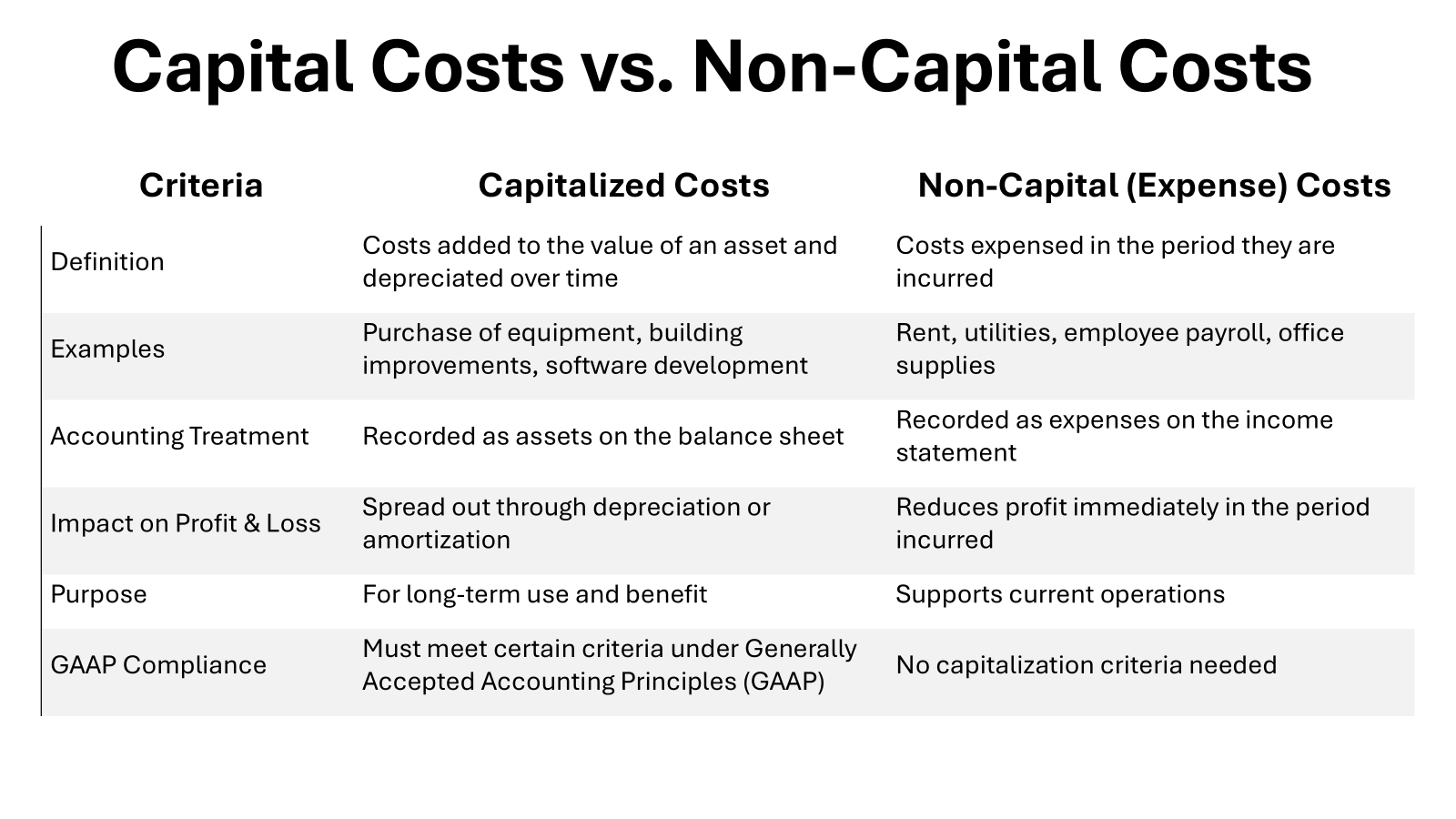

Capitalized vs. Non-Capital Costs at a Glance

Capitalized costs are more than mere numbers on a balance sheet; they’re strategic accounting decisions that shape a company’s financial narrative. When a cost is capitalized, it’s transformed into an asset, helping companies manage the portrayal of their financial health over time. Capitalizing typically spreads the cost over the useful life of the asset, aligning it with the generation of revenue.

