KET TAKEAWAYS

- The discounted payback period accounts for the time value of money, which is crucial when comparing the financial viability of different investment projects. It emphasizes that money received in the future is not worth as much as money received today due to factors like inflation and lost opportunity for alternative investments.

- Calculating the discounted payback period helps investors and businesses determine the time it will take for a specific project to become profitable by considering the discounted cash flows. Shorter payback periods are typically perceived as less risky, as there is a shorter timeframe for potential negative market or policy changes to affect returns.

- A practical advantage of using the discounted payback period is its simplicity and ease of understanding for stakeholders, which streamlines the decision-making process. It allows for straightforward evaluations of liquidity and provides a clear time frame for when the invested capital will be recovered, thereby aiding in efficient capital allocation.

The Importance of Time Value in Investment Decisions

Delving into the realm of investment—and particularly within the sphere of investment banking—one cannot overlook the principle that a dollar in their pocket today has more potential than the same dollar tomorrow. This foundational understanding is crucial for investment banking professionals, who analyze the time value of money as the bedrock of the Discounted Cash Flow (DCF) formula, a core component of financial modeling. This concept acknowledges that money available now is preferable because it can be invested to earn a return. When they’re making investment decisions, whether in personal portfolios or within the ambit of investment banking, they’re essentially choosing to forgo current spending in hopes of future financial benefits. The importance of this principle cannot be overstated; it forms the basis for most investment appraisal techniques, including the DPP. By considering the time value of money, they ensure that they’re not just recouping their initial outlay of capital, but also earning on it as if it had been invested elsewhere, which is a fundamental tenet in investment banking valuations.

Breaking Down the Formula

Components of the Discounted Payback Period Equation

To navigate the waters of the Discounted Payback Period equation, let’s break down its components. Firstly, there’s the initial investment – defined as the amount of money thrown into the ring to kickstart a project or investment. This is where the profitability index can first be considered, gauging the potential profitability of a project by comparing the present value of future cash flows to the initial investment. Next, they’ve got the expected cash inflows, which are the future payments they anticipate from their investment, adjusted for the time value of money. Lastly, the discount rate comes into play, acting like financial gravity pulling the future cash back to present value. Each element is crucial, and when they tweak any of these components, the DPP adjusts accordingly, giving them a dynamic tool for assessing the profitability timetable of an investment.

If a company is using the discounted payback period but they are not sure of their discount rate, they can use the Weighted Average Cost of Capital (WACC).

“Understanding the interplay between the initial outlay, expected cash inflows, and the discount rate is vital. Alterations to any piece of the Discounted Payback Period puzzle can significantly affect your calculations and the resulting visibility into an investment’s payback timeframe,” notes a prominent financial analyst.

