KEY TAKEAWAYS

- Available credit refers to the amount of money you can currently borrow from a revolving charge account, like a credit card, calculated by subtracting the sum of your unpaid charges and any pending charges from your total credit limit.

- Monitoring your available credit is crucial to avoid overspending and exceeding your credit limit, which can result in declined transactions or penalties, such as increased interest rates.

- A high level of available credit relative to outstanding debt on a consumer’s credit report is viewed favorably by lenders and creditors as it indicates responsible borrowing behavior.

The Importance of Understanding Your Finances

Financial literacy is the cornerstone of a secure economic foundation. Comprehending available credit is instrumental for anyone wishing to navigate the world of personal finance with confidence and savviness. When you understand your finances, you are equipped to make informed decisions that align with both short-term necessities and long-term ambitions. This knowledge allows for strategic planning, helping to avoid costly mistakes such as overspending or accumulating unmanageable debt. Additionally, a clear grasp of financial concepts like available credit can lead to better money management, eventually opening doors to opportunities for investment and wealth growth.

The Essence of Available Credit

Defining Available Credit in Simple Terms

Available credit can be considered your financial breathing room on a credit card or revolving charge account. It’s defined as the amount of money you can currently borrow without hitting your credit limit. To calculate this figure, you simply subtract your total outstanding balance — that is, the sum of your unpaid charges— from your credit limit. Keep in mind, pending transactions that act as holds on your account must also be subtracted, as they temporarily reduce your available credit even before they’re fully processed.

How Available Credit Differs from Credit Limit

While they are related, available credit and credit limit represent two different figures within your financial landscape. The credit limit is the maximum amount of credit a lender has agreed to extend to you. It’s the ceiling beyond which you cannot borrow without facing consequences such as over-limit fees or declined transactions.

Available credit, on the other hand, is dynamic. It represents the unused portion of your credit limit at any given moment. Think of your credit limit as a full water tank and your available credit as the remaining volume of water after some has been drawn out. As you make purchases, your available credit diminishes; when you make payments, it replenishes up to the cap set by your credit limit.

Understanding these differences sheds light on your spending power and potential to accrue debt and impacts credit utilization — a critical factor in credit scoring.

