KEY TAKEAWAYS

- The cash flow statement using the indirect method is structured around three types of activities: operating activities, investing activities, and financing activities. It highlights cash inflows and outflows within each activity, helping businesses track their cash usage and generation. This approach is favored for its simplicity and is commonly used by businesses of all sizes, with accounting software like Lili’s making it even more accessible by automatically categorizing transactions and generating cash flow statements.

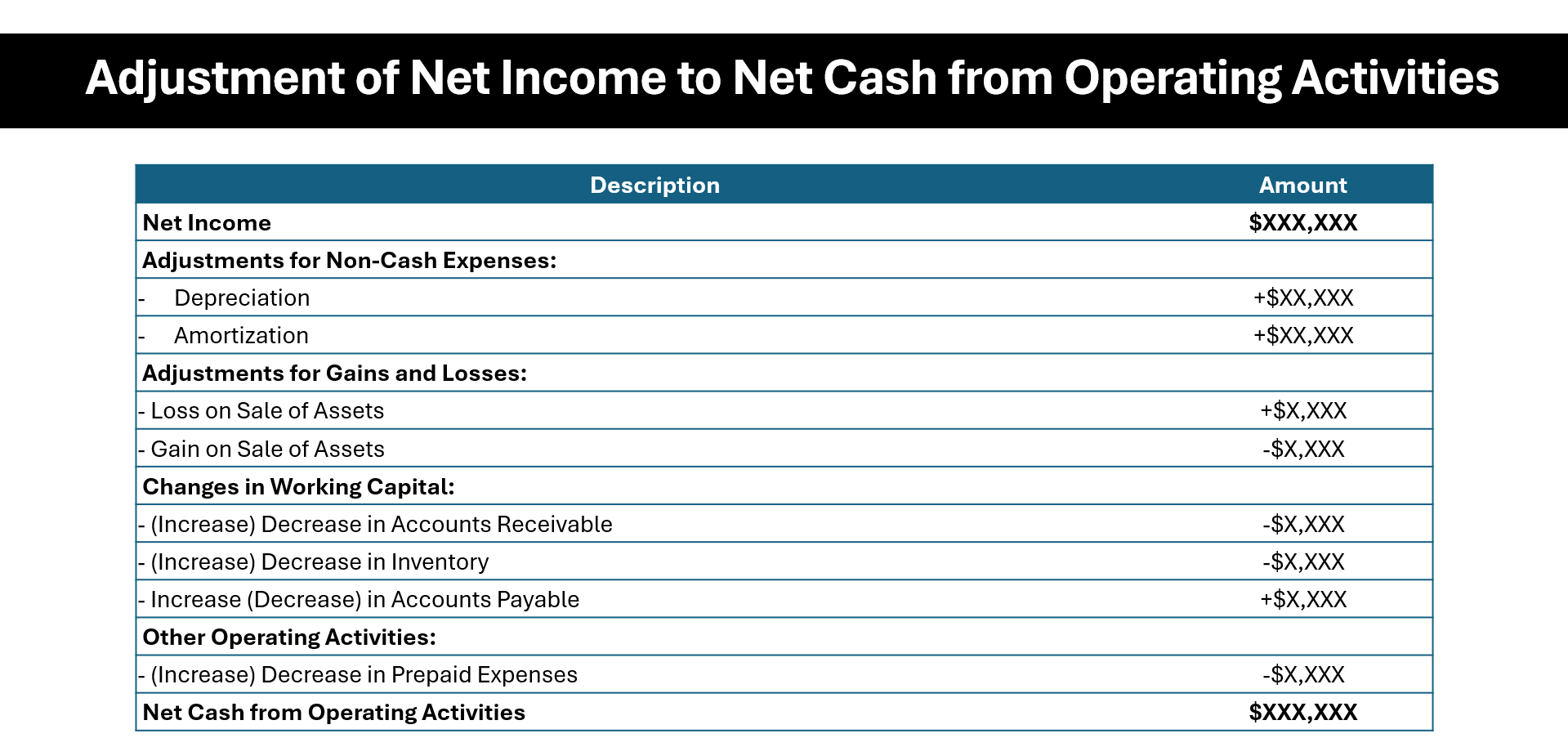

- Preparing a cash flow statement via the indirect method begins with the company’s net income and then makes adjustments for non-cash transactions, such as depreciation and amortization. It also requires adjustments for changes in working capital, including both current assets and current liabilities. For example, an increase in accounts receivable would be subtracted from net income because it represents sales that haven’t yet resulted in actual cash inflow. Conversely, an increase in accounts payable would be added back since it signifies expenses that have not consumed cash yet.