A Closer Look at Cash Flows and Discount Rates

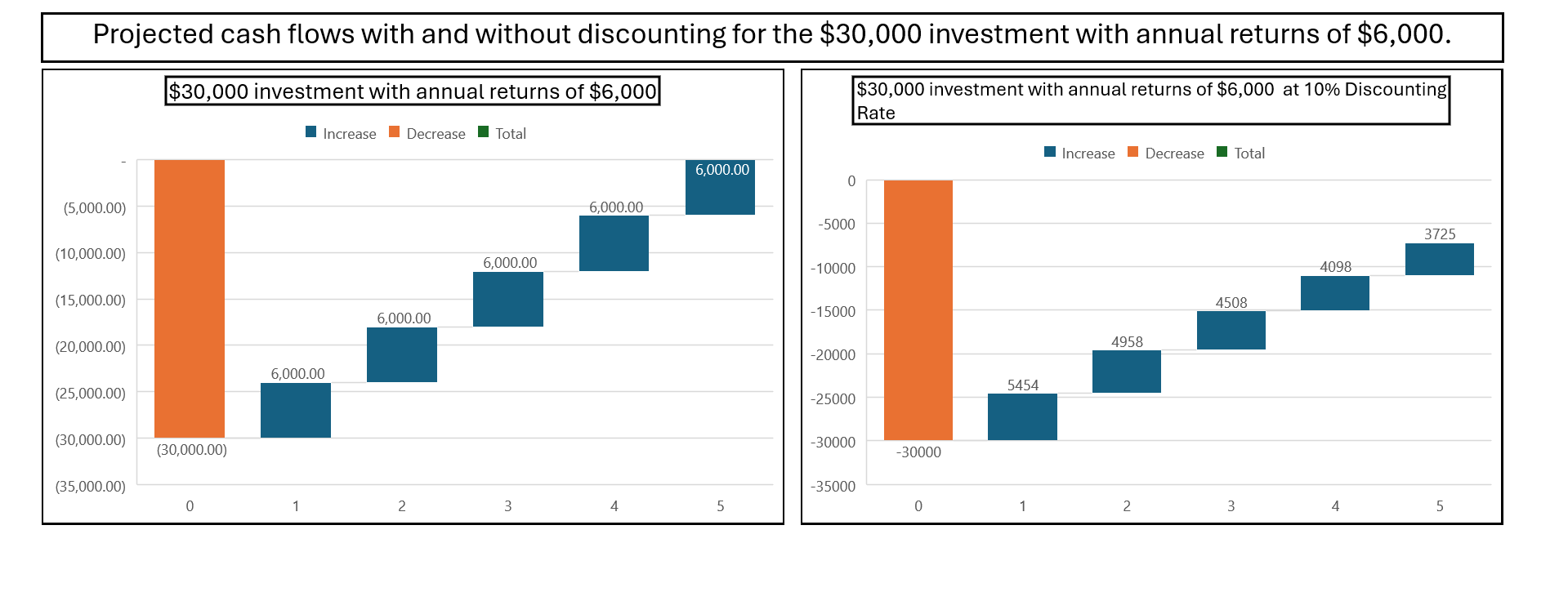

Cash flows and discount rates are the heart and soul of the Discounted Payback Period. Cash flows represent the lifeblood of an investment—the expected stream of money generated over time, like the anticipated cash outflow of capital for projects or ventures. These aren’t just random numbers—they reflect the real-world financial benefits derived from the investment, whether it’s a new product launch or a real estate venture. When considering a project with a typical initial cash outflow, such as a $30,000 investment with annual returns of $6,000, the wise investor looks to recoup that cost / expenditure within the project’s lifetime. But not all cash is created equal; cash tomorrow isn’t worth as much as cash today. That’s where the discount rate steps in—it’s the financial sieve that filters out the rosy optimism, grounding future cash flows in today’s dollars. They need to choose a discount rate that reflects the risk and the opportunity cost of their investment, ensuring a clear-eyed assessment of when the investment is expected to payback and considering the higher value of the current cash outflow compared to future inflows.