In contrast, non-capital costs, or expenses, are recognized immediately on the income statement, reflecting the consumption of economic benefits in the short term. They reduce current profits but can also reduce tax liability, serving as a financial strategy unto itself.

Quick Comparison:

- Capitalized Costs: Treated as assets; Depreciated or amortized over time.

- Non-Capital Costs: Treated as expenses; Deducted immediately in the reporting period.

Remember, while capitalization might bolster a company’s profitability in the short term, it demands a long-tailed consideration of financial ramifications, affecting everything from tax obligations to profit margins over time.

KEY TAKEAWAYS

- Capitalized costs represent expenses that are recorded as assets on the balance sheet due to their future economic benefit. These are depreciated or amortized over the useful life of the asset, spreading the cost over multiple periods. Examples include investments in property, plant and equipment, and development of intangible assets such as patents or software.

- Expenses are recorded on the income statement when they are incurred because they are used up in the generation of revenue for that specific period. These include day-to-day operating costs like rent, utilities, and employee salaries. Expenses impact the net income immediately as they are not expected to provide economic benefit in the future periods.

- The decision to capitalize or expense a cost is governed by a company’s accounting policies and involves the use of professional judgment. This decision is crucial as it affects a company’s financial statements and ratios, thereby impacting the company’s perceived financial health and ability to obtain financing or make informed strategic decisions. Inconsistent or inappropriate capitalization decisions can lead to a misrepresentation of a company’s performance and financial position.

Core Principles of Cost Capitalization

Understanding When to Capitalize Costs

Capitalizing costs is not just a choice, but a strategic move regulated by the Generally Accepted Accounting Principles (GAAP). The decision to capitalize a cost pivots on whether the expense will benefit the company over several periods, rather than just the current one. If you’re peeking into the books of a company and notice a substantial investment not listed among its expenses, they’ve likely capitalized it, aligning the cost with future benefits.

To be capitalized, a cost must meet certain criteria:

- It provides a future economic benefit to the company.

- It extends the useful life of an existing asset.

- It increases the value or productivity of an asset.

Major investments that qualify include the purchase of property, plant, equipment (PPE), and substantial improvements beyond routine maintenance. So, next time you’re making a hefty purchase or improvement for your company, ask yourself, “Will this benefit us over several years?” If yes, you’re looking at a potential candidate for capitalization.

The Impact of Capitalization on Financial Statements

When costs are capitalized, they’re not just tucked into the asset column; they lead a double life affecting both the balance sheet and income statement. Initially, your assets swell, as you’re adding value without immediately taking a hit on the bottom line. The balance sheet grows sturdier—at least at first glance.

On the income statement, the plot thickens. Capitalized costs dodge the immediate blow to your profitability, opting instead for a cameo appearance as depreciation or amortization over time. This act preserves your early profit margins but promises a drawn-out expense narrative in future periods.

What’s unique about capitalized costs is their ability to shift the timing of expenses. They’re the ‘deferred dreams’ of the accounting world—spreading costs across the lifespans of assets rather than letting them flood the current period’s earnings. It’s a long game, playing with how profitability unfolds over time.

Remember, capitalizing affects cash flow statements differently, too. These costs surface in investing activities, which differ from those danced around in operating activities. This distinction is pivotal not just for accountants but also for analysts discerning the operational cash health versus long-term investments.

Navigating Through Capital and Expense Examples

What Does It Mean to Capitalize Expenses?

