes, the reverse is required. If the period incurred a loss, the Retained Earnings account must nobly absorb the impact, ensuring that the loss is reflected in the equity of the company. Once this important shift is accomplished, your ledger is primed and polished for the upcoming period, and you start anew, applying one of the vital takeaways—closing entries steps performed consistently.

And dividends, if there are any, follow suit in this rite of passage to the Retained Earnings account. They get deducted, representing the share of profits distributed to the shareholders, again affecting the overall equity of the company. Remember, dividends are paid out from net income after taxes, thus affecting the amount transferred to Retained Earnings. It’s a cyclical journey—starting with transactions, passing through the Income Summary, and ending in Retained Earnings, ready to begin anew. This process ensures that each accounting period is discrete and manages to accurately portray the company’s financial story over time.

Closing Entries in Different Business Structures

Impact on Corporations: Dividends, Retained Earnings, and Beyond

When a corporation declares dividends, they essentially announce a payout from the profits to the shareholders – a gesture of sharing the economic spoils. As detailed in sources like Investopedia, the declaration sees Dividends Payable jumping up in the liabilities section, and a simultaneous dip in Retained Earnings, which reflects in the equity part of the balance sheet. This transaction doesn’t require a traditional closing entry because it’s already subtracted from Retained Earnings at the declaration.

However, when inventory and other assets are involved, it is essential to apply the latest inventory cost methods, such as FIFO or LIFO, waiting on the broader harmonization under IFRS reviews. In scenarios where a separate Dividends account has been in use during the period, this temporary account is swept clean at year-end. According to best practices outlined on learning platforms including Investopedia, the balance is moved to Retained Earnings, reducing the account by the total dividends paid. This vital adjustment reflects the accrual accounting’s core principle of accurately recording transactions, maintaining the integrity of the closing entries process. It keeps the financial statements coherent, showing exactly how much of the profits are plowed back into the company, and how much is given back to investors. It’s a delicate balance that corporations must manage – supporting growth and rewarding investment, all shown transparently thanks to closing entries. Notably, the amount remaining in Retained Earnings is crucial, as it often represents the corporation’s capacity to fund expansion, innovation, or debt repayment, thus influencing future strategic decisions and investor perceptions.

For Sole Proprietorships and Partnerships: Withdrawals and Capital Accounts

In the realm of sole proprietorships and partnerships, drawing accounts are integral. They track the amounts the owner or partners withdraw for personal use throughout the year. But unlike corporate dividends, these withdrawals don’t touch retained earnings; they directly impact the proprietor’s or partners’ capital accounts, relying heavily on the expertise of the individual managing the funds. To manage these financial processes effectively, participating in a reputable accounting course can provide invaluable knowledge and skills.

As you wave goodbye to the accounting period, you, the business owner, must reconcile any withdrawals. To clean the slate, the balance of the drawing account is transferred to the capital account, decreasing its balance. Learning how to navigate these transactions is a key concept in any comprehensive accounting course. In a sole proprietorship, it’s the singular capital account that adjusts. For partnerships, each partner’s drawing account is closed to their individual capital account.

This reflects a decrease in the business’s equity, vis-à-vis the owner’s capital, due to personal use of funds. It’s a fundamental distinction from corporations, emphasizing the closer relationship between personal finances and business equity in smaller businesses. Making accurate closing entries for these accounts is essential: according to the expertise gathered by HighRadius through a survey of seasoned accountants, they ensure personal expenditures don’t muddle the business’s financial clarity and remain transparent for all stakeholders.

Best Practices for Accurate Closing Entries

Timeliness and Order: Prioritizing Adjusting Over Closing Entries

You know the saying, timing is everything? Well, in accounting that speaks volumes, especially when it comes to prioritizing adjusting entries over closing entries. Adjusting entries, an essential component of account reconciliation, are like your meticulous preparations before a play – you’re setting the stage, getting the lighting right, and ensuring every actor knows their cues. They ensure that the financial statements reflect the true income and expenses that belong to the period, which is crucial for precise account reconciliation.

Now when the curtain falls, closing entries waltz in for the finale – they’re the stagehands who reset everything after the performance. By closing out revenue and expense accounts, they prep the books for the new accounting period, making sure you’re not mixing scenes from two different plays.

The timeliness of these processes is crucial. You want to avoid the financial confusion of having last period’s numbers overstaying their welcome. Adhering to this order – adjusting then closing – ensures your financial narratives don’t become tangled and that every period’s reporting is as crisp as a freshly printed playbill.

Enhanced Financial Clarity: Automated Solutions and Advanced Techniques

Imagine applying the power of fintech to transform the tedious chore of closing entries into a sleek, automated process. With the advent of cutting-edge accounting software, the laborious task of manual tallying is becoming a thing of the past. These sophisticated tools use advanced algorithms to categorize income and expenses, match transactions, and prepare the closing entries with precision – all with just a click and at the speed of electrons.

In the realm of accounting management, this wave of automation not only expedites the process but also significantly slashes the risk of human error – say goodbye to missing a zero or misplacing a decimal point. They provide crystal-clear financial insight, akin to high-definition glasses for your ledger, allowing you to detect trends, issues, and opportunities with unparalleled clarity.

The benefits extend beyond basic efficiency. Implementing an automated solution means bidding adieu to the risks of negligence or fraud tarnishing your financial records. It’s a solid bulwark strengthening accounting controls. And the icing on the cake? These advanced techniques impart peace of mind, liberating precious time for strategic thinking and decision-making – a definitive triumph for any finance team.

