Imagine being able to glance at a spreadsheet and instantly know your company’s capacity to weather financial storms. That’s the power of understanding the quick ratio. It not merely reflects current health but provides peace of mind for you and confidence for potential investors. The quick ratio values forthright information, dismissing less liquid assets, thus presenting a clear-eyed assessment of your financial agility.

KEY TAKEAWAYS

- The quick ratio is a conservative measure of a company’s liquidity, indicating its ability to cover short-term liabilities with its most liquid assets. It excludes inventory from the calculation, offering a more precise insight into a company’s immediate financial capabilities without relying on the liquidation of potentially illiquid assets.

- This financial metric is not only straightforward to calculate but also vital for comparing a company’s liquidity over time or against its peers. By monitoring the quick ratio, businesses can recognize trends and address financial management issues related to profitability or inventory inefficiencies, which may be reflected in a declining ratio.

- While useful, the quick ratio is not a standalone predictor of future financial stability. To ensure a company is prepared to meet its cash flow needs, it is crucial to adopt a dynamic approach that considers upcoming sales, changes in the operating cycle, and industry benchmarks. Regular assessment of the quick ratio can lead to timely adjustments in spending and collections, contributing to overall financial health and growth.

A Brief History: Why It’s Called the “Quick” Ratio

The journey of the quick ratio through history is as intriguing as its function in today’s business finance. If you’ve ever wondered why it’s called the “quick” ratio, it’s because the financial whizzes of yesteryears wanted a method to gauge how promptly a company could turn its assets into cash—hence, the name “quick”. The term has an essence of speed and decisiveness, capturing the essence of the ratio’s purpose: evaluating a company’s immediate liquidity without counting inventory, which takes longer to liquidate.

Developed in the early 20th century, when the pace of business began to accelerate, this metric became an indispensable tool. It provided a no-nonsense snapshot of a company’s core liquidity and excluded assets that weren’t easily converted into cash, such as inventory or prepaid expenses. Over the years, the quick ratio has stood the test of time, maturing along with the economy it helps to scrutinize. Even today, in an age of complex financial derivatives and globalized commerce, the quick ratio endures as a fundamental evaluation of liquidity for businesses, big and small.

The quick ratio, also known as the acid-test ratio, is a critical indicator of a company’s financial viability and liquidity. It measures a firm’s ability to cover short-term liabilities using its most liquid assets, excluding inventories, which may not be immediately convertible to cash. This ratio is particularly relevant in the retail industry, where inventory often makes up a significant portion of current assets. By focusing on liquid assets, the quick ratio offers a more accurate reflection of a company’s reliance on readily available resources, such as cash reserves and accounts receivable. Proper use of accounting software or tools like Excel ensures accuracy in calculations, which is essential for effective financial planning and strategic decision-making.

The downsides of neglecting the quick ratio include potential over-reliance on slow-moving inventory or poorly managed receivables, which can weaken a company’s financial valuation. Regular reconciliation of accounts, alongside inventory analysis, helps mitigate risks and maintain liquidity. In conjunction with assessing profitability and cash flow, businesses can enhance their ownership position and secure a premium standing in the market. With the right financial expertise, companies can effectively use the quick ratio to make data-driven decisions, manage taxes, and strengthen their listings while ensuring long-term stability and growth.

Unveiling the Quick Ratio Formula

Breaking Down the Components

When you dive into the quick ratio, you’re essentially disassembling a financial puzzle to understand which pieces contribute to liquidity at lightning speed. Each component plays a specific role in determining how well-equipped your business is to meet short-term obligations.

Here’s a quick unpacking of the components that make up the quick ratio:

- Cash and Cash Equivalents: This includes physical currency, bank accounts, and liquid investments that can be converted to cash almost immediately.

- Marketable Securities: These are investments that you can quickly sell on public exchanges, such as stocks or bonds.

- Accounts Receivable: Money owed to your company by customers that is expected to be paid within a short timeframe.

It’s essential to exclude any inventory or prepaid expenses from this formula since these do not qualify as “quick” assets due to the longer time needed to convert them into cash. By honing in on the most liquid of assets, the quick ratio truly measures your financial reflexes.

