KEY TAKEAWAYS

- Importance of Average Collection Period for Cash Flow: The average collection period is a crucial metric that reflects how long it takes for a company to receive payment from customers after issuing an invoice. It is essential for businesses to keep this period short to maintain strong cash flow and ensure the effectiveness of their collection policies. A prolonged collection period can lead to reduced profitability and may result in financial difficulties.

- Insight into Collection Strategies and Credit Terms: Using the average collection period formula allows businesses to evaluate the efficiency of their debt management and collection strategies. It aids in determining the optimal credit terms to offer customers, deciding when it might be necessary to write off a debt as uncollectable, and understanding the company’s creditworthiness. This formula serves as a valuable diagnostic tool for financial management and indicates whether a business needs to optimize its collections process.

- Facilitation of Business Growth and Profit Maximization: Monitoring the average collection period helps businesses gain insight into payment patterns and evaluate how quickly customers settle their debts. This knowledge is pivotal for companies to ensure they are receiving payments swiftly enough to support business growth and increase yearly profits. If the average collection period is found to be too long, businesses may consider employing automated accounts receivable (AR) services like Billtrust to streamline – Determines Payment Collection Efficiency: The average collection period formula is crucial for businesses to gauge the efficiency of their debt collection processes. A shorter average collection period indicates a more efficient collection process and faster conversion of credit sales into cash, which is vital for sustaining operations and funding new investments.

- Impacts Financial Decision Making: The formula provides essential data that influences various financial decisions, such as setting credit policies, determining when to write off debts as uncollectible, and assessing the company’s creditworthiness. By analyzing this metric, businesses can adjust their credit terms and collections strategies to improve financial health.

- Benchmarks for Financial Optimization: Tracking the average collection period can help companies set benchmarks against industry standards, and identify areas for improvement in their accounts receivable management. This aids in optimizing cash flow and could lead to increased profitability through timely receivables collection and better management of customer credit.

