The Inner Workings of Accrued Interest

Accrued interest is kind of like a snowball rolling downhill – it starts small, but as time goes on, it gets bigger and bigger. When you borrow money or invest, a specific interest rate tells you how fast that snowball grows. It’s a way for lenders or investments to keep earning money, day by day, even if no cash changes hands until much later.

Now, whether you’re dealing with a savings account, a bond, or a loan, the principle remains the same, but the timing can change things. With some loans, that interest might pile up daily, making a slightly bigger snowball each day. In investments like bonds, it can get a bit more complicated with coupon dates and payment schedules.

Understanding how that interest accrues can help you predict what you’ll owe or earn over time, which is super handy for budgeting or planning investments. It’s also essential for properly recording financial transactions in accounting books to reflect what’s actually happening with your money.

KEY TAKEAWAYS

- Accrued interest is a financial concept that affects both borrowers and lenders by representing the amount of interest that accumulates over time on loans, bonds, or interest-bearing accounts, based on several factors such as account type, principal, interest rate, and timing.

- For borrowers, understanding accrued interest is important to estimate charges on upcoming payments, like credit card statements or mortgage payments, and for lenders or investors, it aids in forecasting interest income and ensuring fair pricing when selling financial instruments like bonds.

- In bond trading, accrued interest is crucial for fair transactions, ensuring that buyers compensate sellers for the interest that has accumulated on a bond since the last payment date up to the transfer of ownership, so both parties receive their equitable portion of the next interest payment.

Accrued Interest in Action

Real-World Example of Accrued Interest

Let’s take John and Sarah as examples to understand how accrued interest literally adds up in the real world. They both invested in the same type of bond, worth $10,000 with a 5% annual interest rate, and payments made every six months. Here’s where it gets interesting: John bought his bond on January 1st, while Sarah waited until May 1st.

For John, the math looks like this: $10,000 principal times 5% interest rate times about 0.0849 of a year (for a 31-day month) equals roughly $42.45 of accrued interest by the end of January.

And for Sarah? The calculation is similar: $10,000 principal times 5% interest rate times approximately 0.0822 of a year (for a 30-day month), giving her about $41.10 in accrued interest by the end of May.

So, regardless of when they jumped into the investment, both John and Sarah’s interest started accruing right away, adding a little bit to their potential earnings each day. Their examples highlight how buying dates and periods matter when calculating accrued interest, ensuring they get their fair share of the earnings during the specific time they held the bond.

Whether saving or borrowing, knowing how to figure out accrued interest like John and Sarah can give you a clearer picture of your anticipated earnings or costs over time.

Daily Vs. Monthly Accrual: A Comparative Study

When you’re weighing your options between accounts with daily or monthly accrued interest, think of it as choosing between getting updates on your investment as each page turns or just at the end of each chapter. Daily accrual means your interest snowball gets a little bigger with every sunrise—every. single. day. This is a frequent choice for credit cards, where precision matters because your balance can shift a lot from one day to the next.

But on the flip side, monthly accrual simplifies things. Mortgages and car loans often prefer this method. Interest grows in bigger chunks here, but only once each month, based on your outstanding balance. So, you won’t see the minute-by-minute changes in your interest, but rather a summarized version at the end of each month.

Daily accrual might have you paying slightly more in March than February, purely because of those extra couple of days. Monthly, you’re dealing with a flat rate that’s the same whether it’s a leap year or not—simple and straightforward.

In essence, daily accrual gives a more granular look at interest as it climbs, potentially leading to higher payouts or dues compared to monthly, which offers a steady, predictable rate that you can easily plan for in your financial calendar.

Accounting for Accrued Interest

Journal Entries to Track Accrued Interest

Tracking accrued interest in accounting is like leaving bread crumbs to remind you where your money’s path is headed. If you’re the borrower, every time that interest clock ticks, you’ll mark down an extra slice of owed cheese on your financial trail. Here’s what you’d scribble in your ledger:

- Interest Expense (debit)

- Accrued Interest Payable (credit)

This tells anyone reading your books that you’ve racked up some interest and that it’s pending payment – you haven’t handed over the cash yet, but it’s definitely on your to-do list.