Real-World Examples and Tips to Ace Closing Entries

Common Scenarios: From Revenue to Owner’s Equity

Understanding the accounting basics can significantly clarify this process. For instance, let’s suppose you’ve had a productive year – your revenues exceed your expenses, leaving you with a commendable net income. Navigating the realm of closing entries in such instances is crucial for accurate financial reporting, and for those delving deeper, exploring a comprehensive list of FAQs on the subject might prove beneficial. This common scenario exemplifies the basics of closing entries, which involve crediting all revenue accounts to transfer their balances to the Income Summary account. Then, you debit the expenses, once again directing the balance to Income Summary, which now reflects your net income.

The next step is a gratifying one: You debit the Income Summary for the total net income, a move that zeroes out this account. A corresponding credit is made to the Owner’s Capital account (or Retained Earnings in case of a corporation), thus increasing the owner’s equity.

Conversely, if faced with a net loss, the Income Summary would be credited and the Owner’s Capital account debited, reflecting the decrease in equity. It’s a classic example of accounting symmetry, tying the ebbs and flows of your financial activities directly to your business’ worth. In this context, a well-maintained FAQ section can be a valuable resource for those new to these concepts, ensuring they understand the impact of these transactions on owner’s equity. These entries, simple on the surface, uphold the integrity of your financial statements, ensuring the owner’s equity accurately captures the business’s actual performance.

Employing Accounting Software: A Step Towards Modern Efficiency

Stepping into the era of modern efficiency for closing entries means embracing accounting software with open arms. This isn’t just about keeping up with the times – it’s about transforming the entire close process from a complex chore into a straightforward task. By integrating a journal entry management module, as found in the Highradius suite, organizations can automate the creation and management of journal entries, drastically increasing efficiency. Employing tools like QuickBooks, Xero, or Zoho Books, you’ll find they automate the entire affair, reducing the risk of errors and inconsistencies with the support of a pre-filled template, which ensures up to 95% journal posting automation.

Now, consider the advantages – software like this can take a load of data, apply predefined rules, and generate closing entries without breaking a sweat. Revenues and expenses find their way to the right places, calculations are double-checked by the system, and the end result is a set of financial statements that align with established accounting principles. Businesses big and small can benefit from such automation as it not only streamlines processes but also gives back time – time that can be invested in growth and strategy, making it a smart move for anyone aiming for a competitive edge.

Closing Entries’ Role Across Accounting Periods

Ensuring Consistency: The Chain Effect from One Period to the Next

Ensuring consistency with closing entries isn’t just about good technique; it’s about setting a steadfast standard that runs through the entire fabric of financial reporting. When you start temporary accounts at zero at the beginning of each period, you’re executing the financial equivalent of “clearing the stage” for a new act. This is crucial for correct financial trajectory tracing because it prevents the mix-up of income, expenses, and dividends across periods – kind of like making sure you don’t carry over scenes from one movie to the next.

Such consistency feeds into the accuracy of comparative analysis. Imagine comparing two periods side by side; the figures should represent their respective slices of time without overlap or gaps. This chain effect underscores the importance of sticking to a routine closing process and applying the same methods each time. It’s a discipline that creates a clearer, more comprehensible financial narrative, leading to better-informed decisions in the subsequent periods.

Additionally, for any further clarifications, a thorough FAQ section can guide through common queries regarding the closing entries process, helping to reinforce understanding and aiding in consistent application.

Auditing and Compliance: The Critical Impact of Accurate Closing Entries

When it comes to auditing and compliance, accurate closing entries aren’t just important, they’re the linchpin of financial integrity. Get them right, and an auditor’s job becomes a smooth operational review; mess them up, and you could find your business in a quagmire of regulatory quandaries.

Accurate closing entries ensure that there’s no question about the legitimacy of your financial statements. They provide auditors and stakeholders with a clear trail of the company’s financial activities and confirm that you’re playing by the rules, from the IRS to the SEC and the GAAP standards. When auditors see that your figures match up across the board—showing no discrepancies between ledgers and statements—they know they’re working with a company that values precision and takes compliance seriously.

Being compliant also means that your business avoids costly penalties and enjoys an upstanding reputation in the market. Whether it’s a routine audit or a surprise check from the authorities, with accurate closing entries, you’ll have nothing to fear. They are your financial world’s safety net, ensuring that every act in your business’s ongoing economic play is above board.

FAQ on Understanding & Making Closing Entries

In Which Journal Are Closing Entries Typically Recorded?

Closing entries are typically recorded in the general journal, also known as the book of original entry. It’s here that all closing entries begin their journey, ensuring that your revenues, expenses, and dividends have their balances zeroed out and transferred to permanent accounts properly for the next accounting cycle.

Can Sophisticated Accounting Software Simplify the Process of Closing Entries?

Absolutely, sophisticated accounting software can significantly simplify the process of making closing entries. Programs like QuickBooks and Xero automate the steps, ensuring accuracy and consistency, which saves time and reduces human error. They’re designed to make the closing process more reliable and efficient.

What Are the Frequent Challenges Faced During the Closing Entry Process?

During the closing entry process, common challenges include ensuring accurate recording of transactions throughout the period, staying updated with the latest accounting standards, and reconciling all accounts before closing. Additionally, complex intercompany transactions and human error can complicate matters, potentially leading to misstated financial reports.