- Understanding and applying the indirect method involves interpreting the impacts of various transactions on net income correctly. For instance, gains and losses that do not involve cash, such as those on the sale of long-term assets, require adjustments to reconcile the net income to the net cash provided by operating activities. These adjustments ensure the cash flow statement reflects the actual liquidity movement rather than just accrual-based accounting figures, providing a clearer picture of the business’s financial health and cash-generating ability.

Direct vs. Indirect Method: A Brief Overview

When it’s time to communicate your company’s cash flow, you can traverse one of two paths: the direct or indirect method. Both ultimately illustrate the same end figure, but they differ significantly in approach. The direct method lists all cash receipts and payments, including cash paid to suppliers, cash receipts from customers, and cash paid in wages. It might be more intuitive as it resembles your checkbook register, which aligns closely with the financing sections operating values of cash inflows and outflows.

On the flip side, the indirect method is like solving a mystery by following the clues backwards. It starts with net income and adjusts for all non-cash transactions and changes in working capital, offering a clear view of cash flows from operating activities. This method might involve less digging into transactional details since it deftly makes use of the income statement and balance sheet data already at your fingertips, reflecting the substance over form principle inherent in disclosing financing transactions.

In the preparation of the investing and financing sections of the statement of cash flows, whether one uses the direct or indirect method, the presentation of cash flows from financing activities, which typically involves analyzing the cash proceeds from issuance of debt or equity, remains the same. This delineation underscores the flexibility entities have in representing cash flows while adhering to accurate disclosure of financing cash flows.

Core Components of the Indirect Method

Starting with Net Income

The journey to creating a cash flow statement using the indirect method begins with net income, the protagonist of your financial narrative. Net income is your business’s earnings after all expenses—including taxes, interest, and operating costs—have been settled. It’s your starting line, with the statement unfolding as you adjust this figure to reflect the true cash position. For a comprehensive understanding of your company’s financial health, it is crucial to integrate income statement depreciation adjustments to accurately illustrate the business’s cash flow. In essence, business accounting doesn’t merely end with net income; it includes the thorough application of basis accounting principles as prescribed by both GAAP and IFRS frameworks.

For an instance, if your business’s income statement displays a net income of $10,000 for the quarter, that’s the figure you’re kicking off with on your cash flow statement. Yet, that number doesn’t tell the whole cash story, so you dig deeper with adjustments for a complete cash flow portrait.

Adjustments for Non-Cash Transactions

Adjustments for non-cash transactions are the detectives transforming net income into actual cash flow. These adjustments are like a cornerstone in financial documentation, ensuring that your company’s liquidity is not misrepresented due to accounting entries that do not immediately affect cash reserves. Advisors often stress the importance of such adjustments, as they’re vital because many accounting entries don’t involve immediate cash movement. Depreciation and amortization are classic examples where they allocate the cost of an asset over its lifespan without cash changing hands each year.

Here, you’re adding back expenses that didn’t decrease cash or deducting revenues that didn’t increase cash. This could include stock-based compensation and gains or losses from asset sales. An astute review of your income statement and balance sheet, often guided by professional advisors, will help you decode these non-cash clues to reveal a more precise cash flow from operating activities.

For example, if you reported $5,000 in depreciation, you’d add that back because it didn’t actually drain your cash reserves. Similarly, if your stock-based compensation totaled $2,000, that value is adjusted since no cash left your coffers. These adjustments ensure your cash flow statement reflects the reality of your cash situation.

A Step-by-Step Guide to the Indirect Method

Listing Operating Activities and Adjustments

To lift the veil on your cash flow from operating activities, grab your ledger and scrutinize it for cash-ins and cash-outs related to daily business operations. The indirect method requires you to adjust your net income by adding or subtracting changes in your working capital accounts. This includes accounts receivable, inventory, and accounts payable, among others.

