Understanding the Basic Concepts

Grasping the basic concepts of the matching principle helps you see the financial picture with more clarity. In essence, it’s about aligning expenses with the revenues they help to generate. So if a company incurs costs to sell a product or provide a service, those costs should be recorded in the same period the revenues are earned. It’s not about when the cash changes hands—it’s about the economic events and their timing.

For example, when a software company incurs costs for developing a program that it plans to sell over several years, the matching principle guides them to recognize those costs as expenses over the same period the software generates revenue, not all at once.

KEY TAKEAWAYS

- Accurate Financial Representation: The matching principle ensures that revenues and expenses are reported in the same period they occur, providing a more precise depiction of a company’s profitability and financial performance over time. This results in financial statements that better reflect the true economic activities and results of an organization.

- Informed Decision-Making: By aligning expenses with the revenues they help generate, the matching principle aids businesses and investors in making more informed decisions regarding operations, resource allocation, and investments. This alignment helps in assessing the real impact of financial events and strategizing for future growth or adjustments.

- Transparency and Comparability: Adherence to the matching principle promotes transparency and accuracy in financial reporting, bolstering the confidence of investors, creditors, and other stakeholders. This, in turn, ensures that financial information is consistent across periods, enhancing comparability and helping maintain trust and integrity in financial reporting.

Delving into the Details

The Role of the Matching Principle in Financial Reporting

The matching principle plays a pivotal role in financial reporting, serving as the financial world’s balancing act. It ensures that each period’s financial statements are telling the true story of a company’s economic events. With expenses matched to generated revenues, they provide a coherent and fair view of profitability for that period. This principle stops financial statements from being misleading, with either inflated profits or understated expenses, guiding stakeholders towards more informed decisions.

Examples that Illustrate the Matching Principle at Work

Dive into these real-life scenarios to see the matching principle in motion! Take a publishing company that pays for a manuscript in one month but doesn’t publish and sell the book until months later. By aligning the cost of acquiring the manuscript with the revenue from book sales, they practice the matching principle. Or consider a tech firm that buys ads in December; the benefits spill into January, so they recognize the cost in January’s reports alongside the revenue those ads generate. It’s all about linking expenses directly to their revenue counterparts.

The Role of Matching Accounting Principles in Financial Reporting

Embracing the matching principle fundamentally shapes the integrity and reliability of financial reporting. It commits to ensuring that the financial results of a period rightly mirror the economic activities that occurred. Investors and analysts rely on this principle to assess the true profitability and performance trends of a business, free from distortions due to timing issues. Without it, there’d be chaos, with income and costs misplaced, and the whole financial narrative could read like fiction rather than fact.

How the Matching Principle Matches Expenses and Revenues

You’re on a journey to understand how the matching principle expertly pairs expenses with revenues, and it’s a bit like a dance. When a company earns revenue from selling a product or service, any expenses that contributed to that sale should take the stage in the same period. It’s not just about when the money comes in or goes out. Say a business throws a big launch event for a new product—it’s crucial to account for the event’s cost in the same timeframe the product starts raking in sales, keeping the profit and loss performance in tune with reality.

Implementation Challenges

Navigating Difficulties with Revenue Recognition

Charting the waters of revenue recognition can be tricky, especially when revenue streams ebb and flow over time. Think about when a project spans several years; recognizing revenue appropriately then becomes a complex task. Adjustments to contracts, evolving project scopes, and various degrees of customer involvement add layers of difficulty. CFOs like to steer clear of ‘revenue leak‘—essentially, gaps between the profits on the books and the cash actually making its way to the bank.

To ensure you’re recognizing revenue correctly, you might dive into our on-demand webinar, “Stop the Cash Leakage! Extend Your Liquidity Runway by Optimizing the Invoice to Cash Process.” It’s got insights on sealing up those leaks.