Understanding the Basics Before Calculating

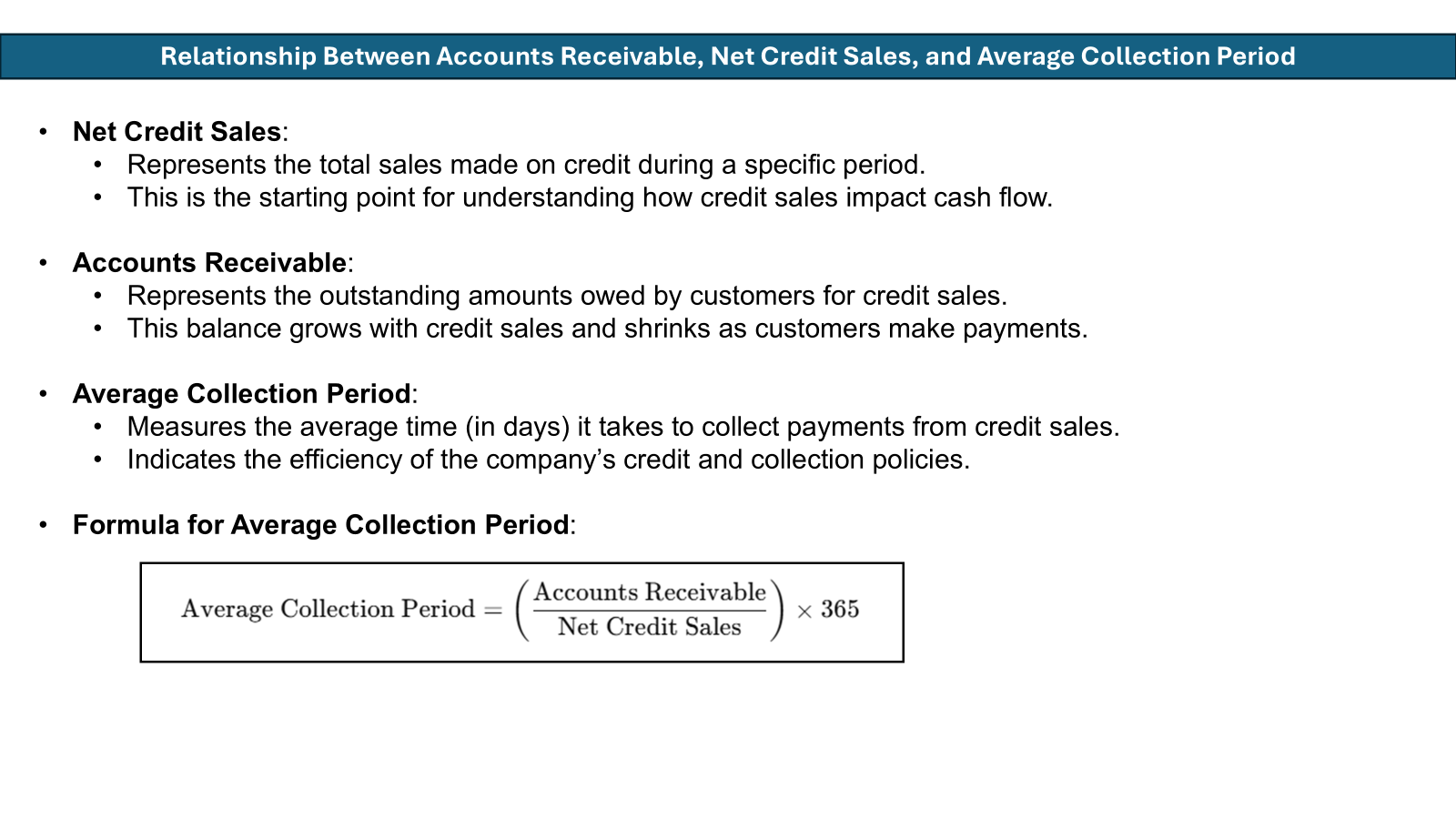

Before you dive into calculating the Average Collection Period, you’ll want to grasp some fundamentals. It’s crucial to have a firm grasp on the components such as the average accounts receivable (AR) balance – which is a more reliable measure than using just the year-end AR balance to avoid skewed results. Understand that this metric is concerned with credit sales – not cash sales – as it measures the effectiveness of your AR service and collection practices. You’ll be looking at accounts receivable, which represent the money owed by customers, and net credit sales during a given period. These figures lay the groundwork to determine how quickly you’re turning receivables into cash and if your ar service practices are up to par. Knowing these basics sets the stage for a more accurate calculation and insightful understanding of your business’s financial health.

Breaking Down the Calculation

Formula for the Average Collection Period

Calculating the Average Collection Period involves two key formulas that you can use depending on the data available:

- 365 Days / Receivables Turnover Ratio – This approach leverages the number of days in a year and divides it by the receivables turnover ratio. This vital financial metric assesses how effectively your company converts credit sales to cash, matching net credit sales with the average accounts receivable balance.

- Average Accounts Receivable Balance / Average Credit Sales Per Day – This method is particularly useful when daily credit sales data is at your disposal. By calculating your average accounts receivable balance against the average daily credit sales, you can figure out the typical duration it takes to complete payment collections.

These formulas not only quantify the speed of cash collection but also reflect on the health of a company’s credit terms and collection processes. Selecting the correct formula for your business vitally hinges on your particular accounting practices regarding recording of credit sales and receivables.

Example: Step-by-Step Computation

Let’s say you want to calculate the Average Collection Period for your business for the previous year. Here’s how you’d go about it step by step:

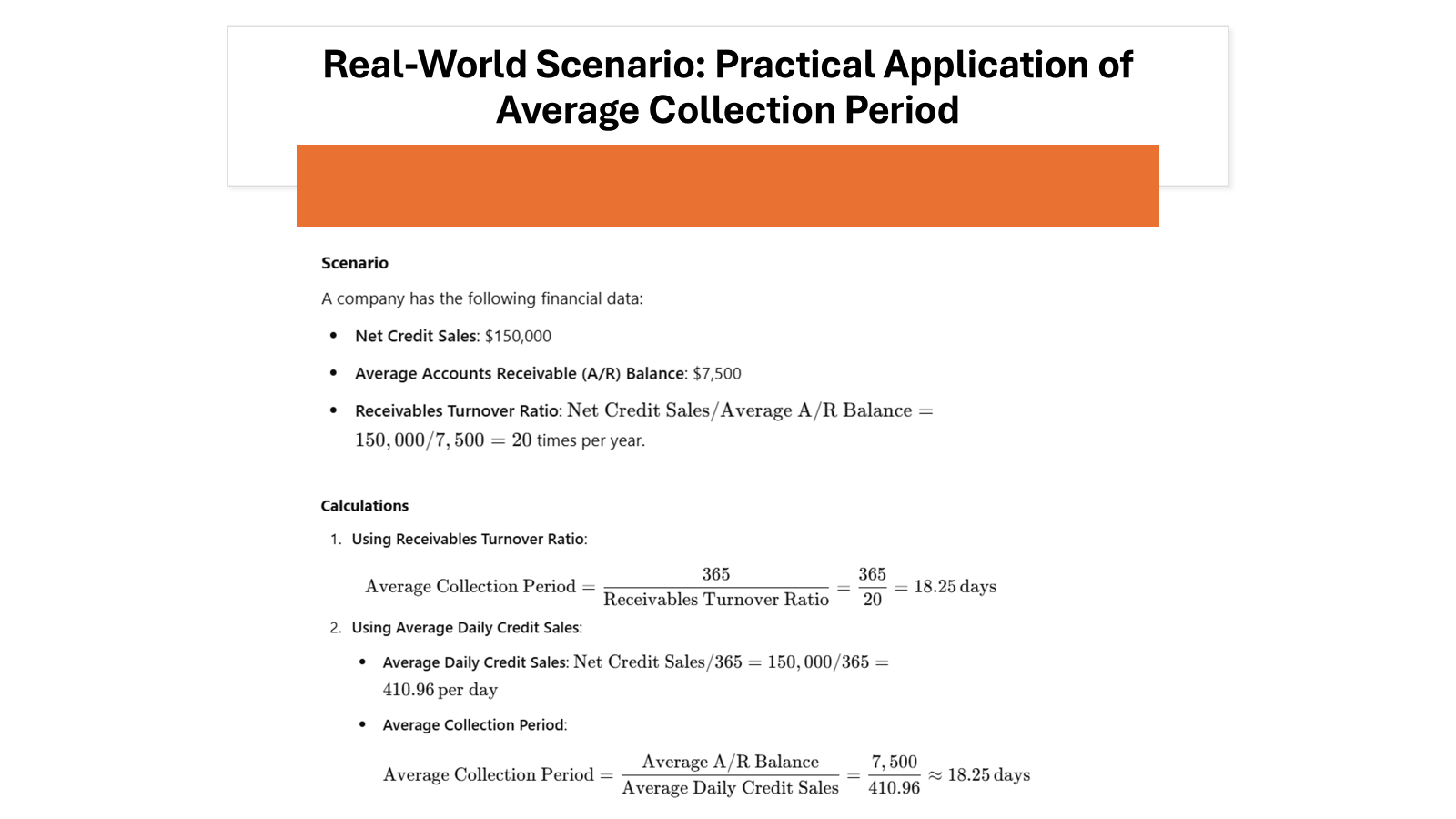

- Determine Your Net Credit Sales: Imagine your total sales on credit amounted to $150,000 last year. However, $10,000 of those sales were returned, bringing net credit sales to $140,000.

- Calculate Your Average Accounts Receivable: To avoid skewed results from an atypical year-end balance, if, for instance, at the beginning of the year, your accounts receivable was $20,000 and it was $30,000 at the ending AR marker, the average would be (20,000 + 30,000) / 2, which equals $25,000.

- Choose Your Formula and Compute: Using the average balance method, take your net credit sales ($140,000), divide by the days in the year (365), to determine the average daily credit sales ($383.56). Then, divide your average accounts receivable ($25,000) by this number for the Average Collection Period, which is approximately 65 days.

In this example, it takes, on average, 65 days to collect payments from credit sales. It’s a straightforward process, but it’s crucial for keeping a pulse on your cash flow and understanding the effectiveness of your current credit policies.

Importance and Implications

Significance of Monitoring Your Average Collection Period

Monitoring your Average Collection Period is significant for several reasons. It offers insights into how effectively you’re managing your credit and collections. A shorter period suggests that you’re quickly converting sales into cash, which bolsters your liquidity – that’s essential for meeting short-term obligations and investing in growth opportunities. Conversely, a longer collection period may indicate potential issues with your credit policies or the financial health of your customers, possibly tying up funds that could otherwise be used more productively. Regularly checking this metric can help you identify trends, such as seasonal variations in customer payment behavior, and take proactive measures to tighten up your collection strategies before they impact your business negatively.