For the lender, the ledger tells a slightly different story. They’re expecting some extra cheese for their bread (so to speak), so they’ll track it like this:

- Accrued Interest Receivable (debit)

- Interest Income (credit)

These entries serve as a promise that there’s money coming in and it’s part of the earnings. Once the borrower hands over the interest payment, both parties will clean up their trail, reversing these entries to reflect the actual cheese that’s moved between them.

Remember that keeping these journal entries accurate is absolutely key to a clear, honest, and transparent set of financial statements. They’re like sending a message to your future self – or anyone looking at your books – that all the financial ducks will be in a row when it’s time to settle up.

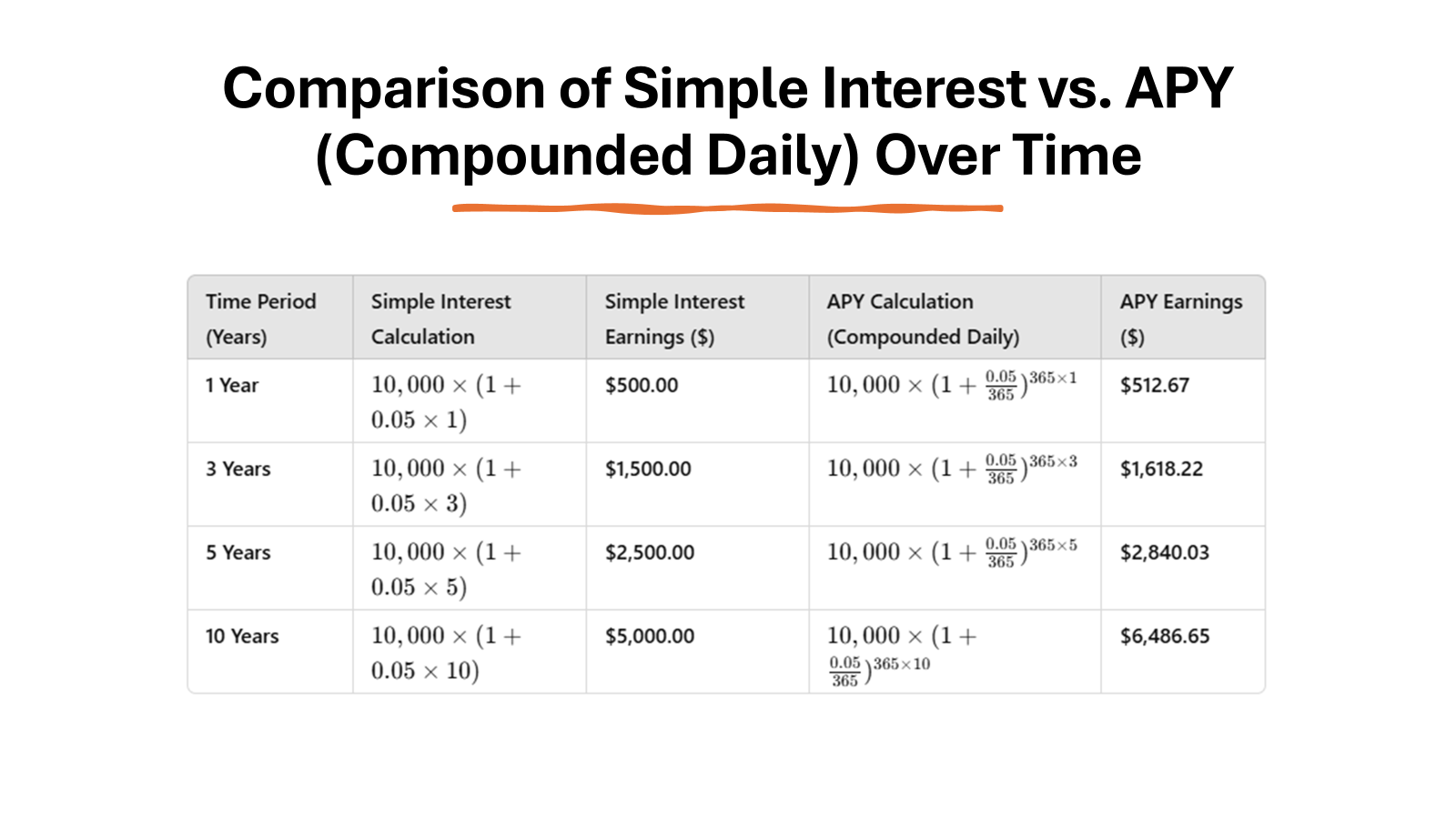

Annual Percentage Yield and Its Impact on Accruals

When it’s time to chat about Annual Percentage Yield (APY), imagine it like a trusty magnifying glass focusing on the true earning power of your investments or the real cost of your loans. APY doesn’t just glance at the basic interest rate; it digs deeper, taking into account how often that interest is compounded – whether it’s daily, monthly, or annually.

Think of APY as the more accurate, beefed-up cousin of the simple interest rate. It reveals the actual scene by factoring in these compoundings, which can make a noticeable difference to your bottom line over time. Essentially, with APY, those interest snowballs we talked about? They don’t just grow; they grow on growth, like a financial Matryoshka doll.

For borrowers, a higher APY means that you’re effectively paying more over the year than the base rate would suggest. For savers and investors, a higher APY is the golden ticket, as it means more money in your pocket. So anytime you’re comparing loans or savings accounts, pull out that magnifying glass and look for the APY – it’ll give you a more precise compass for navigating the jungle of interest rates out there.

To sum it up, when managing and tracking your accrued interest, stay keenly aware of APY. It’ll help ensure that the numbers on your screen or paper match the reality of your financial journey, whether you’re saving for a rainy day or financing your dreams.