How Available Credit Impacts Your Financial Health

The Role of Available Credit in Credit Utilization

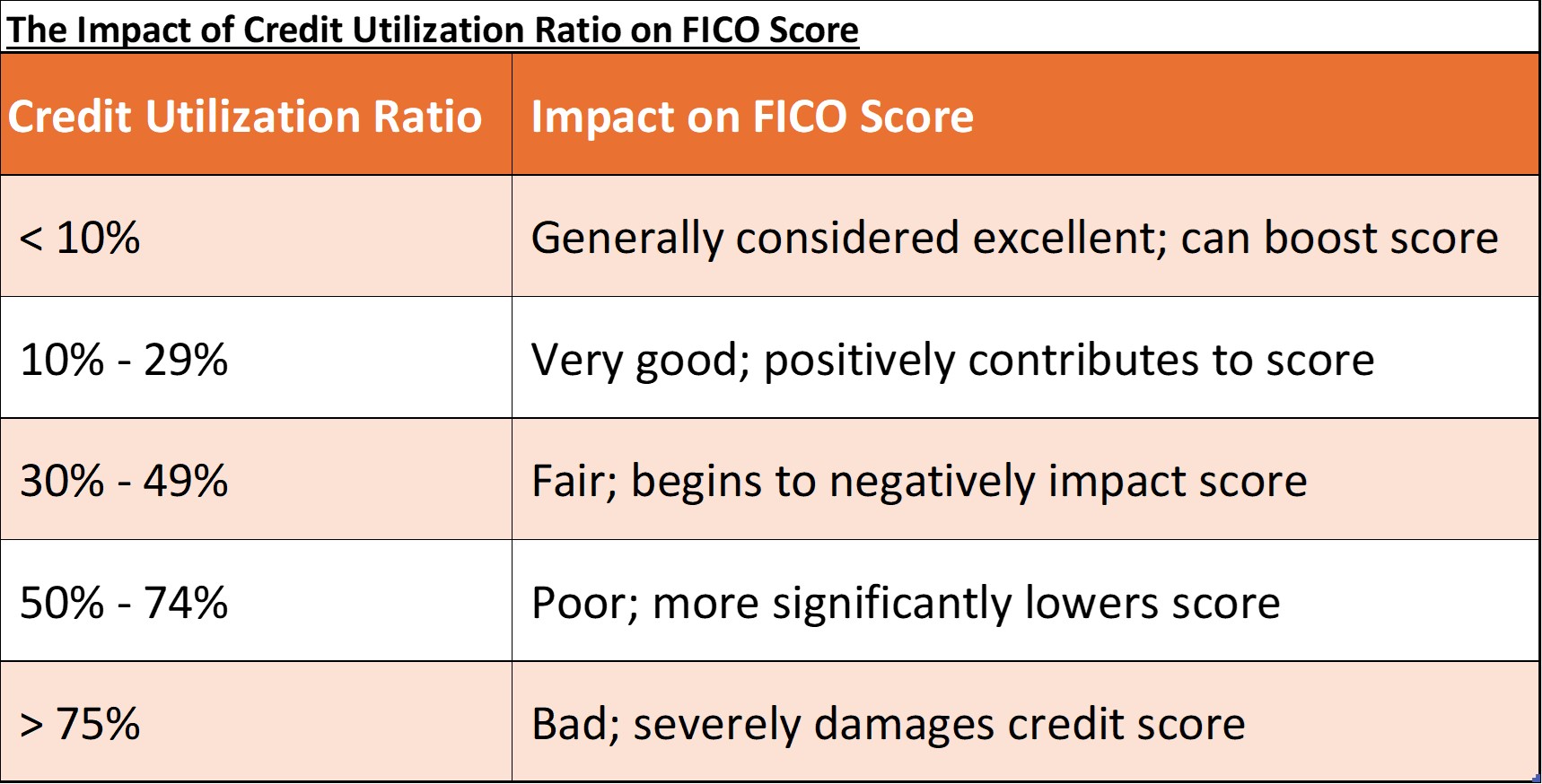

Available credit plays a pivotal role in the calculation of your credit utilization rate, serving as a key meter of your credit use. Credit utilization is the ratio of your current credit card balances to your credit limits, expressed as a percentage. It is a critical component in the mathematics of credit scores, accounting for a substantial portion — approximately 30 percent — of your FICO score.

To figure out your utilization rate, divide the total amount you owe across all credit cards by your total credit limit. For example, if your combined credit card balances are $3,000 and your total credit limit across all cards is $10,000, your credit utilization rate would be 30%. Financial experts recommend keeping this ratio below 30% because it signifies to potential lenders that you’re not overextending yourself and can manage credit wisely. Having a lower credit utilization rate typically indicates better creditworthiness and can positively influence your credit score.

Your available credit therefore acts inversely to your utilization: as available credit drops, utilization climbs. Maintaining a considerable amount of available credit can help keep your utilization low, which can lead to a healthier credit score.

The Relationship Between Available Credit and Your Credit Score

Understanding the relationship between available credit and your credit score is essential as it influences how lenders perceive your credit risk. As your available credit decreases, it suggests that you are using a higher portion of your credit limit, leading to an increase in your credit utilization ratio. High credit utilization can act as a red flag to lenders and credit scoring models, indicating that you may be over-leveraged or at potential risk of financial strain.

Conversely, maintaining a larger amount of available credit typically indicates a lower credit utilization ratio, which is generally viewed favorably by credit scoring models like FICO. For instance, if a consumer consistently maintains a credit utilization ratio below 30%, it signals to potential lenders that they’re managing their credit responsibly. This responsible management, in turn, can lead to a higher credit score.

Thus, your available credit is a key variable affecting your credit score. The way you manage it not only reflects your current financial health but also impacts your ability to obtain favorable rates for future loans or higher credit limits. It’s a balancing act where the goal is to responsibly manage both your debt and the credit that’s available to you to maintain an optimal credit score.