When pieced together, these elements form the numerator of the quick ratio, balanced against the denominator—current liabilities, which represent all debts and obligations due within a year. Understanding these building blocks is like financial literacy 101—they’re the ABCs of assessing your company’s immediate financial standing.

Step-by-Step Calculation Guide with Examples

Calculating the quick ratio is like following a trusted recipe—it’s straightforward if you have all the ingredients measured and ready. Let’s go through it step-by-step:

- Tally Your Quick Assets: Add up your cash and cash equivalents, marketable securities, and accounts receivable. These are your assets that can be quickly converted to cash.

- Identify Your Current Liabilities: List all your company’s short-term obligations—anything due within a year.

- Apply the Quick Ratio Formula: Divide your quick assets by your current liabilities to find your quick ratio. The formula looks like this:

Here’s an example to bring this to life:

Assume your company has the following financials:

- Cash and Cash Equivalents: $50,000

- Marketable Securities: $20,000

- Accounts Receivable: $30,000

- Current Liabilities: $40,000

Applying the formula:

So, your quick ratio is 2.5. This means you have $2.50 in liquid assets for every $1.00 of current liabilities, suggesting a comfortable cushion for settling short-term debts.

It’s essential to regularly perform this calculation to keep current with your company’s financial buoyancy. Adjusting for real-time changes in your assets and liabilities keeps your financial decision-making sharp and informed.