Understanding the Differences

Regular Interest Versus Accrued Interest

If you’ve ever felt confused about the difference between regular interest and accrued interest, you’re not alone. Think of them like two chapters in the same book. Regular interest, also known as paid interest, is the amount you pay or collect in a straightforward exchange. You borrow money, and you pay back a little extra—end of story.

Accrued interest, on the other hand, is the buildup of that extra before it’s actually exchanged. It’s like bookmarking the interest you’ll owe or receive on a specific date. This amount can fluctuate based on the balance or terms of your account or loan, gathering silently in the background until it’s either due or paid out.

Here’s a quick comparison to make it crystal clear: With simple interest loans or regular savings accounts, your interest debt or credit stays the same. It’s agreed upon from the start and doesn’t change over time. As for credit cards or investments with accrued interest, the amount can vary because it depends on daily or monthly changes in balances or rates.

So, think of regular interest as a fixed photo on your financial mantelpiece, while accrued interest is more like a slideshow, constantly updating until the moment you freeze it into a payment. By grasping both concepts, you can better manage your loans, savings, and investments to ensure no surprises when it comes to the actual costs or earnings in your financial adventures.

How Investment Accounts Handle Accrued Interest

Investment accounts handle accrued interest with all the precision of a master chef measuring ingredients — every pinch matters. When you invest in something like a bond, the accrued interest accumulates between interest payments, just waiting to be added to the pot. But when you sell that bond before the next interest payment is made, you need to pay the buyer the interest that’s built up since you bought it.

Here’s how it boils down: if you invest in a bond, every day that passes adds a bit more interest into your mix. The financial institution keeps a tally of this, ensuring you’re paid the correct amount of interest on the right date, typically the bond’s coupon date.