If you find that your accounts receivable have decreased, that means cash has flowed into your business, and you’ll add this amount to your net income. Conversely, an increase in inventory means you’ve used cash, so this gets subtracted. The art of listing operating activities and adjustments is like putting together a puzzle where each piece represents the ebb and flow of cash through your business operations.

Imagine your company had a decrease in accounts payable. This would indicate that you’ve paid off some of your debts, leading to a cash outflow: a detail that must be subtracted from your net income. All these adjustments culminate to form the “net cash from operating activities,” providing a clear picture of cash generated or used in the everyday running of your business.

Accounting for Investing and Financing Activities

The spotlight now shifts to the part of your cash flow statement where you showcase the cash used in or provided by investing and financing activities. Investing activities encapsulate the money spent or received from the sale and purchase of long-term assets, like property, plants, and equipment—critical moves that involve buying significant assets. Any decrease that has taken place in current assets, such as a decrease in accounts receivables, or acquisition of new assets, would appear in this section. If your company purchased new machinery, the cash paid would be a cash outflow in this section.

Financing activities, meanwhile, offer a window into how cash is exchanged between your company and its creditors and investors. This is where you’d see transactions dealing with the equity section of your organization. Issuing debt through bonds or notes can lead to a cash inflow, registering in this section. For example, if your company benefitted from a debt transaction due to the issuance of new bonds, the cash inflow from the bonds is recorded here. Conversely, debt repayment, including the principal amount of a note, represents a cash outflow. Similarly, equity transactions such as stock issuance, indicate an influx of capital from investing parties, and therefore, would also be listed as an inflow here.

By netting each section to reflect inflow less outflow, you determine the net cash provided by or used in investing and financing. This, along with the net cash from operating activities—reflecting operations-driven adjustments like decreases in receivables and other operation-related movements—gives you the final piece in the cash flow puzzle, revealing the net increase or decrease in cash for the period. This net figure is then reconciled with the opening cash balance to arrive at the closing cash balance for the period.

Practical Illustration: An Example Statement

Company XYZ’s Cash Flow Walkthrough

Let’s journey through the cash flow statement of a fictional business, Company XYZ, to see the indirect method in action. With an opening cash balance listed as $10.7 billion, Company XYZ embarked on the financial year with a healthy cash reserve. Over the reporting period, they engaged robustly in their operations, which generated a substantial $53.7 billion in cash.

Delving into the investing activities, the ledger reveals a hefty $33.8 billion used in various investments—perhaps sprouting new seeds for future growth. The financing activities section offers another intriguing chapter, with $16.3 billion directed towards rearranging the company’s debt and equity financing structure.

After all the adjustments and netting off figures in each section, Company XYZ closed the reporting period with a victory lap—a $3.5 billion increase in cash and cash equivalents. Thus, the curtain falls on the financial year with the final balance of cash and cash equivalents fluttering at $14.3 billion, painting a dynamic picture of Company XYZ’s financial maneuvers throughout the period.

Translating Net Income into Operating Cash Flow

For Company XYZ, the alchemy of converting net income into operating cash flow is an intriguing process. Starting with a net income figure, which is the business’s reported profit, adjustments are meticulously added or deducted to reflect the actual cash movement. Intangible wear and tear on assets—depreciation—is one non-cash expense that’s added back, as no cash has actually been spent.

Receipts trickling in late add another layer to the tale if accounts receivable have decreased, showing that customers have settled their dues in actual cash. A dive into the inventory levels reveals yet another subplot; if there’s an increase, cash has gone out to stock up on materials or goods, signifying a deduction. On the other side of the equation, if there’s a climb in accounts payable, it signals that bills are yet unpaid, conserving cash, so this gets added to the net income.

By the end of this transformative calculation, Company XYZ arrives at its operating cash flow—a number often seen as a more robust measure of financial health than net income, as it captures the actual cash generation capacity of the company’s core business operations.

Why Opt for the Indirect Method?