Calculating Discounted Payback Period by Example

Step-by-Step Calculation with a Real-World Scenario

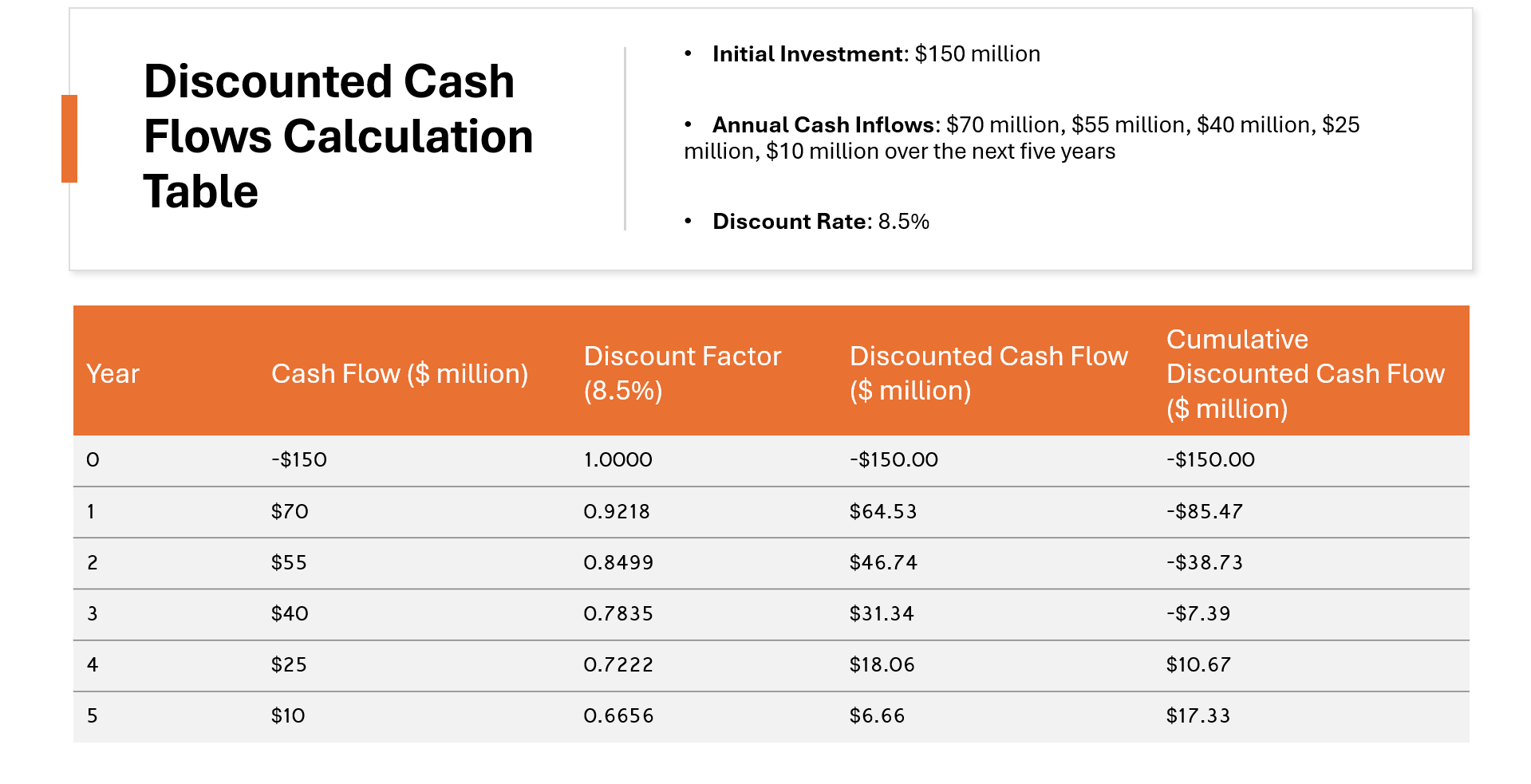

Imagine they’ve got a fresh project on their hands, and they need to calculate the Discounted Payback Period. Here’s how they’d typically approach it: first, take the estimated after-tax cash flows over the project’s life. Suppose the project requires a $150 million initial investment with expected annual cash inflows of $70 million, $55 million, $40 million, $25 million, and $10 million over the next five years respectively.

- They’ll need to discount these cash flows to their present value using the chosen discount rate—for instance, 8.5% to account for the project’s risk profile.

- Then, add up the discounted cash flows year by year until they eclipse the initial investment.

- The moment the cumulative cash meets or exceeds their initial outlay, voilà—that’s the discounted payback period.

By following these steps with real numbers in an Excel spreadsheet or a DPP calculator, they’ll have a clear forecast of when their project will reach its financial breakeven point.