Capitalizing expenses means taking a cost that could have been considered as an immediate expense and instead recognizing it as an asset on the balance sheet. In essence, you’re saying, “Let’s not rush; this investment is for our future growth, and its benefits will unfold over time.” You’re giving expenses a new identity as capital assets, which will gracefully age on your balance sheet through depreciation or amortization.

Here’s what happens when you capitalize an expense:

- The cost is recorded as an asset, rather than an immediate hit to your profit and loss statement.

- It shifts part of the expense to the future, spreading it out over the asset’s useful life.

- Depreciation (for tangible assets) or amortization (for intangible assets) becomes the new norm for recognizing the cost over time, slowly chipping away at it on the income statement.

By capitalizing an expense, you’re essentially deferring the recognition of costs, which can enhance your company’s current profitability and smooth out earnings over time. This approach aligns expenses with the revenue they help to generate, adhering to the matching principle in accounting.

Expert Examples of Capitalized Costs

Capitalized costs have a presence across nearly every industry and come in various forms. However, they all share the common thread of being pivotal for long-term growth. Here’s a rundown of some expert examples where businesses typically capitalize costs:

- Materials used to construct an asset: If you’re building a new facility, all the bricks, mortar, and steel go onto your balance sheet, not your monthly expenses.

- Interest on construction loans: Interest that accrues while you’re building a sizable asset—think a new corporate headquarters—can be capitalized, easing your current interest expense burden.

- Wages and benefits associated with construction: The paycheck for every worker who laid a brick or wired a switch in a new building capital project adds value and sits as an asset, not an expense.

- Purchased assets and sales taxes related to them: Everything from the heavy machinery down to the sales tax on that machinery can be viewed through the capitalization lens.

- Transport and testing costs for new assets: Getting a heavy piece of equipment to your site and making sure it’s working smoothly? Those costs too can be embossed onto the balance sheet.

- Costs spent improving an existing asset: When you upgrade machinery or renovate a property such that it boosts the asset’s value or useful life, these improvements fall under capitalized costs.

- Qualifying software development costs: Developing in-house software isn’t just a line item on your expense report; it’s an investment into an intangible asset that you’ll capitalize and then amortize.

Businesses gauge these types of costs, forecast their utility, and then decide that instead of expensing them right away, they’ll recognize them as assets, setting the stage for future earning potentials. Capitalizing these costs reflect a company’s investment posture and strategic allocation of its resources.

Non-Capital Costs and Current Expensing: What Falls Under This Category?

Non-capital costs are the day-to-day expenditures that companies incur during their normal course of business. These costs don’t result in ownership of an asset and don’t offer future economic benefits that are capitalizable, hence they are expensed in the period when they occur. Understanding what falls under this category prevents overstating assets and provides a clear, immediate reflection of expenditures on financial performance.

Here are some examples of non-capital costs:

- Office Supplies: The pens, paper, and printer ink that keep the office running smoothly are not assets, but necessary expenses for everyday functionality.

- Utility Bills: Monthly payments for electricity, water, and internet services are costs that keep the business environment operational.

- Routine Maintenance and Repairs: Keeping your existing assets functioning, like fixing a leaky faucet or a laptop tune-up, counts as an expense.

- Advertising and Marketing Costs: These efforts, though essential for growth, are expensed because they generally don’t create a long-term asset.

- Rent: The cost of leasing a space for operations is considered an expense as it doesn’t result in ownership, although it’s crucial for operations.

These operational expenses can’t don the cape of capital costs; they fly as expenses, directly matching revenue with the costs incurred to earn it in the same period. This method ensures businesses reflect a healthy, transparent interplay between income and outgoings.

The Accounting Treatment: Capitalize vs. Expense

Dive Into Capitalized Software Development Costs

When it comes to software development, the capitalization journey begins when you’ve moved past the preliminary stage and are actively engaged in creating a product that will offer future economic benefits. Capitalized software development costs break down to two main spheres: internal-use software and software intended for sale.