The Relevance and Application of the Quick Ratio in Business

Using the Quick Ratio to Assess Financial Health

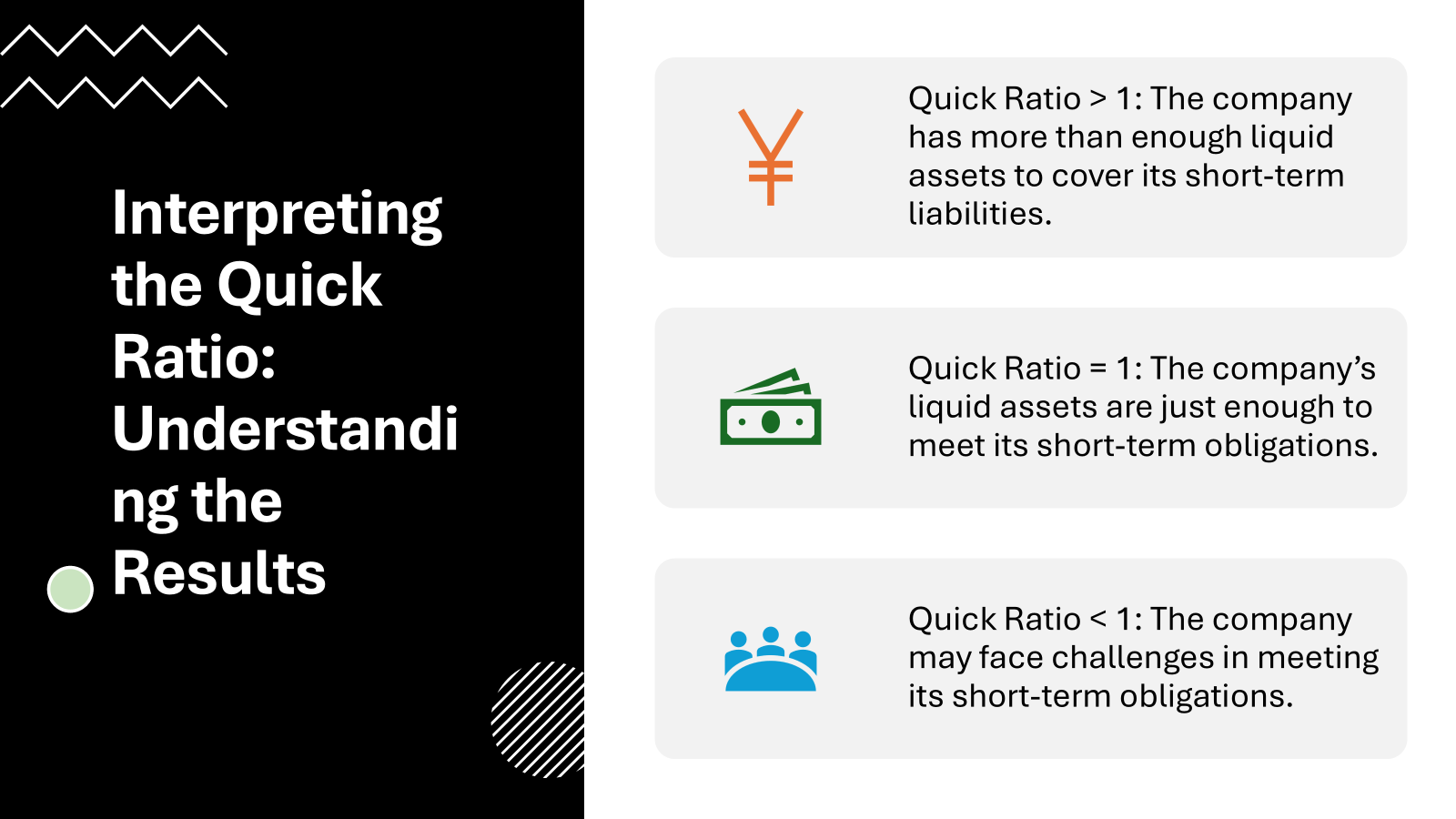

Using the quick ratio to assess financial health is akin to taking your company’s financial temperature: it provides an instant reading on your liquidity status. A higher quick ratio indicates a robust ability to cover short-term debts, reflecting strong financial health. Conversely, a lower quick ratio suggests potential liquidity challenges on the horizon.

So, why tailor a suit when you can tailor your financial strategy? By tracking the quick ratio, you can identify strengths and weaknesses in your cash flow, empowering you to make smart adjustments. Sudden dips signal the need for action, like hastening collections or freezing non-essential spending. A comfortably high ratio, meanwhile, functions as a green light for strategic investments or managing debts.

Knowing your quick ratio is like having a financial compass—it orientates you toward optimal liquidity. It gives stakeholders confidence in your company’s capacity to meet its immediate financial commitments, painting a picture of a business that is solvent and well-managed.

Real-World Scenarios: When to Rely on the Quick Ratio

When the seas of commerce get choppy, the quick ratio serves as a lifesaver to keep your business afloat in the short term. Here are some real-world scenarios where leaning on the quick ratio can be particularly insightful:

- Economic Uncertainty: If the market is volatile, knowing your quick ratio helps prepare for unexpected downturns by ensuring you have enough liquid assets to navigate challenging economic waters.

- Seeking Credit: When applying for a loan or line of credit, prospective creditors may look at your quick ratio to determine your ability to repay short-term debts.

- Investor Relations: Showing a healthy quick ratio can attract and reassure investors, indicating that their investment is in a resilient company.

- Cash Management: The quick ratio can flag cash flow issues, prompting you to adjust your cash management strategies, like accelerating the collection process or deferring certain expenditures.

- Mergers and Acquisitions: If you’re considering a merger or acquisition, the quick ratio can help you evaluate the target company’s liquidity and the potential impact on your own financials.

In essence, the quick ratio isn’t just a number—it’s a navigational tool that helps steer your business’s financial decision-making in various circumstances, from normal operations to periods of strategic change.

Comparative Analysis: Quick Ratio vs. Current Ratio

Key Differences and Similarities

When choosing between the quick ratio and current ratio, think of them as sibling metrics in the liquidity family, each offering a unique perspective on your company’s financial immediacy.

Similarities:

- Both ratios measure short-term liquidity, spotlighting your business’s ability to pay off current debts.

- They each use current liabilities in the denominator, quantifying what’s due within the next year.

- Quick and current ratios are indicators of financial stability, and are often reviewed by investors and creditors.

Differences:

- The quick ratio is the more selective sibling, considering only cash, marketable securities, and receivables, thus excluding inventory from the equation.

- The current ratio is more inclusive, factoring in all current assets, including inventory and other less liquid assets.

- Due to its stricter criteria, the quick ratio can give a more conservative perspective, making it ideal for assessing liquidity in industries where inventory doesn’t quickly convert to cash.

Briefly put, while the current ratio offers a broad view of your assets, the quick ratio provides a focused insight, particularly useful when quick liquidity is paramount.