Accounting for Long-Tail Costs and Depreciation

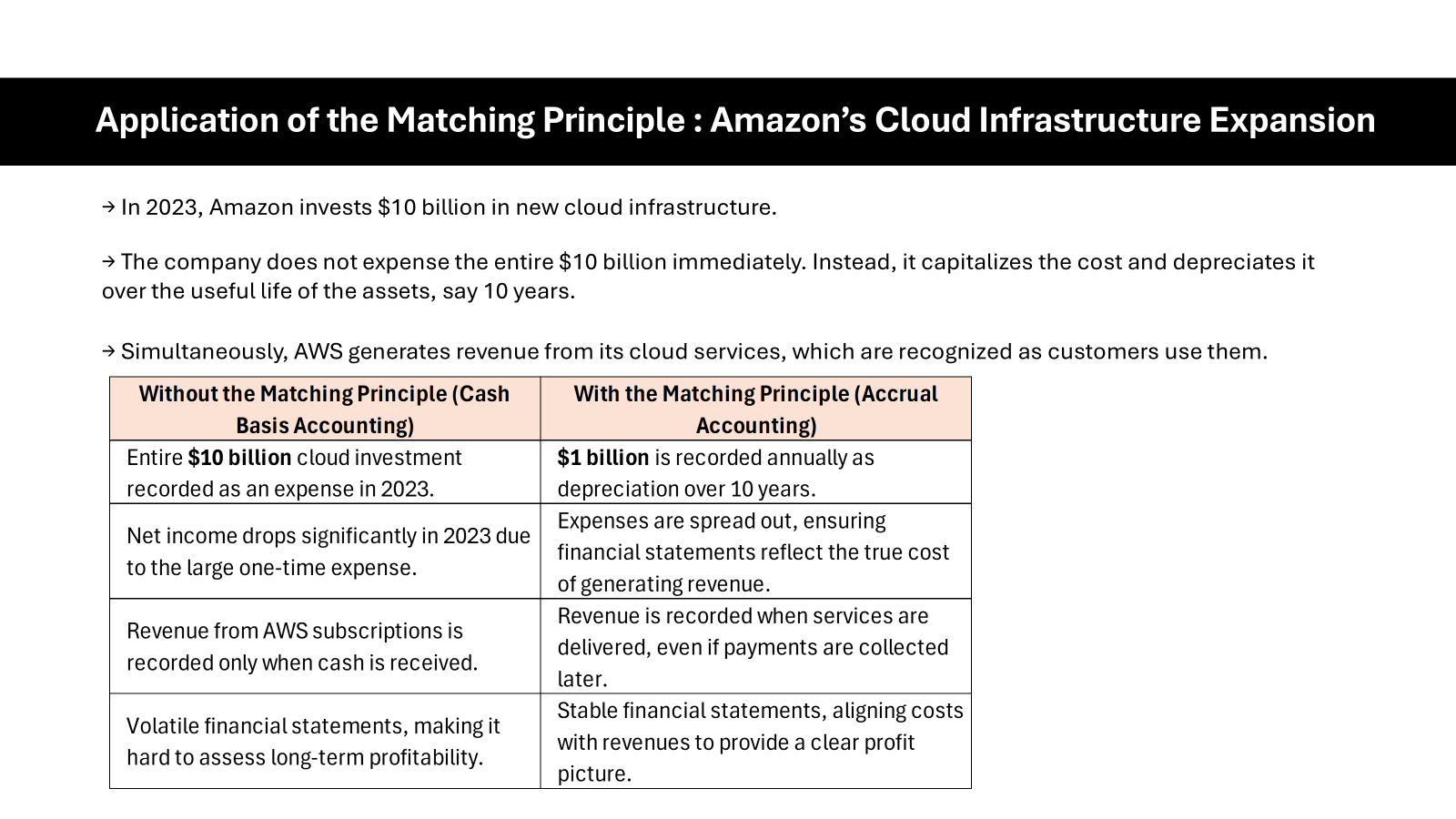

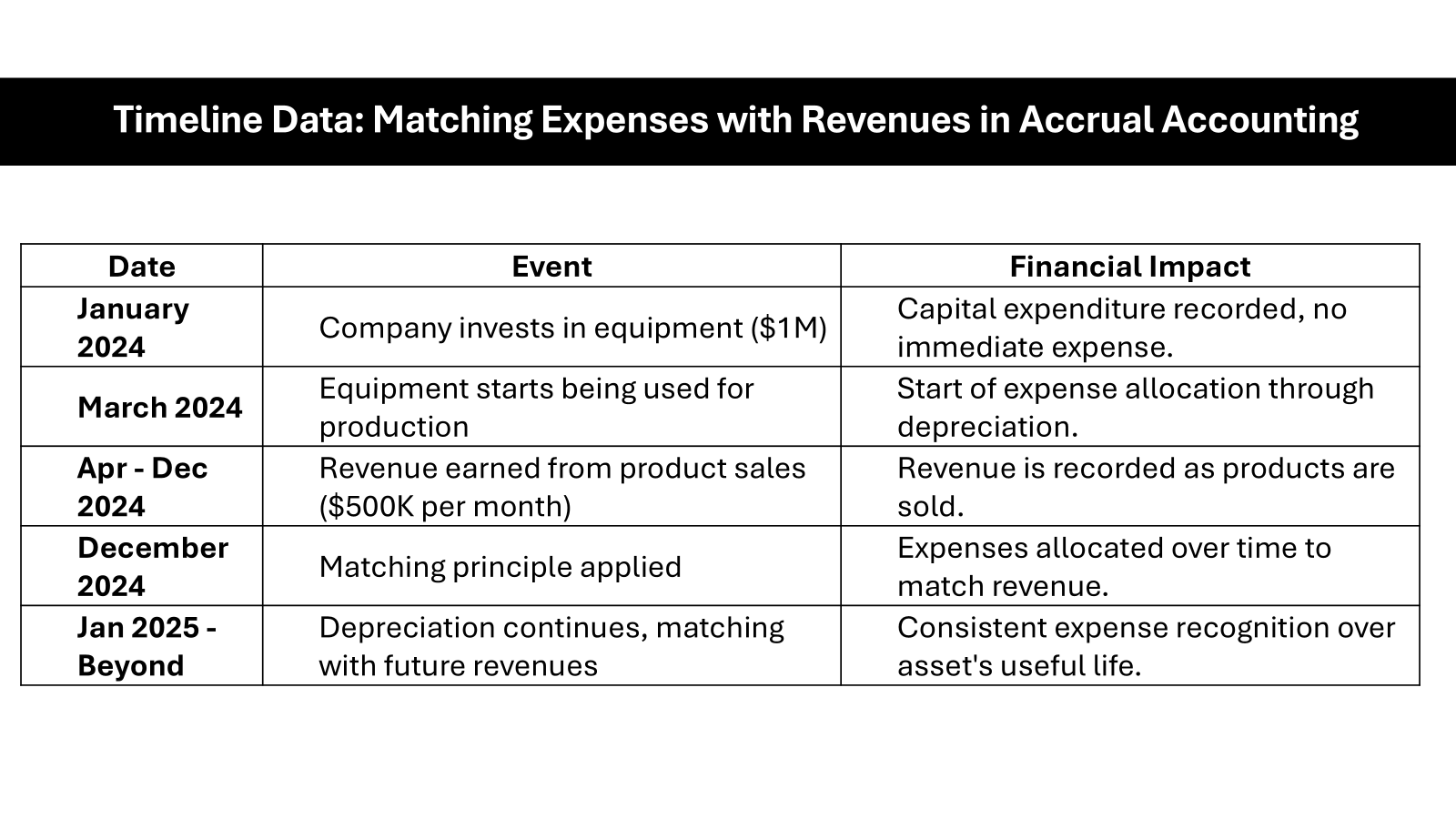

When you start to deal with long-tail costs and depreciation, things get a tad more complicated, but fear not! Long-term assets like machinery or office buildings don’t just wear out overnight. By stretching their costs across their useful life, you match the expense of long-term assets with the income they help produce. It’s like slicing a cake for guests arriving at different times; each slice represents the asset’s expense for that period.

Consider this: a company splashes out $100,000 on a new machine expected to last 10 years. Instead of swallowing the cost in one gulp, they savor it, recording a $10,000 depreciation expense annually. This way, the cost is proportionally savored over each year the machine helps churn out products, aligning costs with benefits received.