For internal-use software, think about an accounting system tailor-made for your business. Here’s what you can capitalize:

- Costs of coding and testing during the development phase.

- Salary and wages of developers directly involved in the project.

- Third-party development fees, if you’ve outsourced some of the work.

If the software is intended for sale, the rules change slightly. Capitalization starts when the product is technically feasible and ends when the product is available for general release. During this phase, you can capitalize:

- Programming costs.

- Direct labor costs associated with software construction.

- Overhead costs that are directly tied to software development.

Capitalizing these development costs means stretching the investment over the software’s useful life, smoothing out expenses, and matching them against the revenues generated.

Why Certain Costs Are Capitalized and Others Are Expensed

The decision to capitalize or expense comes down to the benefit that the cost will provide and the duration of that benefit. Costs are capitalized when they are expected to help generate revenue over several accounting periods. This is in harmony with the matching principle in accounting, which seeks to match expenses with the revenues they help to produce.

Here’s why certain costs are capitalized:

- To better match costs with the resulting revenue

- To provide a more accurate financial picture over time

- To comply with accounting standards and principles

On the other hand, a cost is expensed if its benefit is short-lived and consumed within a single accounting period because it:

- Reflects the immediate consumption of the benefit

- Ensures expenses are recorded in the period they are incurred

- Avoids overstating assets and understating expenses

Deciding to capitalize or expense is more than just following the rules — it reflects a company’s strategic financial stance. Excessive capitalization could mislead about a company’s profitability in the short term, while expensing significant investments could unnecessarily diminish reported earnings.

Detailed Explanations: Capitalize or Expense?

Deciphering Internal Labor Costs and Their Treatment

Internal labor costs in the context of capitalizable activities are a nuanced affair. It’s not about the paychecks for the day-to-day jobs, but about the wages poured into constructing an asset or enhancing its value. If you’ve got a team diligently working on the development of a new product or building an addition to your facility, their labor isn’t just an operational cost; it’s an investment contributing to the creation of a valuable, long-term asset.

These labor costs can be capitalized when:

- Directly associated with a capital project like constructing or developing an asset.

- Able to be specifically identified and measured as part of the cost of the asset.

- Incurred during the application development stage for software or during the construction period for tangible assets.

For example, if you’re developing a breakthrough software, the time spent by your developers is capitalized as part of the software’s cost on your balance sheet. This leads to a deferred recognition of the expense through amortization, matching the cost with the revenue the software will generate over its useful life.

By capitalizing these costs, companies can better represent the relationship between investment and returns, as well as manage their reported earnings. Just remember, the key is precise measurement and a clear connection to the asset being created or improved.

Furniture, Fixtures, and Equipment – To Capitalize or Not to Capitalize?

Furniture, fixtures, and equipment — often referred to collectively as FF&E — embrace a large portion of a company’s tangible assets. When pondering whether to capitalize these items or not, businesses take a stroll through several considerations:

- Cost: Is the purchase price significant enough to warrant capitalization?

- Useful Life: Does the item have a life expectancy beyond the current year?

- Benefit: Will it contribute to generating revenue over several periods?

The standard playground rules are clear: if the FF&E cost is substantial and will provide enduring utility, then it’s typically appropriate to capitalize it. Once nestled in your assets column, these items gradually share their cost with the income statement via depreciation, reflecting their consumption over time.

But not all seats at the table get the same treatment. Smaller, less significant items, or those that wear out within a year, often get the expense ticket straight to the income statement. They may not command the limelight as assets, but they keep operations running day-to-day.

Capitalization of FF&E can significantly impact financial reporting and tax planning, adding layers to asset management strategies. So, when you equip your business next time, mind not just the price tag, but also the long-term role each piece plays.