Even in savings or investment accounts that earn interest, institutions ensure that accrued interest is allocated correctly. This means the firm will track how much you’ve earned since the last payout and add it to your account balance. You’ll often see this interest reflected in your monthly statements, and it becomes part of your principal for the next cycle of compounding.

It’s a bit like an ongoing game of tag between your money and the interest it’s collecting. By understanding how this process works with your investment accounts, you can more accurately figure out your returns and stay on top of your financial game.

Accrued Interest in Various Financial Scenarios

Accrued Interest in Mortgages and Loans

For mortgages and personal loans, accrued interest plays quite the backstage role, much like a diligent production crew ensures a play runs seamlessly without hogging the limelight. Every day or month, a slice of interest silently adds up on the amount of the loan that’s yet to be settled—your unpaid principal.

When you make a standard payment on your loan or mortgage, it’s like you’re covering two bills at once: one for the interest that’s accrued up until now, and another chip off the old principal block. Lenders have this down to an art form—they use an amortization schedule, which creatively maps out how much of each payment swings towards the interest versus the principal over the loan’s life.

It’s crucial to grasp that at the start, it’s mostly the accrued interest that gobbles up your payments. With every passing month, as the principal balance drops, so does the amount of new interest accruing, gradually making room for more of your payment to diminish the principal. This is known as loan amortization.

By appreciating the role of accrued interest in your loans, you can make more informed choices on things like additional principal payments, which can cut down future interest and fast-track your journey to being debt-free.

Bonds & Savings: Calculating Accrued Interest

Calculating accrued interest for bonds and savings is like following a recipe—the ingredients are the principal, the interest rate, and time. Bonds, whether corporate or municipal, conventionally use a 360-day year for their interest cauldron, while government bonds prefer the actual 365-day calendar. Savings accounts typically follow the lead of the latter, accumulating interest with every calendar day that passes.

For bonds, the method is relatively straightforward: take the interest rate (your recipe’s spices), apply it to the principal (the main ingredient), and adjust for the time period (how long you’re letting it simmer). If you’re selling the bond before the next interest payment, you’ll need to calculate the accrued interest so that the price reflects both the value of the bond and the earned interest.

Savings accounts work similarly, but the beauty here is that the interest continually compounds, folding back into the principal and starting the process anew, potentially increasing your earnings over time exponentially, like a snowball rolling downhill, gathering speed and size.

Understanding these calculations empowers you to gauge the true value of your investments or savings at any point in time, ensuring that you get your just desserts when they are due or knowing exactly what to expect when it’s your turn to pay out.