Simplifying Reporting for Larger Organizations

Large organizations often juggle complex financials and numerous transactions, making the indirect method a boon for simplifying reporting. It leans on the familiarity of income statements and balance sheets, which are already part of the accounting routine in these big entities. This means less additional work since the data needed is already prepared—no need for the meticulous tracking of each cash transaction as in the direct method.

For a behemoth of a company, the ability to streamline financial reporting processes cannot be overstated. It allows them to present a complex cash flow narrative in an accessible, understandable format. With the indirect method, they can paint a comprehensive picture of their financial health without getting swamped by the granular data that would otherwise overwhelm the uninitiated.

Reconciling Accrual Accounting with Cash Reality

The indirect method excels at reconciling the sometimes-disparate worlds of accrual accounting and actual cash. While accrual accounting recognizes revenues and expenses when they are incurred, regardless of cash movement, the indirect method meticulously adjusts for these transactions to reveal the cash reality. This reconciliation is like a financial reality check, providing stakeholders with insight into the actual cash available.

By converting accrual-based net income to cash-based profit, businesses can offer a clear window into their cash operations, ensuring stakeholders aren’t misled by numbers that look good on paper but don’t reflect the company’s immediate fiscal health. It’s a process that not only clarifies the present but also helps predict and manage future cash flows.

The Benefits of Mastering the Indirect Cash Flow Method

Informed Decision-Making through Financial Analysis

By mastering the indirect method, you earn a deeper understanding of your business’s cash activities, which is golden for informed decision-making. It’s like having a financial compass—this method paints a clearer picture of how operations, investing, and financing activities impact your cash position. Better yet, it helps you comprehend the story behind the numbers, such as the implications of increasing accounts receivable or the long-term investments being made.

Armed with knowledge of the cash flow intricacies, you can analyze trends, evaluate the efficiency of your operations, and make strategic decisions with confidence. Whether you’re considering expansion plans, assessing the ability to service debts, or just trying to improve cash management, understanding the cash flow dynamics is critical to steering your business towards success.

Strategic Planning and Financial Management

Being fluent in the indirect method equips you with a strategic lens for your financial planning and management efforts. It’s akin to having a financial roadmap, guiding you through the terrain of projected earnings and expenditures. This method offers visibility into how cash is moving in and out, allowing you to pinpoint areas that may need tightening up or, conversely, present opportunities for investment.

Financial management becomes more astute when you’re armed with a comprehensive understanding of your cash flow. It ensures that you’re not flying blind but rather, making strategic decisions based on a realistic cash position. Whether you’re safeguarding liquidity, setting budget priorities, or evaluating the impact of potential changes, mastering the indirect method is an ally in navigating your business toward a prosperous future.

Frequently Asked Questions (FAQ)

What Are the Main Advantages of Using the Indirect Method?

The indirect method boasts practicality and efficiency, making it a hit among finance professionals. Its key advantages include using already available financial statement data, reducing the need to track down additional information. Plus, it’s superb for consistency and comparability across companies, greatly beneficial for benchmarking and financial analysis.

Why is the indirect method preferred in financial reporting?

The indirect method is preferred in financial reporting largely due to its seamless integration with accrual accounting and the ease with which it allows larger companies to report complex transactions. It’s accustomed to financial professionals and aligns with established reporting systems, enabling consistent and comparative analysis across various businesses.

How Can One Move from Accrual Accounting Figures to Cash Flow?

To move from accrual accounting figures to cash flow, you start with the net income and adjust for all non-cash transactions—like depreciation and changes in working capital. This includes recalculating income and expenses reported on an accrual basis to reflect when the actual cash is received or spent, ensuring an accurate cash flow figure.

Why do we add back depreciation and amortization expenses?

We add back depreciation and amortization expenses because they are non-cash charges to income. They account for the gradual wear and tear of assets over time, not actual cash spent. Adding these expenses back to net income adjusts for the fact that they reduce reported earnings, but do not impact cash reserves.

What is the difference between the indirect and direct cash flow methods?

The indirect cash flow method adjusts net income for non-cash transactions and changes in working capital to determine cash flow, while the direct method tallies up all actual cash transactions, like cash received from customers and cash paid to suppliers. The indirect method is less time-consuming to compile but less detailed compared to the direct method, which provides a granular breakdown of cash inflow and outflow.