Case Studies: Real-Life Capitalization Scenarios

Capitalization Example with Fixed Assets

Let’s roll out a classic example involving fixed assets — say, a company splurges $2 million on a building, plotting a grand strategy over its expected 40-year lifespan. Capitalization swoops in, turning this expenditure into a fixed asset on the balance sheet versus an intolerable expense on the income statement.

Here’s the breakdown:

- Initial Cost: $2 million purchase price is recorded as the building’s value.

- Depreciation: $50,000 a year ($2 million ÷ 40 years) is methodically recognized as an expense.

- Cash Flow: The actual cash shelled out appears on the cash flow statement under investing activities during the purchase year.

The outcome? The balance sheet flexes its stability with a new asset while the income statement remains unscathed by the full cost upfront. Instead, the expense takes a leisurely, predictable stroll across four decades, mirroring the building’s gradual aging. By the end of the useful life, if the salvage value is nil, the $2 million carrying value of the building will have gracefully bowed out, leaving no balance.

This approach ties back to the principle of matching expenses with revenue generation, providing a clear-eyed view of how the asset helps the business give back over time.

These strategic maneuvers around fixed assets showcase capitalization as an essential element in financial storytelling — rational, yet with long-term foresight.

Expense Example with Inventory Purchase

An inventory purchase illustrates the sprinting counterpart to capitalization’s marathon. When a company stocks up on inventory, it’s gearing up for near-term sales rather than long-term asset accumulation. Inventory is classified under current assets, as it is expected to be sold within the business cycle — typically within one year. The costs are cycled out swiftly, unlike the steady trek of a depreciating asset.

Here’s the quick dive into inventory expensing:

- Initial Cost: The company records the inventory purchase as a current asset.

- Cost of Goods Sold (COGS): Once the inventory is sold, the cost transitions to an expense, reflecting on the income statement.

- Correlation to Sales: The expense recognized aligns neatly with the revenue from the sale, following the close-knit dance of the matching principle.

In the bustling ballet of business operations, inventory expenses take center stage, capturing the immediate nature of these costs. The recognition of inventory expenses in tandem with the sales they drive maintains a clear, timely picture of profitability.

By taking the expense route with inventory, companies underscore the nimble nature of operations—where the flux of buying and selling shapes the financial health of every quarter.

Recognizing the Long-term Effects of Capitalization Decisions

How Does the Capitalize or Expense Decision Impact Returns?

Your choice to capitalize or expense a cost brings with it ripples that sway the company’s reported earnings and, subsequently, returns. Capitalizing delays the expense recognition over the asset’s useful life, buoying net income in the early years post-investment. This can mean an attractive, beefed-up bottom line and return on equity thanks to a lower immediate expense burden.

Conversely, the expensing decision pops the expense balloon right away, fully impacting earnings in that period. This could signal leaner profit margins initially, but it dispenses with the drag of future amortization or depreciation, setting the stage for clearer skies ahead in terms of earnings.

In terms of return on assets, capitalized costs might lead to seemingly lower returns earlier on due to the increased asset base. Yet, as time trots on, provided the assets generate adequate revenue, the returns can balance out or even improve.

These decisions don’t just echo in the halls of accounting; they spill over into tax implications since they determine taxable income. Capitalizing lowers taxable income initially, while expensing could mean a greater tax deduction in the current period.

It’s essential to keep both eyes open on how these decisions mold the curves of your financial trajectory — from sparkling income statements to the steady heartbeat of the balance sheet, and into the taxman’s ledger.

Treading the line between capitalizing and expensing is therefore not just a matter of regulatory compliance, but one of strategic financial management, influencing investor perception and the future financial elasticity of the enterprise.

Benefits and Limitations of Cost Capitalizing

Delving into cost capitalizing opens the door to a mixture of tactical advantages and potential drawbacks. The upside of this approach touches upon several facets of financial reporting and strategic planning.

Benefits of Cost Capitalizing:

- Improved Short-Term Profitability: By avoiding immediate expense recognition, net income takes a less immediate hit.