Practical Guidance on Accrued Interest

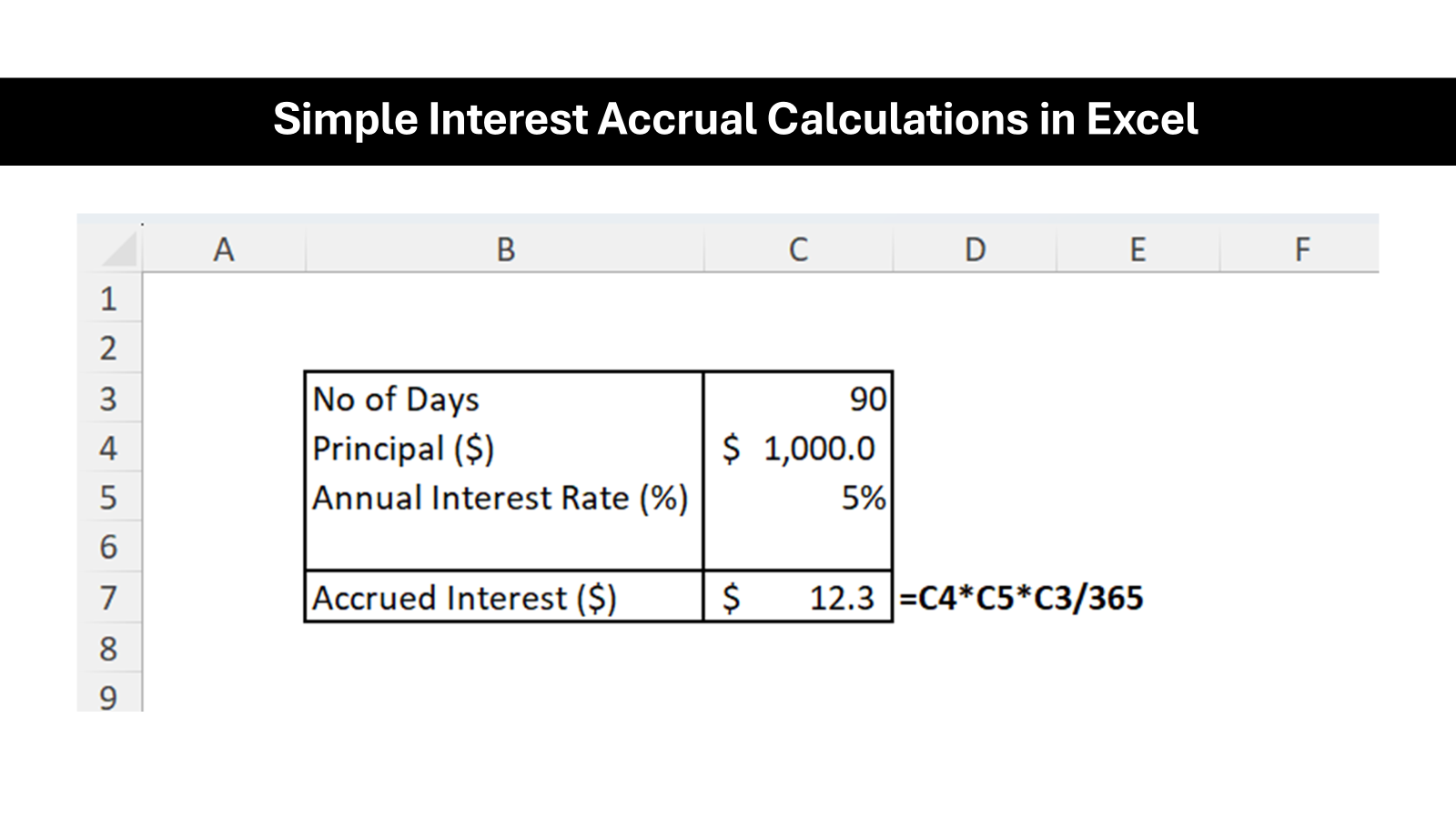

Step-by-Step Guide to Calculate Accrued Interest

Ready to become a whiz at calculating your own accrued interest? Don’t worry; it’s like piecing together a simple puzzle. Here’s how to do it in four easy steps:

- Identify the Principal Amount: This is the starting point—the total sum of money you’ve loaned out or borrowed that hasn’t been repaid yet.

- Pin Down the Interest Rate: Locate the annual interest rate of the bond or loan. It’s often expressed as a percentage.

- Time Period: Figure out the number of days for which you want to calculate the interest.

- Do the Math: Plug these numbers into the accrued interest formula:

- Accrued Interest = Principal × Interest Rate × (Number of Days ÷ Days in a Year)

Here’s an insider tip: Financial institutions might use 360 or 365 for “Days in a Year”—check which one applies.

Let’s break it down with an example. Suppose you have a $1000 bond with a 5% annual interest rate:

- Principal (P): $1000

- Interest Rate (r): 5% or 0.05 (as a decimal)

- Days (t): 30 (let’s say we’re looking at a one-month period)

- Days in a year (y): 365 for this example

Plug them into the formula:

Accrued Interest = $1000 × 0.05 × (30 ÷ 365) Accrued Interest = $4.11 (rounded to two decimal places)

That means $4.11 has accrued in that time.