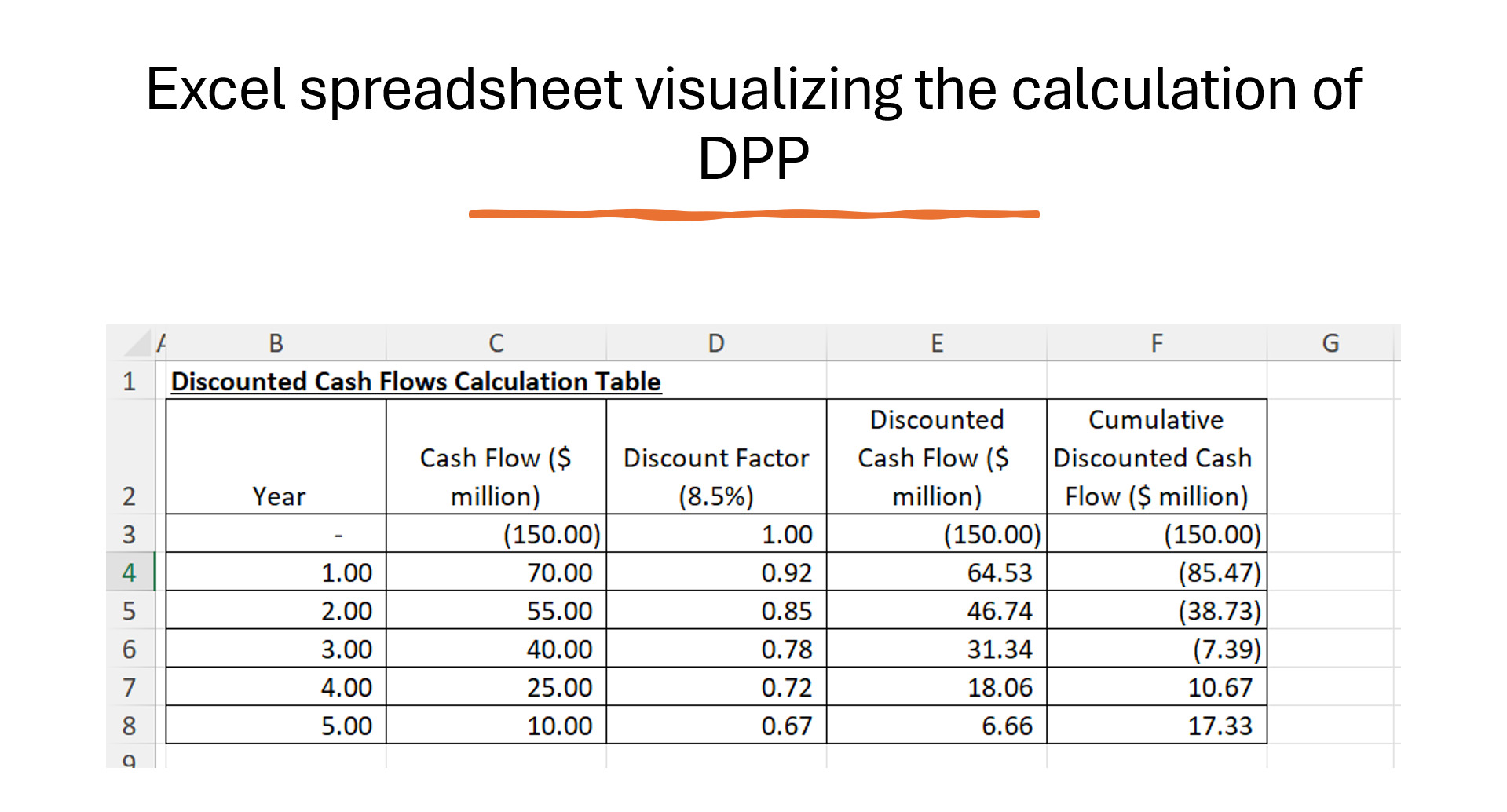

Visualizing the Process Through Excel

Taking to Excel, they can translate their investment scenario into a crystal-clear visual roadmap. To calculate the Discounted Payback Period here, they’ll start by entering each year’s forthcoming cash flows into a worksheet. Next up, they’ll apply the discount rate to each cash flow to calculate its present value. Once they’ve done that, they’ll sum up these discounted cash flows cumulatively until the initial investment is recovered. The beauty of Excel is its ability to churn through the numbers swiftly. They just provide the initial numbers, and with a few formulas, Excel paints the whole picture—a table or chart tracking the trek of discounted inflows crossing the break-even point.