Strategic Use Cases for Each Ratio

Knowing when to use the quick ratio versus the current ratio is like choosing the right tool for a job—it ensures precision and efficacy. Here’s how you might strategically use each ratio:

Quick Ratio:

- When Speed Matters: If your industry requires the ability to mobilize funds rapidly, the quick ratio is your go-to metric. It’s especially relevant for businesses where inventory either takes a long time to sell or has uncertain sell-through.

- During Financial Instability: In times of economic volatility, the quick ratio helps measure your immediate defensive position, providing a clear view of the assets that can quickly be liquidated.

Current Ratio:

- Comprehensive Financial Overview: If you’re interested in a broader picture of your company’s ability to meet short-term obligations, including the strategic use of inventory, the current ratio is fitting.

- Stable Industries: For sectors with fast inventory turnover or where inventory holds significant value, the current ratio may provide a more balanced view of liquidity.

By astutely applying these ratios, you can navigate your financial landscape with the foresight of a chess grandmaster, always staying several moves ahead in the game of liquidity management.

Improving Your Company’s Quick Ratio

Best Practices for Better Liquidity Management

To safeguard your company’s liquidity like a financial fortress, there are some tried-and-true practices that can help improve your quick ratio:

- Speed Up Receivables: Encourage quicker payments from customers with discounts for early settlement or tighten credit terms to enhance cash inflow.

- Trim Short-Term Liabilities: Restructure debt to more favorable terms when possible, and prioritize high-interest obligations to reduce outflows.

- Bolster Liquid Assets: Liquidate non-critical assets and invest in short-term vehicles that can be easily converted to cash without significant loss.

- Raise Inventory Turnover: Implement processes to move inventory faster, like strategic pricing or promotions, to free up cash tied in stock.

- Audit Inventory Regularly: Regular reviews can help offload underperforming stock, unloading it to inflate your liquid assets.

- Leverage Technology: Inventory management software can be a game-changer, optimizing stock levels in real-time and leading to a more favorable quick ratio.

By ingraining these best practices into your company’s operational mindset, you create a resilient buffer against fiscal draughts, keeping your business’s liquidity healthy and responsive.

Strategies for Remedying a Low Quick Ratio

If your quick ratio is signaling a red alert, don’t panic—there are strategies you can employ to get back on a stable liquidity track:

- Tighten Credit Policies: Implement stricter criteria for extending credit to customers. This can mean shorter payment terms or more rigorous credit checks.

- Accelerate Collections: Consider incentives for early payment, additional follow-up on outstanding invoices, or even third-party collections services for delinquent accounts.

- Restructure Debt: Negotiate with lenders for longer repayment terms or lower interest rates to reduce the burden of current liabilities.

- Liquidate Surplus Inventory: If you have more stock than necessary, consider discounts or sales to turn this into cash.

- Cost Control Measures: Take a hard look at your expenses and cut back on non-essential spending to enhance your cash position.

- Increase Equity: Inject more capital into the business, either through personal investment or by bringing in new investors.

With these strategies, remember that every company’s situation is unique, so tailor your approach to your specific liquidity needs. It’s like custom-tuning an engine—you’re adjusting all parts to get the performance you need.

Tips for Mastering the Quick Ratio

Understanding Nuances within Industry Standards

While the quick ratio is a universal measure, it’s important to look at it through industry-specific lenses. Each sector has its own rhythm and cadence when it comes to liquidity. For instance, technology companies might boast a lower quick ratio compared to service-oriented firms because they are often heavily reliant on inventory that is not as quickly liquefiable.

Digging into the nuances within your industry is paramount. For example, as of April 2024, the biotechnology and medical instruments industries are soaring with quick ratios above 4.5 and 2.78, respectively, highlighting their robust liquidity positions. Conversely, the discount retail sector often hovers around a quick ratio of 0.3, given their high inventory levels relative to liquid assets.

Understanding these benchmarks helps you contextualize your quick ratio, setting realistic goals and performance expectations aligned with industry liquidity standards. It’s about knowing the financial terrain of your field to strategize accordingly.