What Does Your Average Collection Period Indicate?

Your Average Collection Period is a telling indicator of your business’s financial and operational efficiency. If the period is short, congratulations are in order—they’re a testament to your adept credit management and efficient collections process. This can mean you’re getting cash back into your business swiftly, which is critical for paying expenses, purchasing inventory, and keeping your operations running smoothly.

On the flip side, a lengthy collection period can signal trouble. Perhaps your credit terms are too lenient or your collection process needs tightening. It may hint at deeper issues, like customers experiencing financial difficulties, which could risk your own cash flow. In essence, this metric is a health check for your business, flagging areas where you might be vulnerable and where streamlined processes could reinforce your financial stability.

Using the Average Collection Period Wisely

Comparing Against Industry Norms

Comparing your Average Collection Period against industry norms can be eye-opening. It places your results in the context of a broader economic landscape, showing you where you stand among peers. If your period is significantly lower than the industry average, your credit and collection policies might be more aggressive than necessary, potentially scaring away customers who require more flexibility. However, if it’s higher, there’s a chance that your policies are lax, exposing you to higher credit risk and slower cash inflow.

To get the most accurate picture, aim to compare with businesses of similar size and credit terms within your industry. This can help you gauge whether your practices are holding you back or pushing you ahead of the competition.

Strategies to Optimize Your Collection Process

To optimize your collection process, you can employ a variety of strategies. Consider automating your accounts receivable (AR) processes with tools like Billtrust, which streamline and accelerate billing, minimizing human error and freeing up time to focus on core business aspects. Proactive collections approaches also pay dividends; establish clear communication channels with customers and follow up promptly on overdue accounts.

Another strategy is to enhance the order-to-cash process, turning it into a well-oiled machine that reduces Days Sales Outstanding (DSO). Such methods not only quicken cash inflows but also improve customer satisfaction by providing a smooth, professional transaction experience.

With these optimizations, you could see a shorter collection period, stronger cash flow, and ultimately, a more robust financial position for your business.

Practical Tips to Improve Your Collection Period

Reviewing and Updating Credit Policies

Regularly reviewing and updating your credit policies is a must for ensuring that they align with current market conditions and your business objectives. Reevaluate your credit terms, like net 30 or net 60, to ensure they are still appropriate for the type of customers you serve and the level of risk you’re comfortable taking. You might find that certain customers warrant stricter terms due to past late payments, while others could qualify for more lenient terms due to a consistent track record of timely payments.

Adjustments to your credit policies can directly impact the Average Collection Period by either speeding up or slowing down cash inflow. Just remember, any changes should be communicated clearly to your customers to maintain transparency and good relations.

Benefits of Offering Early Payment Incentives

Offering early payment incentives is a tried-and-true method to boost your collection efforts. Encouraging clients to settle their accounts earlier than the due date can significantly shorten your Average Collection Period. Let’s say you offer a small discount, such as 2% off, if the invoice is paid within 10 days—this can motivate customers who are looking to save some funds and ensures that you receive payment well within your desired timeframe.

The beauty of this strategy lies not only in its simplicity but also in its dual benefits: enhancing customer relationships through positive reinforcement while bolstering your cash flow. It’s a win-win for both you and your clients and can be a competitive advantage in the marketplace.

Top 5 features:

- Faster cash inflows

- Reduced credit risk exposure

- Enhanced customer satisfaction

- Potential competitive edge

- Improved liquidity for reinvestment or expenses

Benefits:

- Encourages timely payments

- Creates a positive reward system for customers

- May reduce the need for collection efforts and associated costs

- Can improve financial forecasting with more predictable cash flow

- Strengthens customer loyalty with incentives

Cons:

- Potentially reduced revenue from discounts given

- Risk of dependency on incentives for timely payments

Best for: Businesses looking to improve cash flow and customer goodwill while potentially sacrificing a small portion of their margin for faster payment.

Limitations and Considerations

Recognizing Potential Drawbacks

While leveraging the Average Collection Period as a financial barometer has its merits, it’s crucial to recognize potential drawbacks. For one, it represents an average, meaning outliers—customers who pay exceptionally early or late—can skew the figure, offering a distorted view of your collection efficiency. Moreover, this average doesn’t provide a detailed breakdown by customer, so it’s not effective for identifying specific late payers who could be edging towards default.