By following these steps, you can track the interest ticking up on investments or loans, like watching a second hand on a clock. This knowledge is your ticket to mastering the financial details and staying ahead of your fiscal responsibilities or earnings.

Tips for Managing and Tracking Accrued Interest

Staying on top of accrued interest is like tending a garden—you’ve got to keep an eye on it regularly, or it might grow out of control. Here are some tips to manage and track it like a pro:

- Stay Organized: Keep a detailed log or spreadsheet of all your loans and investments, noting the interest rates and accrual periods.

- Set Reminders: Create calendar alerts for payment due dates or times to check in on your accrued interest, so nothing catches you by surprise.

- Use Financial Tools: Embrace digital tools or apps designed to monitor accrued interest and other financial metrics. These can automate the hard work for you.

- Review Statements Carefully: Regularly examine your loan and investment statements to make sure the accrued interest aligns with your own calculations.

- Understand Your Agreements: Know the terms of your investment or loan agreements, including how the interest is compounded and what that means for you financially.

By keeping a close tab on how much interest is accruing, you can budget accordingly, avoid unnecessary debt, and ensure you’re earning what you’re due.

Armed with these tips and a watchful eye, you’ll maintain a lush financial garden, reaping the rewards of your careful attention and diligence.

In-Depth Insights

Related In-Depth Explanations

For those of you who love diving deep into details, there are plenty of in-depth topics related to accrued interest that can satisfy your intellectual curiosity. Here’s a sneak peek into subjects that offer a closer look:

- Compound Interest Theory: This is the engine behind how accrued interest can magnify your savings or debts over time. It’s interest on interest, and it’s powerful.

- Amortization Schedules: Understand how each payment breaks down between principal and interest, and see the long-term journey of a loan.

- Time Value of Money: Grasp the core financial concept that money available now is worth more than the same amount in the future due to its earning potential (and accrued interest plays into this).

- Risk and Interest Rates: Explore how the level of risk influences interest rates and why higher risk can lead to higher accrued interest.

- Tax Implications: Dive into how accrued interest can affect your tax liabilities or deductions, depending on your role as the borrower or lender.

Each of these topics unwraps another layer of the accrued interest onion, providing you with clearer insights and understanding to leverage in your financial strategies.

Equipped with this detailed knowledge, you can make more informed decisions that align with your financial goals, and maybe even uncover some strategies you hadn’t considered before.

Additional Resources for Further Learning

Eager to expand your knowledge horizon on accrued interest and related financial concepts? You’ve got a treasure trove of resources at your fingertips:

Online Courses and Certifications: Enroll in specialized online courses or certifications to get a more structured and comprehensive understanding. Some examples include the Financial Modeling & Valuation Analyst (FMVA)® or the Commercial Banking & Credit Analyst (CBCA)®.

Books and eBooks: Hit the books, literally. There are numerous finance and accounting textbooks that cover everything from the basics to advanced theories.

Webinars and Workshops: Keep an eye out for live sessions from financial experts that often include Q&A segments for real-time learning.

Podcasts: There’s a whole world of finance podcasts that you can listen to on-the-go, offering insights from industry leaders and educators.

Each of these resources can set you on a path to expertise. The most important part is to choose the medium that resonates with your learning style—whether that’s interacting with a live instructor, listening while you jog, or deep-diving into a thick book.

Remember, understanding accrued interest is a marathon, not a sprint—pace your learning, and don’t shy away from revisiting concepts until they stick. Happy learning!

Conclusion

Summarizing Key Takeaways

In wrapping up our exploration of accrued interest, let’s crystallize the key nuggets of wisdom:

- Accrued interest is the amount earned or owed during a specific period but yet to be paid or received.

- Understanding how it’s calculated—principal, interest rate, and time—is crucial for managing loans and investments effectively.

- Daily and monthly accruals differ in frequency, affecting how much interest ultimately accumulates.