Analyzing Company Trends Through the Quick Ratio Lens

Viewing your historical quick ratios over time offers a cinematic reel of your company’s liquidity journey—a sequence of financial flashes that can reveal both progress and pitfalls. It’s like studying the pulse of your company’s financial heartbeat, looking for patterns and irregularities.

By tracking these trends, you can identify if dips in the quick ratio align with specific business decisions or external market changes. Perhaps a prolonged low quick ratio signals a systemic issue with collections or too much capital tied up in sluggish assets. On the flip side, consistently high quick ratio values might indicate an overly conservative approach that could be limiting growth potential.

Regularly analyzing your quick ratio trends helps you fine-tune your financial strategy, equipping you with the foresight to anticipate liquidity needs and adjust operations proactively.

The Impact of Quick Ratio on Credit Decisions and Risk Management

Evaluating Short-Term Solvency for Creditworthiness

When suppliers or lenders peep through the keyhole at your business, the quick ratio often greets them as a measure of your creditworthiness. They’re looking for signs of short-term solvency—that your company won’t just survive, but thrive in the immediate future.

A robust quick ratio is like a financial welcome mat, inviting in new opportunities and credit. It reassures these financial counterparts that you’re equipped to honor debts promptly, a trait that could earn you better terms or more favorable rates. A weaker ratio might necessitate some convincing or, conversely, provide the impetus to improve your liquidity management.

Keep in mind that different industries have different baseline expectations for what constitutes a “healthy” quick ratio, so do your homework to know where you stand.

Mitigating Non-Payment Risk with an Effective Quick Ratio

Maintaining an effective quick ratio is like having a financial shield against the risk of non-payment. If customers are slow to pay or default, a strong quick ratio ensures that you have enough liquid assets on hand to cover short-term liabilities without a flinch. It’s a buffer that allows you to navigate customer payment unpredictability with less risk to your own solvency.

Here’s how a robust quick ratio can help:

- It creates resilience against the downtime in collections, preventing a domino effect on your payables.

- It signals to your suppliers and partners that, despite customer payment behaviors, your commitments will be met on time.

In short, a quick ratio that reflects a healthy balance of liquid assets arms you against the ripples of non-payment, enabling your business to continue operations smoothly and maintain credibility in the marketplace.

Limitations and Considerations for the Quick Ratio

Recognizing Potential Misinterpretations

Navigating the financial seas with the quick ratio as your compass is wise, but beware of potential misinterpretations that can send you off course. For instance, a high quick ratio may not always herald financial health if it reflects excessive cash that could be otherwise invested for growth.

On the flip side, a low quick ratio doesn’t necessarily spell doom, especially if your company has solid long-term prospects or easy access to financing options. It’s crucial to interpret this metric within the broader context of your business model and industry norms.

Remember, the quick ratio is a snapshot, not the whole album, and it should be reviewed alongside cash flow analysis and other financial indicators to create a complete picture of liquidity.

Where the Quick Ratio Falls Short

The quick ratio provides an expedient glance at a company’s liquidity, yet it’s not without its blind spots. Take, for example, its exclusion of inventory. This can skew perspectives, particularly in retail or manufacturing sectors where inventory turns over rapidly and is indeed ‘quick’.

Furthermore, the quick ratio is a momentary snapshot and cannot gauge the effects of future income or expenditures that might significantly alter a company’s liquidity. It also doesn’t take into account the quality of accounts receivable; not all receivables may be collectible within the quick timeframe implied by the ratio.

Another limitation is the ratio’s silence on a company’s capital structure. It does not differentiate between debt financed through high-interest loans or low-cost credit facilities, giving only a surface perspective on a company’s debt situation.

It is clear, then, that while the quick ratio can highlight potential liquidity issues, it should not stand alone as a measure of financial health. It’s a piece of the puzzle but not the full picture, requiring other financial metrics and qualitative considerations for a holistic financial diagnosis.

Practicing Quick Ratio Analysis

Practical Exercises to Hone Financial Analysis Skills

To master financial analysis, you need to practice, much like a musician learning a new piece. Here are some practical exercises to help you hone your skills in quick ratio analysis:

- Historical Data Review: Pull historical financial statements of your company or a publicly traded company. Calculate the quick ratio for each period and analyze the trends.