Navigating Available Credit Responsibly

Strategies for Managing Your Available Credit

Effectively managing your available credit requires a strategic approach to ensure you maintain a healthy financial profile. Here are some strategies you can implement:

- Track your spending: Regularly monitor your credit card accounts to stay aware of how much credit you’ve used. This will help you avoid maxing out your credit cards and keep your credit utilization rate low.

- Pay your bills on time: Late payments can hurt your credit score. Setting up automatic payments or creating calendar reminders can help ensure you never miss a due date.

- Pay more than the minimum: If possible, pay off your entire balance every month to avoid interest charges and reduce your credit utilization ratio.

- Manage your credit limits: Don’t be tempted to spend more just because you have a high credit limit. Maintain discipline in your spending habits regardless of your available credit.

- Request credit limit increases: If you have a good track record, you can ask your credit card issuer for a higher limit. This can immediately lower your credit utilization rate, as long as you don’t increase your spending.

- Balance multiple credit cards: If you have multiple credit cards, spread your purchases across them, and aim to keep the utilization rate on each card low.

- Avoid closing old accounts: Keeping older accounts open can benefit your credit score by increasing your overall available credit and contributing to a longer credit history.

- Strategically open new accounts: Only apply for additional credit if it makes sense for your financial situation. Opening new accounts can increase your total available credit but be mindful of the potential impact on your credit score from hard inquiries.

- Keep an eye on your credit score: Regular check-ups will help you understand how your credit utilization and other factors are affecting your score.

Remember, sage management of available credit isn’t about having access to funds you don’t need to spend; it’s about demonstrating to lenders that you can handle the credit you have responsibly.

Tips on Keeping a Healthy Level of Available Credit

Maintaining a healthy level of available credit is crucial for a good credit score and overall financial wellbeing. Here are some tips to help you achieve this balance:

- Monitor Your Spending Habits: Be mindful of how much you’re charging to your credit cards. Aim to spend well below your credit limits to keep a plentiful amount of available credit.

- Stay Below the 30% Threshold: Many experts advise keeping your credit utilization — the percentage of your credit limit that you’re using at any given time — below 30%. This can be beneficial for your credit score.

- Set Balance Alerts: Consider setting up alerts with your credit card issuer to notify you when you’re approaching a self-imposed spending limit.

- Make Multiple Payments: If you find yourself approaching your credit limit, consider making more than one payment in a billing cycle to free up available credit.

- Prioritize Debt Repayment: Work on a strategy to pay down existing debt, which can increase your available credit by lowering your balances.

- Limit New Accounts: While new accounts can increase your total available credit, they can also lower your average account age and potentially ding your credit score. Open new accounts sparingly.

- Adjust Your Credit Limits: If you have an excellent track record with your lender, consider requesting a credit limit increase which can elevate the amount of available credit. But remember, higher limits should not encourage higher spending.

By employing these tips and keeping a sharp eye on both your spending and repayment habits, you can maintain a healthy level of available credit, which in turn supports a strong credit profile.

The Consequences of Mismanaging Available Credit

What Happens When You Exceed Your Available Credit?

Exceeding your available credit means you’ve surpassed the credit limit set by your lender, and this can lead to various negative outcomes:

- Declined Transactions: Your credit card issuer may simply decline any further transactions until you’ve paid down your balance sufficiently.

- Over-the-Limit Fees: Some issuers might approve the transaction but charge you an over-the-limit fee, adding to your debt.

- Penalty Interest Rates: You may be subject to penalty APRs, which are higher interest rates applied to your balances, increasing the cost of any outstanding debt.

- Lower Credit Score: Going over your limit can harm your credit score since it signals to credit bureaus that you’re struggling to manage your credit responsibly.

- Reduced Credit Line: Your issuer might reassess your creditworthiness and decide to reduce your credit limit, which can further affect your utilization ratio and hence your credit score.

- Loss of Reward Points: In certain cases, exceeding your credit limit could lead to the forfeiture of points or rewards earned during that billing cycle.

To avoid these consequences, it’s advisable to pay close attention to your credit card balance relative to your limit, and take immediate steps to address any over-limit situation by making a payment or contacting your issuer to discuss your options.

Understanding the Risks of Low Available Credit

Low available credit, which is the result of high credit utilization, poses several risks that can affect your financial health and flexibility:

- Higher Credit Utilization Ratio: As one of the major components influencing your credit score, a high utilization ratio (indicative of low available credit) can lead to a decrease in your credit score.