To avoid making decisions based on potentially misleading data, supplement the Average Collection Period with other measures like the accounts receivable aging report. This provides granular details of due receivables, helping you pinpoint where to focus your collection efforts for more impactful results.

Adjustments for More Accurate Analysis

For a more precise analysis of your Average Collection Period, consider making adjustments that account for seasonal sales patterns, new product launches, or changes in credit policy. These factors can cause spikes or dips in sales volume, which might not represent the typical collection experience. For instance, if you’ve just had a major product rollout, your collection period might be artificially low due to an influx of cash.

Moreover, if you’re noticing significant variations, it might be worth breaking down the calculations monthly or even weekly. This can give you a finer-grained understanding of collection patterns over time, enabling you to adjust your business strategies more responsively.

Lastly, don’t forget to adjust for any one-off events or non-recurring sales that may not be reflective of ongoing business. By doing so, you’ll refine the accuracy of your analysis, ensuring that the insights you gather truly reflect your business’s collection and cash flow situation.

Tools and Resources for Calculation

Average Collection Period Calculators and Templates

Calculators and templates designed for the Average Collection Period can be powerful allies in your financial toolkit. They not only streamline the computation process but also ensure greater accuracy by minimizing the risk of manual errors. Many online finance platforms and accounting software include built-in calculators that can automatically pull and process the required data from your accounting records.

Excel templates are another helpful resource. They can be customized to your specific needs and often come with pre-programmed formulas to make calculations as simple as inputting your net credit sales and average accounts receivable figures. These resources save time and provide a consistent format for analyzing trends over periods.

Utilizing Software for Streamlined Tracking

Embracing software solutions for tracking your Average Collection Period can transform the way you manage accounts receivable. These systems automate much of the legwork involved in calculating this KPI, leaving you more time to analyze the results and strategize improvements. Look for software that seamlessly integrates with your existing accounting platform and provides real-time insights into your receivables.

Additionally, AR software often comes with customizable alerts and dashboards, helping you stay ahead of any collection issues that may arise. By choosing a robust software system, you can enjoy streamlined tracking, proactive management of receivables, and a healthier cash flow position for your business.

FAQs

What is the average collection period Ratio?

The average collection period ratio is a measure of the time it typically takes a business to receive payments owed by its customers. It’s calculated by dividing the average accounts receivable by the total net credit sales and then multiplying the result by the total number of days in the period. This ratio provides insight into the efficiency of a company’s credit and collection policies.

The average collection period formula is a key financial metric that evaluates how efficiently a company collects payments from its customers. It is calculated using the formula:

Average Collection Period=(Accounts Receivables Balance / Net Credit Sales)×Number of Days in the Period

This formula offers a snapshot of a company’s credit management effectiveness. For instance, if Company A has a shorter average collection period, it means they are collecting payments more quickly, improving cash flow and reducing liabilities. Businesses can use this information to optimize productivity by negotiating better terms with suppliers or offering discounts for early payments, aligning their practices with industry benchmarks.

How do you interpret a company’s average collection period?

Interpreting a company’s average collection period involves comparing it against the credit terms extended to customers. If the period is shorter than the credit terms, it suggests efficient collections and a strong cash flow. Conversely, a longer period than the credit terms could mean delays in receiving payments, signaling potential issues with credit policies or customer payment habits that might need addressing.

What are some effective methods to reduce the average collection period?

Effective methods to reduce the average collection period include:

- Streamlining the invoicing process for quicker billing.

- Offering various payment options to make it easier for customers to pay.

- Implementing early payment discounts to incentivize faster payment.

- Enforcing strict credit policies and following up promptly on overdue accounts.

- Utilizing automated reminders for upcoming or past-due invoices.

How to calculate average Accounts receivable?

To calculate the average accounts receivable, simply add the beginning and ending balances over a certain period—often a month or a year—and then divide by two. This gives you the average amount of receivables during that period, allowing for a fair representation over time, rather than relying on a potentially fluctuating end-of-period number.

What is the accounts receivable days formula and how is it used?

The accounts receivable days formula, commonly known as Days Sales Outstanding (DSO), measures the average number of days it takes a company to collect payment after a sale has been made. The formula is: (Average Accounts Receivable / Net Credit Sales) * Number of Days. Businesses use it to assess the efficiency of their credit and collections process and to understand their liquidity position regarding receivables.