- Tax Deferral: Capitalization could lead to tax savings in the early years since depreciation expenses are lower than the upfront cost would have been.

- Cash Flow Management: Since the expense is spread out, it can help manage cash flows more effectively.

- Asset Valuation: The balance sheet reflects a more comprehensive view of the company’s assets that contribute to revenue generation.

- Compliance with GAAP: Proper capitalization aligns with accounting standards, providing an accurate financial representation.

Limitations of Cost Capitalizing:

- Complexity in Accounting: The process of capitalizing costs requires detailed tracking and can be resource-intensive.

- Long-Term Profitability Impact: While short-term profitability improves, there might be reductions in reported earnings over time due to ongoing depreciation or amortization expenses.

- Potential for Misleading Financial Health: Overzealous capitalization practices may present a stronger financial position than what is accurate, potentially misleading stakeholders.

- Undercapitalization Risk: Companies with less cash on hand might face financial instability, as significant cash outflows for capitalized costs are not immediately evident on the income statement.

Each enterprise must weigh these factors carefully, tailoring its capitalization policies to fit its financial landscape while ensuring transparency and regulatory compliance.

In the end, like most choices in finance, capitalizing costs is about balance—leveraging the benefits while navigating the limitations to illuminate the most accurate picture of a company’s financial performance and position.

Practical Takeaways for Business and Finance Professionals

Key Learning Points From Capitalization Practices

Capitalization practices offer a treasury of insights for business and finance professionals aiming to master the art of financial clarity and foresight. Here are some key learning points to pocket:

- Future-Forward Accounting: Capitalization underscores the principle of looking beyond the immediate period to strategize how investments unfold financially over time.

- Discerning Value: Learning when and what to capitalize teaches the importance of discerning the enduring value of expenses versus their transient nature.

- Regulatory Adherence: Familiarity with capitalization rules sharpens compliance with GAAP, ensuring that a company’s financial reporting adheres to recognized standards.

- Strategic Financial Management: Understanding capitalization offers a viewpoint in how to manage the company’s earnings, taxes, and cash flows strategically.

- Integrity of Financial Statements: Implementing capitalization appropriately ensures the integrity of financial statements, reflecting the company’s true financial health.

Bulletproof your accounting strategies by appreciating the nuances of capitalization. Let these insights be your compass in navigating the complex web of financial reporting, taxation, and long-term financial planning.

Soak in these insights, and you’ll find that capitalization isn’t just about the balance sheet or the income statement, but it’s also a testament to how thoughtfully a company chooses to present its financial journey over time.

Enduring Impacts on Depreciation and Market Capitalization

The ripples of capitalization practices extend to affect both the depreciation schedule of a company’s assets and its market capitalization over time. When you capitalize a cost, you’re signing up for a long-term relationship with it through depreciation, which methodically allots the cost of an asset over its useful life. This commitment impacts profit margins and cash flow forecasts for years, making savvy depreciation methods crucial.

Depreciation, while a non-cash charge, diminishes reported earnings, affecting key performance ratios and potentially influencing stock prices and investor decisions. Companies must judiciously appraise their assets’ life expectancies, steer through different depreciation methods, and make any necessary impairment adjustments to ensure financial statements stay true to the story.

On the broader horizon, capitalization influences market capitalization—a company’s valuation in the public eye—by shaping perceptions of financial health and growth potential. Effective capitalization policies can underpin solid earnings reports and robust balance sheets, enhancing investor confidence and driving up market valuation.

In a nutshell, capitalization’s enduring impacts span the granular level of ledger entries to the broad strokes of market presence and worth.

By grasping the nuances of depreciation and being cognizant of its cascade onto market capitalization, finance professionals can align capitalization policies with business strategies that steady the ship across both tranquil and turbulent financial waters.