- Potential for Declined Transactions: With minimal available credit, you’re at risk of having transactions declined, which can be embarrassing and inconvenient, especially in situations where it’s crucial to make a purchase.

- Difficulty in Financial Emergencies: Low available credit limits your ability to cover unexpected expenses, such as medical emergencies or urgent car repairs, potentially putting you in a difficult financial spot.

- Reduced Creditworthiness: Lenders and credit issuers view low available credit as a sign that you may be over-relying on credit, making you appear to be a higher-risk borrower. This can affect future credit approvals and the terms of new credit lines, such as interest rates and credit limits.

- Challenge in Managing Cash Flow: Without sufficient available credit, you may find it hard to manage cash flow gaps when awaiting paycheck deposits or other forms of income.

- Increased Financial Stress: Constantly operating close to your credit limits can create anxiety and stress due to the potential for fees, penalties, and declined transactions.

Understanding these risks should underscore the importance of managing your credit well and keeping an eye on your available credit to ensure it stays at a healthy level.

Enhancing Your Credit Strategy

When and Why to Increase Your Available Credit

There are several scenarios when increasing your available credit might be a strategic financial move:

- Improving Credit Utilization Ratio: Increasing your available credit while maintaining or reducing your balances can lower your credit utilization ratio, which may positively affect your credit score.

- Financing Large Purchases: If you’re planning a significant purchase that you can responsibly pay off, a higher credit limit can provide the necessary funds without negatively impacting your utilization ratio.

- Preparing for Emergencies: More available credit can provide a safety net for unexpected expenses, reducing the need to take out high-interest loans or dip into savings.

- Expanding Business Operations: Business owners often need to increase their available credit to invest in growth opportunities or manage cash flow effectively.

- Taking Advantage of Rewards: If you’re a diligent payer and seek to leverage credit card rewards without incurring debt, more available credit can afford you this luxury without harming your credit score.

However, it is crucial to consider increasing your available credit only if you have a disciplined approach to spending and are confident in your ability to manage additional credit without accruing debt. Responsible usage is key to ensuring the benefits outweigh the risks.

Balancing Credit Increases with Financial Stability

Successfully managing increased available credit requires a fine equilibrium with your overall financial stability. Here are some guiding principles to consider:

- Assess Your Financial Habits: Before seeking a credit increase, evaluate your budgeting and spending habits to ensure you can handle additional credit without overspending.

- Maintain or Improve Financial Discipline: A credit increase should not be seen as an opportunity to spend more. Continue to use credit cards strategically and pay off balances in full, if possible.

- Understand Your Needs: Determine the reasons for a credit increase. Is it to improve your credit utilization ratio or to cover a planned expense? Ensure the increase aligns with sound financial planning.

- Evaluate the Timing: Spacing out credit applications is beneficial since too many hard inquiries in a short period can negatively impact your credit score. Time your credit limit requests to minimize this risk.

- Read the Fine Print: Sometimes, increasing your credit may come with stipulations, such as a potential interest rate increase. Review any terms and conditions associated with a higher limit.

- Build an Emergency Fund: Instead of relying solely on credit, establish a savings buffer. An emergency fund can reduce the need to use credit for unexpected expenses.

- Check Your Credit Score Regularly: Monitoring your credit score and report will help you understand the implications of a credit limit increase and keep tabs on your financial health.

Balancing these factors can help ensure that your credit increases contribute positively to your financial stability rather than encouraging unsustainable debt accumulation.

Frequently Asked Questions (FAQs)

Can I Use All My Available Credit Without Consequences?

While you technically can use all your available credit, doing so may have unintended consequences:

- High Credit Utilization: Using all of your available credit can spike your credit utilization ratio, which might negatively affect your credit score.

- Risk of Penalties: If any additional fees or charges push your balance over the limit, you could incur over-the-limit fees or other penalties.

- Reduced Flexibility: Maxing out your credit line leaves you with no cushion for emergencies or unforeseen expenses.

- Increased Debt: Utilizing all available credit can lead to larger balances that may be harder to pay off, especially if you can’t pay the full amount by the due date and start accruing interest.