Remember, the year when the cumulative discounted cash inflow surpasses the initial outlay marks the discounted payback period. They’ll be pinpointing the precise moment in time when their investment transitions from cost to profit, all neatly laid out in their Excel grid.

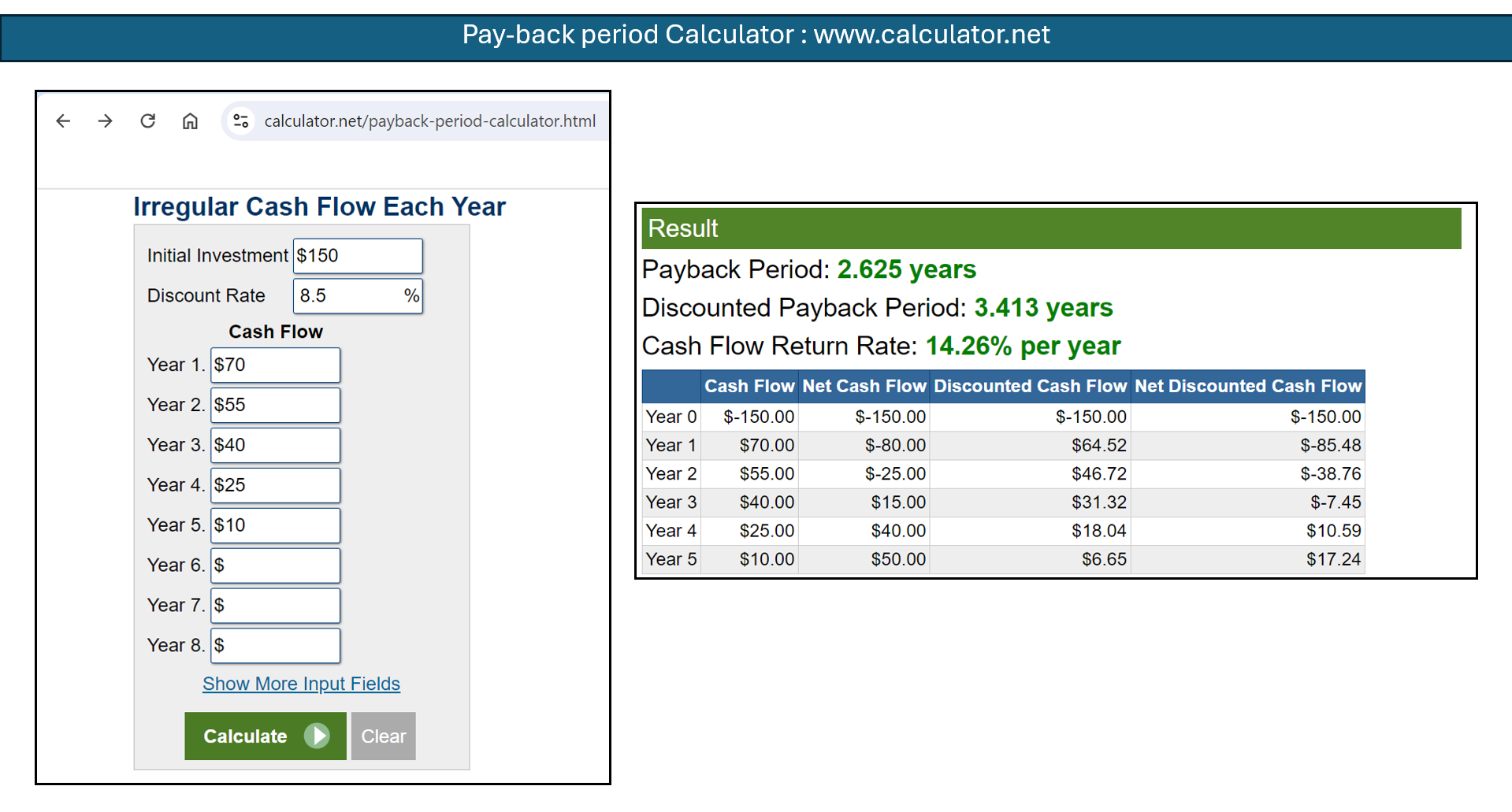

Using DPP Calculators

For those who want to skip the complexity of spreadsheets or just need a quick estimate, DPP calculators are a handy tool. These nifty online widgets are designed to crunch the numbers in a heartbeat. All they need to do is inputs their initial investment, their stream of expected cash flows, and their chosen discount rate, and the DPP calculator does the heavy lifting. It offers the advantage of simplicity and speed, making it an ideal choice for brisk investment assessments. Plus, these calculators often come with additional features to help them visualize the payback timeline or compare different scenarios at a click.