Conclusion

Summarizing the Concept of Capitalization in Business

To unwrap the concept of capitalization in business is to understand its dual role as both a financial strategy and an accounting methodology. It’s a principle that determines how companies spread the cost of tangible and intangible assets over their useful lives, rather than expensing them immediately. This shapes a company’s financial narrative, smoothing out earnings and reflecting an investment mindset that’s playing the long game.

You’ve learned that capitalization is about more than just keeping the books; it affects everything from tax strategies to how a business is perceived in the market. It demonstrates a company’s commitment to sustainable growth, ensuring that costs are recognized in sync with the benefits they generate.

To sum up, Capitalized costs are expenditures that are recorded as assets on a company’s balance sheet and depreciated over time. These costs can include lease payments, patent and copyright fees, and other asset expenditures that meet certain specifications. The threshold for what constitutes a capitalized cost can vary depending on the type of asset and the accounting rules in place. For example, in the United States, the IRS has specific guidelines for what can be capitalized and what must be expensed immediately. In the marketplace, companies must carefully consider which expenditures to capitalize in order to accurately reflect their financial position and avoid misrepresenting their income statement. This is particularly important for depreciation expense accounts, as incorrectly capitalized costs can lead to inaccurate depreciation expense on the income statement. Additionally, government data and trade-in values can also impact the calculation of capitalized costs. By understanding the different types of expenditures and how they are treated under accounting rules, businesses can ensure that they are accurately reporting their financials and making informed decisions about their investments.

Remember, capitalization is not a mere accounting choice; it’s a crucial cog in the machinery of financial wisdom. It flexes with the company’s strategic moves, marks its growth trajectory, and helps stitch together the fabric of fiscal prudence and transparency that envelops successful businesses.

FAQ Section

What is the capitalize meaning in financial terms?

In financial terms, to capitalize means to record a cost as an asset on the balance sheet, rather than as an expense on the income statement. This process spreads out the recognition of the cost over the asset’s useful life through depreciation or amortization, offering a strategic method to match expenses with the revenues they help to generate. Capitalization ensures that the cost is recognized in tandem with the asset’s contribution to business operations over time.

Can You Provide Examples of Capitalized Costs Within a Company?

Certainly! Capitalized costs within a company can include the purchase price of property and equipment, the construction costs of a new facility, major renovations to existing assets, and the software development costs for in-house use. All these represent substantial investments that will provide long-term benefits to the company. By capitalizing these, the company turns the costs into assets on the balance sheet, and they will be depreciated or amortized across their useful lives, influencing the company’s financial statements gradually rather than immediately.

How Is Capitalization Treated Differently in Accounting vs. Finance?

In accounting, capitalization involves the recording of a cost as an asset on the balance sheet, with the cost being allocated over the asset’s lifespan through depreciation or amortization. It’s a technique that aligns with the matching principle of recognizing expenses in the same period as the related revenues.

In finance, capitalization is often viewed through a broader lens, relating to the overall capital structure of a company. This includes the mix of a company’s equity, debt, and retained earnings used to fund its operations and investments. Financial capitalization affects a company’s strategic decisions, risk profile, and how investments and operations are financed.

What Costs Should Always Be Capitalized According to GAAP?

Under GAAP, costs that should always be capitalized are those that result in the acquisition or improvement of long-term assets with a useful life extending beyond the current year. These include the purchase price of property, plant, and equipment, along with the associated transportation and installation costs, and significant overhauls or renovations that extend the asset’s life or improve its capacity. Software development costs for internal use or for sale, once past the preliminary stage and when future economic benefits are expected, should also be capitalized.

What is a capitalizable cost in accounting?

A capitalizable cost in accounting is an expenditure that is recorded as an asset on a company’s balance sheet rather than being expensed immediately. This includes costs that add value to a business in the form of acquiring or upgrading a long-term asset, such as equipment, buildings, or intangible assets. Capitalizable costs provide future economic benefits and are depreciated or amortized over the useful life of the asset, reflecting their consumption over time in a manner that corresponds with revenue generation.