- Potential of Minimum Payment Trap: If you’re only able to make the minimum payment on a maxed-out card, you could end up in a cycle of debt due to accumulating interest.

It’s generally advisable to use credit cards strategically and maintain a significant margin of available credit to avoid these adverse outcomes. It’s beneficial to stay well below your credit limits and pay off balances in full each month whenever possible.

What Should I Do If My Available Credit Is Decreasing?

If you notice a reduction in your available credit, it’s important to take proactive steps to manage the situation:

- Review Your Spending: Analyze recent transactions to better understand why your available credit is decreasing. Identify areas where you can cut back.

- Pay Down Balances: Start paying off your debt, aiming to pay more than the monthly minimum to reduce your credit utilization ratio and free up available credit.

- Budget Adjustment: Revisit your budget to allocate more funds towards debt repayment and prevent further increases in your balance.

- Restrict New Charges: Avoid making new charges on your card until you’ve regained a comfortable margin of available credit.

- Monitor for Fraud: Ensure that the decrease in available credit isn’t due to unauthorized use of your account. Immediately report any suspicious activity to your credit card issuer.

- Communicate with Creditors: If you’re facing financial difficulties, contact your creditors to discuss possible solutions or adjustments to your credit terms.

- Consider a Balance Transfer: If high interest is contributing to your decreasing credit, explore balance transfer options to cards with lower rates or promotional periods.

- Seek Professional Advice: If managing your debt becomes overwhelming, consider seeking advice from a financial advisor or credit counselor.

Taking these steps can help arrest the decline in available credit within the banking sector and set you on a path towards restoring your financial health.

Can I spend my available credit?

Yes, you can spend your available credit as this is the amount you’re currently able to borrow on your credit card. Your available credit is the difference between your credit limit and your current balance, including any pending charges. However, it’s important to be mindful of the ramifications of approaching your credit limit.

Spending all your available credit can lead to high credit utilization, which may negatively impact your credit score. It can also leave you without any credit for emergency situations and potentially lead to accruing high-interest debt if you’re unable to pay off the full balance.

As a best practice, it’s recommended to keep your credit utilization ratio below 30% to maintain a good credit score and ensure financial flexibility. Therefore, while you can spend your available credit, it’s advisable to do so judiciously and within the boundaries of responsible financial management.

Why is my available credit low?

Your available credit may be low for several reasons:

- High Outstanding Balances: If you have charged a significant amount to your credit card and have not yet paid it off, your balance will be high, which in turn reduces your available credit.

- Pending Transactions: Charges that have been authorized but not yet posted to your account will reduce your available credit temporarily.

- Holds and Pre-authorizations: Certain transactions, like hotel or rental car bookings, can place holds on a portion of your credit line, affecting how much credit is available to you.

- Fees and Interest: Annual fees, late payment fees, or accrued interest can add to your balance. If not accounted for, these can eat into your available credit.

- Reduced Credit Limit: Sometimes, a lender may lower your credit limit due to various factors such as a drop in your credit score or if you have missed payments.

- Fraudulent Activity: Unauthorized use of your credit card can lead to a drop in available credit. Regularly check your transactions to catch any fraud early.

Understanding the reasons behind a low available credit can help you take appropriate actions, such as paying down balances or disputing unauthorized transactions, to manage your credit effectively.

What do available credit and credit limit mean?

Available credit and credit limit are fundamental terms in the world of credit management:

Credit Limit: This is the maximum amount of credit your lender has granted you on a credit product, such as a credit card. It’s the total sum you’re allowed to borrow, and it’s set by your lender based on factors including your creditworthiness and income.

Available Credit: This refers to the remaining amount of credit that you can use at any given time. It fluctuates based on your account activity. To calculate your available credit, you subtract the current balance — which includes all purchases, cash advances, balance transfers, fees, and interest charges — from your credit limit. If you have not used your credit card yet, or you’ve paid off any balance in full, your available credit would be equal to your credit limit.

Understanding these terms can assist you in effectively managing your credit card usage, ensuring you don’t exceed your limit and maintaining a good credit utilization ratio, which benefits your overall financial health.