- Scenario Analysis: Create ‘what-if’ scenarios. How would the quick ratio change if accounts receivable collection period increased? What if you negotiated extended payment terms with suppliers?

- Industry Comparison: Compare the quick ratios of companies within the same industry. How do they stack up against each other? Which companies exhibit stronger liquidity management?

- Role Play: Take on the role of a credit analyst. Using quick ratio and other financial data, decide whether to extend credit to a business or not.

- Interpretation Challenge: With a partner, interpret the same set of quick ratio data differently, then discuss how and why your interpretations vary.

By practicing these exercises, you’ll strengthen your financial analysis muscles, allowing you to grasp the nuances of the quick ratio and use this metric to make informed business decisions.

Incorporating Quick Ratio Insights into Broader Financial Contexts

Embedding the insights gleaned from the quick ratio into a broader financial context is like setting a solitary piece into a mosaic—it’s where the true picture emerges. To do this effectively:

- Integrate with Cash Flow Analysis: Dialogue with your cash flow statement to understand how your liquid assets are being generated and used over time.

- Balance with Other Ratios: Use the quick ratio in concert with other financial metrics such as the debt-to-equity ratio, return on assets, or profit margins, to paint a more comprehensive picture of financial health.

- Trend Analysis Over Time: Look at how your quick ratio has changed across different periods and why. Consider external factors such as market conditions and internal factors like changes in business operations.

- Industry Benchmarking: Compare your quick ratio to industry benchmarks to position your company relative to its peers.

- Strategy Alignment: Ensure that your quick ratio aligns with your business strategy—whether it’s aggressive growth necessitating more liquidity or steady operations with less rapid turnover of assets.

Remember, the quick ratio provides deep insights, but it’s when you weave those insights into the broader financial narrative that you truly command your company’s fiscal story.

Frequently Asked Questions About the Quick Ratio

How to compute quick ratio using financial data?

To compute the quick ratio using your financial data, follow these steps:

- Total your quick assets, which include cash, marketable securities, and accounts receivable.

- Sum up your current liabilities, such as short-term debt and accounts payable.

- Divide your quick assets by your current liabilities.

The resulting figure is your quick ratio, showing you how many times you can cover your short-term obligations with your quick assets.

Example: If you have $30,000 in quick assets and $15,000 in current liabilities, your quick ratio is 2 ($30,000 / $15,000), indicating good liquidity.

What Constitutes a Good Quick Ratio?

A good quick ratio generally falls around 1 to 1.5, indicating that a company has enough quick assets to cover its current liabilities once over. However, a good ratio may fluctuate based on industry standards and should ideally meet or exceed those benchmarks for solid financial footing.

How Can Inventory Impact the Quick Ratio Calculation?

Inventory can significantly impact the quick ratio since it’s excluded from the calculation. A business with high inventory levels may have a lower quick ratio, but if the inventory turns over rapidly, it might not accurately reflect short-term liquidity. Each industry’s approach to inventory will vary the ratio’s interpretation.

How Often Should a Company Calculate Its Quick Ratio?

A company should calculate its quick ratio regularly, at least quarterly. Consistent monitoring can track liquidity trends, pinpoint issues, and guide strategic financial decisions. During volatile periods, more frequent analysis may be prudent for an up-to-date financial health snapshot.

How to find the quick ratio when given current assets and liabilities?

To find the quick ratio from current assets and liabilities, subtract inventory and any prepaid expenses from the current assets to calculate your quick assets. Then, divide this result by the current liabilities. This will give you the quick ratio, reflecting how well you can cover short-term obligations without selling inventory.

Is the Quick Ratio A Reliable Indicator in All Sectors?

The quick ratio is not equally reliable in all sectors, as it doesn’t account for industry-specific factors like inventory turnover or payment cycles. Therefore, it’s best used for comparison within the same industry and supplemented with other financial metrics for a fuller picture of liquidity.

How to work out quick ratio for small businesses or startups?

For small businesses or startups, work out the quick ratio by totaling cash, marketable securities, and accounts receivable—considered liquid assets. Then, divide by current liabilities. This calculation helps assess if there are sufficient liquid assets to cover short-term obligations, crucial for growing businesses with limited financial reserves.