Real-World Application

Common Scenarios Where the Matching Principle Comes Into Play

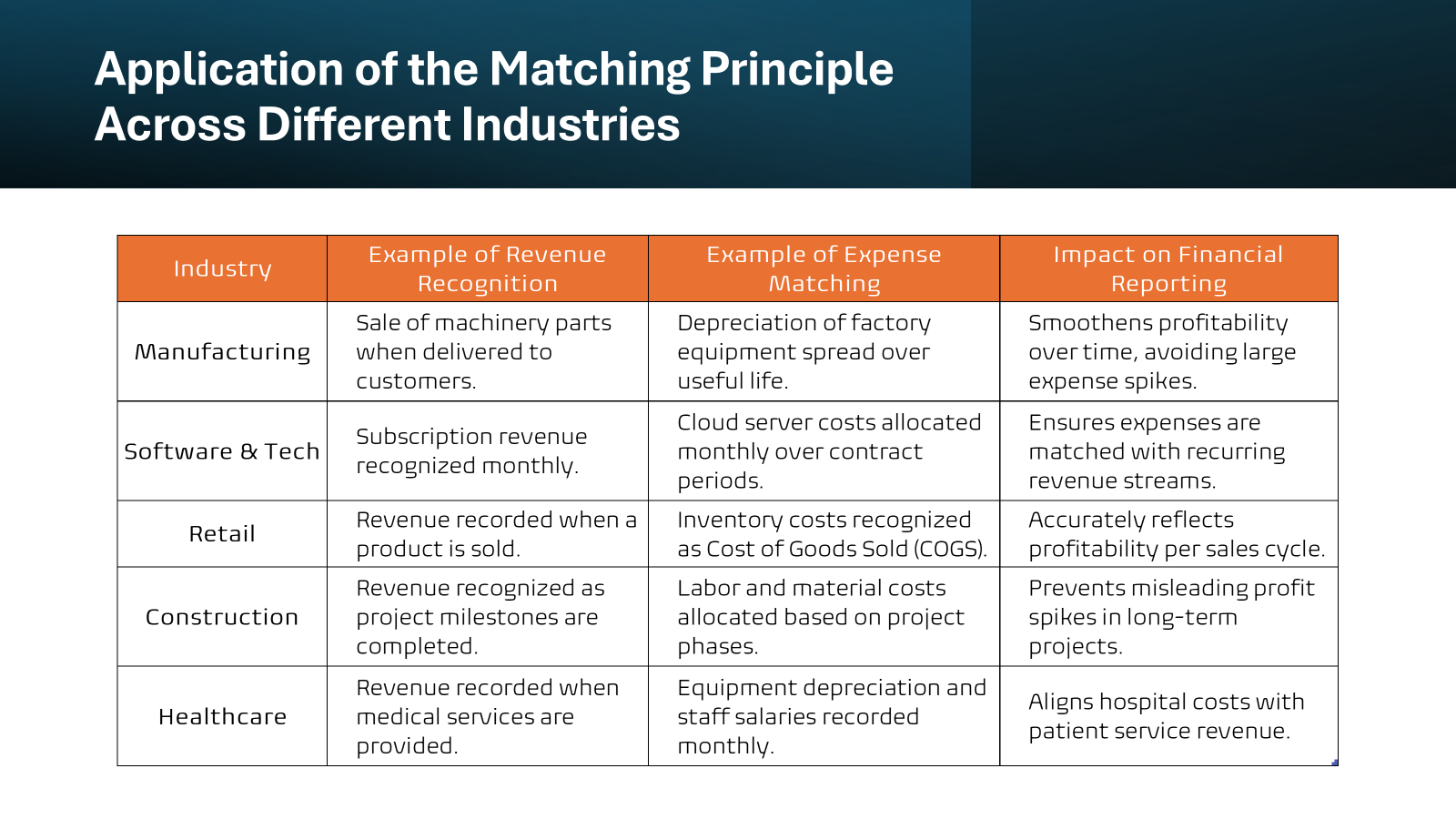

Let’s peek at some everyday business situations where the matching principle really comes into its own. Imagine a retailer selling holiday items; they’ll rack up costs for seasonal inventory and marketing well before December. By matching these costs with the holiday sales revenue, they maintain an accurate financial portrait. Or take your favorite magazine subscription; the publisher distributes the cost of producing the entire issue over its shelf life, matching it with the sales revenue across the same span.

In construction, companies face expenses like materials and labor long before they invoice their clients. They apply the matching principle by recognizing these costs in the same period they recognize the revenue from that project.

And don’t forget the tech world, where giants regularly invest in research and development. These investments are methodically matched against revenues from the resulting products or services, showing a transparent picture of profitability.

How Automating Accounts Receivable Can Comply with the Matching Principle

Automation in accounts receivable can be a game-changer when it comes to adhering to the matching principle. Think of it as having a financial sous-chef that preps everything perfectly for you. Automation tools help you capture expenses and link them to corresponding revenue with precision timing. This alignment is critical for companies with complex revenue cycles or numerous clients on different payment terms.