Decision-Making with Discounted Payback Period

When it comes to making investment decisions, the Discounted Payback Period is like a trusty compass pointing to projects that promise quicker returns, adjusted for the time value of money. By measuring how fast they’ll recover their investment, it helps them gauge risk and liquidity. If the DPP is shorter than the project’s expected life or a pre-set benchmark, they’re likely looking at a worthwhile venture. On the flip side, a longer DPP might signal caution or prompt them to explore other opportunities. No one likes their capital tied up in a sluggish investment, after all. Ultimately, combining DPP with other evaluation tools offers a more rounded financial analysis, empowering businesses to make smarter, more informed investment calls.

Comparison with Other Investment Appraisal Techniques

Discounted vs. Simple Payback Period: The Key Differences

When distinguishing between the Discounted and Simple Payback Periods, you’re essentially pitting apples against more financially savvy apples. The Simple Payback Period is like the straightforward friend who tells them how many years it’ll take to get their investment back, no frills attached. On the other hand, the Discounted Payback Period is that friend who also considers the decreasing power of money over time. It answers the same question but takes into account the time value of money—ensuring they don’t overestimate long-term cash flows and that they’re truly comparing apples to apples regarding today’s value. It’s a more nuanced approach which often results in a longer payback period, but one that’s more aligned with the real-world financial landscape they operate in.

How DPP Complements Net Present Value (NPV) and Internal Rate of Return (IRR)

The Discounted Payback Period, Net Present Value (NPV), and Internal Rate of Return (IRR) form a stellar trio in the investment analysis concert. While DPP offers a sneak peek at how quickly the investment recoups its cost, NPV takes the longer view by measuring total profitability over the investment’s entire horizon. The IRR, for its part, sings the tune of the investment’s efficiency by highlighting the expected rate of growth.

Leveraging DPP alongside NPV and IRR gives them a symphonic perspective. DPP highlights liquidity and risk exposure by focusing on the payback timeframe, whereas NPV and IRR accentuate overall viability and return rate. When used in harmony, they provide a comprehensive financial composition that allows investors to hit all the right notes in making savvy, balanced investment choices.

FAQs About Discounted Payback Period

What is the basic difference between Payback Period and Discounted Payback Period?

The basic difference lies in how they treat the time value of money. The Payback Period measures how long it takes to recoup an investment based on nominal cash inflows, ignoring when the inflows occur and their present value. The Discounted Payback Period, however, adjusts these cash inflows to their present value using a discounting factor, offering a more realistic timeline for when an investment pays back.

Can the Discounted Payback Period be used for all types of investments?

While versatile, the Discounted Payback Period may not be suitable for all investments. It’s most effective for investments with regular, predictable cash flows. It might not be as reliable for investments with erratic or speculative cash inflows due to the complexity of accurately discounting such flows.

How does the choice of discount rate affect the Discounted Payback Period?

The choice of a discount rate directly impacts the Discounted Payback Period—selecting a higher rate devalues future cash flows more, extending the payback period, while a lower rate means a shorter payback period. It’s essential to choose a rate reflecting the investment’s risk and the opportunity cost of capital.

What are the limitations of using Discounted Payback Period as an investment appraisal method?

The Discounted Payback Period’s major limitation is its disregard for cash flows beyond the payback point, potentially overlooking a project’s total profitability. Also, it doesn’t provide a concrete yes-or-no investment decision like NPV or IRR might. Furthermore, estimating an appropriate discount rate can be challenging and subjective—an inaccurate rate may significantly affect the outcome.