- Tracking accrued interest via journal entries is essential for accurate financial statements.

- The Annual Percentage Yield (APY) provides a fuller picture of earned or owed interest, factoring in the compounding effect.

- Differences between regular and accrued interest reflect the timing of payment and affect financial planning.

- Investment accounts keep detailed tracks of accrued interest, which can impact the total value, especially during transactions like bond sales.

- Calculating and managing accrued interest requires diligence, but with practice and the right tools, it becomes second nature.

- A wealth of additional resources, from online courses to webinars, is available for those hungry to learn more.

The knowledge of accrued interest empowers you to make smarter, more informed financial decisions, ensuring that when it comes to your money, you’re both a borrower and an investor who is wise beyond your years.

Remember these takeaways and you’ll be ready to navigate the world of accrued interest with confidence and savvy.

Putting Knowledge into Practice

Taking these insights on accrued interest to heart, it’s time to turn theory into action. Start by pinpointing any loans or investments you have and examine how accrued interest affects them. Use the tips and step-by-step guide we discussed to calculate the current or future accrued interest. This will give you a snapshot of where you stand financially.

Next, reassess your budget and financial planning. Can you make additional payments towards loans to minimize interest expenses? Should you tweak your investment strategies to maximize interest earnings? Now that you’re accruing wisdom as well as interest, make those educated decisions.

For practical application, also check out software or apps that can automate these calculations for you. This can be especially helpful for tracking fluctuating interest accruals on credit card debts or variable rate loans.

Lastly, embrace the habit of continuous learning. The world of finance is forever evolving, much like accrued interest itself. Keeping abreast of changes and deepening your understanding will ensure your financial practices remain as sharp as ever.

By putting this knowledge into practice, you’re not just managing accrued interest, you’re mastering a critical aspect of your financial health, setting you on a course to achieving your financial goals with gusto.

Frequently Asked Questions

What is the meaning of accrued interest and Why Does It Matter?

Accrued interest refers to the amount of interest that has accumulated on a debt or investment over time but hasn’t been paid out yet. It matters because it affects how much you’ll eventually pay on what you borrow or earn on your investments. Understanding accrued interest helps in forecasting financial obligations and returns, aiding in effective budgeting and financial planning.

Accrued interest refers to the interest that has accumulated on a financial instrument but has not yet been paid by the issuer or received by the seller. In bond transactions, the interest accrued between the last payment date and the sale date is often transferred from the buyer to the seller at the time of purchase. The amount of accrued interest is typically calculated using the coupon rate and follows accrual accounting principles, ensuring that interest income or expenses are recorded when earned or incurred, rather than when cash is received or paid. Under the accrual basis of accounting, this allows for a more accurate financial summary, reflecting the true financial position of an entity.

How Do You Perform Accrued Interest Calculations in Accounting?

In accounting, you calculate accrued interest by multiplying the principal amount by the interest rate, then by the fraction of the year that has passed since interest was last paid or received. This tells you how much interest has built up to be accounted for in financial statements, ensuring accuracy in tracking your debts or investments.

What is the journal entry for interest accrued?

The journal entry for interest accrued on a borrowed sum includes debiting the Interest Expense account and crediting the Accrued Interest Payable account. This reflects an increase in expense and a liability for the borrower, indicating that interest cost has been incurred but not yet paid.

How do you record the accrual of interest journal entry?

To record the accrual of interest, debit the Interest Expense account, if you’re the borrower, reflecting the cost of borrowing funds. Credit the Accrued Interest Payable account, which recognizes a liability for this unpaid interest. Reverse the entry when the interest is actually paid.

How does interest incurred relate to accrued interest?

Interest incurred is the cost of borrowing money that has been recognized in your accounts, while accrued interest is the portion of that interest that has been recognized but not yet paid. Incurred interest adds to your expenses, and the accrued portion acknowledges a forthcoming payment obligation or receivable.