For instance, AR automation tools can recognize revenue from a subscription as it’s earned each month, while spreading out the costs of the support team over the same period. It’s a tidy way of ensuring your books reflect the true health of your business without sweating over spreadsheets.

The Advantages and Limitations

The Benefits of Using the Matching Principle in Accounting

The benefits of employing the matching principle in accounting are a win-win for accuracy and insight. By mirroring expenses with the revenue they help to generate, you get a truer sense of a company’s profitability and sheer financial performance. This crucial alignment aids in crafting informed business decisions. And it’s not just the decision-makers who benefit; transparency and precision in financial reporting are invaluable to investors and stakeholders, reinforcing trust in the company’s figures.

- Top 5 Features:

- Benefits:

- Cons:

- Best For: The matching principle is best for businesses that value accuracy and transparency in their financial statements, particularly those with operations and transactions that span multiple accounting periods.

Potential Pitfalls and Disadvantages

The matching principle isn’t without its snags and drawbacks. For smaller businesses or those without in-house accounting expertise, applying this principle can seem like traversing a maze blindfolded—it gets complicated. It demands more effort to track accruals and shift expenses across periods, which can deter some from using this approach. Plus, not all expenses have a clear cause-and-effect relationship with revenue, leaving businesses scratching their heads over how to distribute costs.

Sometimes, like with marketing costs or the depreciation of an office building, it’s tough to pinpoint exactly how they drive revenue over time. Applying the matching principle in such cases requires assumptions and estimations, which can open the door to inaccuracies and subjective judgment calls.

- Top 5 Features:

- Benefits:

- Cons:

- Best For: The matching principle is best for organizations with the accounting resources to tackle its complexities and for those transactions where a direct link between costs and revenues is discernible.

Conclusion

The matching principle is a fundamental concept in accounting that ensures expenses are recorded in the same period as the revenues they help generate. This principle, commonly used under accrual accounting standards, assists in creating a more accurate financial snapshot by aligning revenues with related expenditures. For example, in a retail company, employee bonuses should be recorded as a bonus expense within the same accounting period in which the revenues attributed to the employee’s efforts are recognized. This systematic alignment, even amidst market fluctuations and revenue allocation complexity, enhances the consistency and reliability of financial data.

Incorporating automation software, such as AR automation software, can streamline the process and reduce uncertainties or discrepancies in financial reporting. By automating data entry related to accruals or amortization, and using model templates within the accounting system, businesses can maintain consistency and minimize human error. This efficiency is crucial not only for simplifying transaction outcomes but also for ensuring liability and equity valuations reflect true business performance over the assumed lifespan of various expenditures or investments.

Despite the complexity that sometimes accompanies the implementation of accrual accounting methods, automating processes ensures that liabilities are accurately portrayed, allowing for better cash flow management and valuation assessments. As businesses strive to remain competitive, avoiding misrepresentation through accurate cash accounting entries becomes paramount. Templates and consistent application of accounting principles across various accounts can assist administrators and reps in maintaining transparency and accountability, ultimately benefiting productivity and minimizing the risks of financial misstatements.

FAQ Section

What is the matching principle in accounting?

The matching principle in accounting is a strategy that dictates companies should report expenses in the same period as the revenues they help to generate, ensuring that each period’s financial statements accurately reflect the company’s economic activities and profitability.

Why is the matching principle important for accurate financial reporting?

The matching principle is vital for accurate financial reporting as it aligns expenses with related revenues, depicting a company’s profitability and performance realistically, aiding stakeholders in making informed decisions based on true financial health.

Can the matching principle be applied under cash basis accounting?

No, the matching principle is not used under cash basis accounting. This method only recognizes revenue when cash is received and expenses when cash is paid, disregarding the matching of expenses to the revenues they help generate.

How does the matching principle differ from the revenue recognition principle?

The matching principle and the revenue recognition principle both guide accurate financial reporting, but they differ fundamentally. The revenue recognition principle determines when revenue is recognized, focusing on the exact point it’s earned, regardless of when cash is received. The matching principle, in turn, aligns the expenses directly with earning the revenue they help to produce, ensuring both are recorded in the same accounting period for consistent financial portrayal.

What are some examples of the matching principle in action?

Some examples of the matching principle include a company recognizing the cost of goods sold at the same time it records the revenue from sales, or a business amortizing the cost of an intangible asset across its useful life as it generates associated revenues. Another example is matching advertising expenses with the increase in sales revenue from the campaign period.