Compound Interest Uncovered

Unearthing compound interest uncovers a remarkable secret weapon in the arsenal of savvy earners and savers. It’s where your money starts to work harder, earning interest not only on the original amount you’ve set aside but also on the interest that accumulates over time. It’s a case of earning “interest on interest”, and it can lead to significant growth of your wealth, transforming your financial situation dramatically when hained over the long term.

KEY TAKEAWAYS

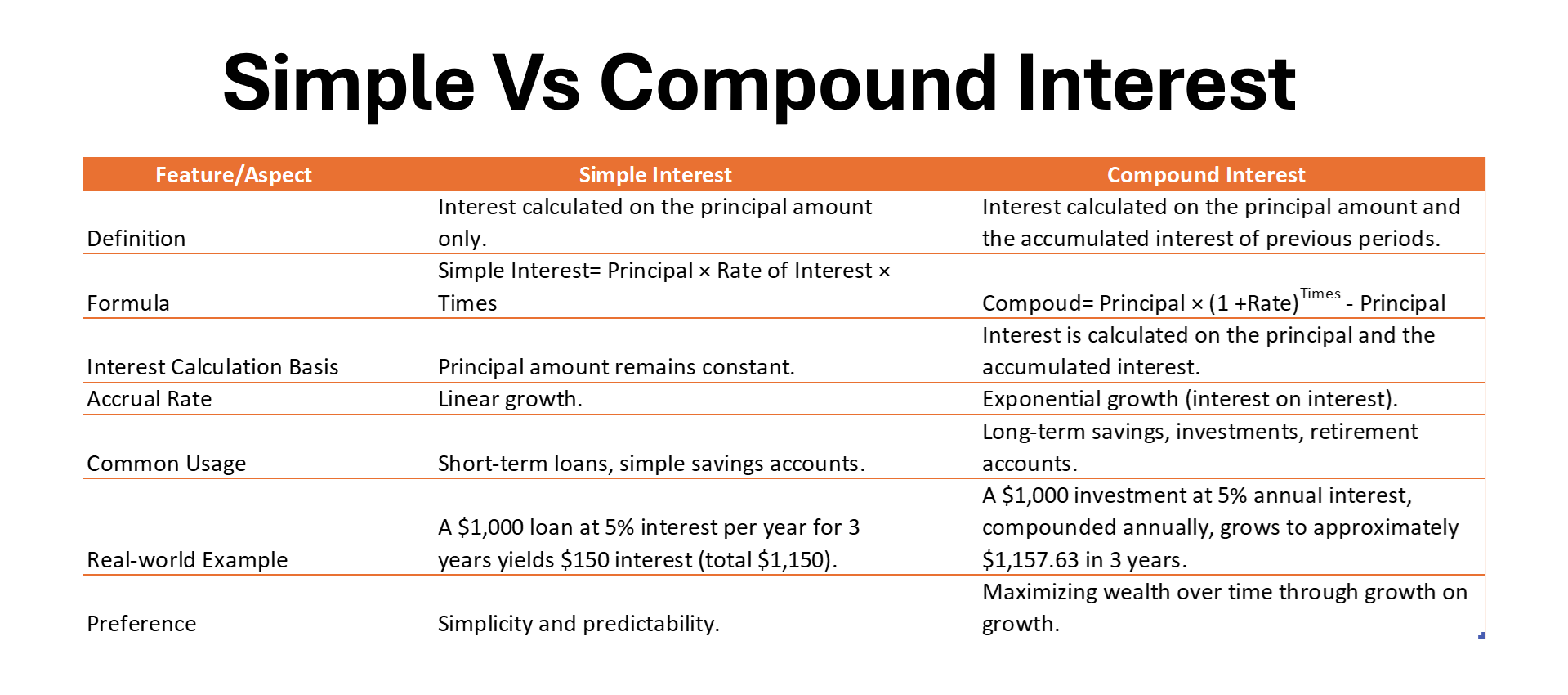

- Compound interest allows for potentially higher earnings than simple interest because it involves earning interest on both the principal and the previously accumulated interest. This can lead to exponential growth over time, making it beneficial for long-term savings and investments.

- Simple interest is calculated only on the principal amount, which means the interest earned does not compound. This can be advantageous for borrowers as it results in lower total interest payments over the life of a loan than if the interest were compounding.

- The frequency of interest compounding can significantly impact the total amount of interest earned or paid. The more often the interest compounds, the greater the potential for growth. Savers and investors should seek out accounts that offer frequent compounding to maximize earnings, while borrowers should look for loans with less frequent or no compounding to minimize costs.

Understanding the Basics of Simple Interest

What is Simple Interest?

Simple interest is essentially the fee you either earn or pay for the use of money. It’s determined by multiplying the principal amount – that’s the original chunk of cash in question – by the interest rate and by the time for which it’s invested or borrowed. With simple answer, they don’t factor in any interest that’s piled up previously; it’s always about the base amount.

Whether you’re stashing away funds in a savings vehicle that pays you simple interest or you’re taking out a loan that charges it, the calculations are refreshingly linear. The deal is clear-cut: the interest you’ll deal with will be predictable and unchanged over time.

Calculating Your Simple Interest Potential

Calculating your simple interest potential is like baking a basic three-ingredient recipe. Calculating your simple interest potential is like baking a basic three-ingredient recipe. You’ve already got your amounts: the principal (how much dough you’re starting with), the rate (essentially the recipe for how much extra dough you’ll earn each year), and the time (how long you’re letting that dough rise). Mix them together, and voilà, you’ve got your interest. To fine-tune this baking process, consider using a savings account interest calculator for a precise outcome.

Here’s what to do: take your starting sum (the principal), multiply it by the annual interest rate (as a decimal), then multiply that by the number of years you’re considering. This multiplication marathon gives you the total interest you can expect to pocket (or pay, if it’s a loan), separate from the original amount. It’s that simple.

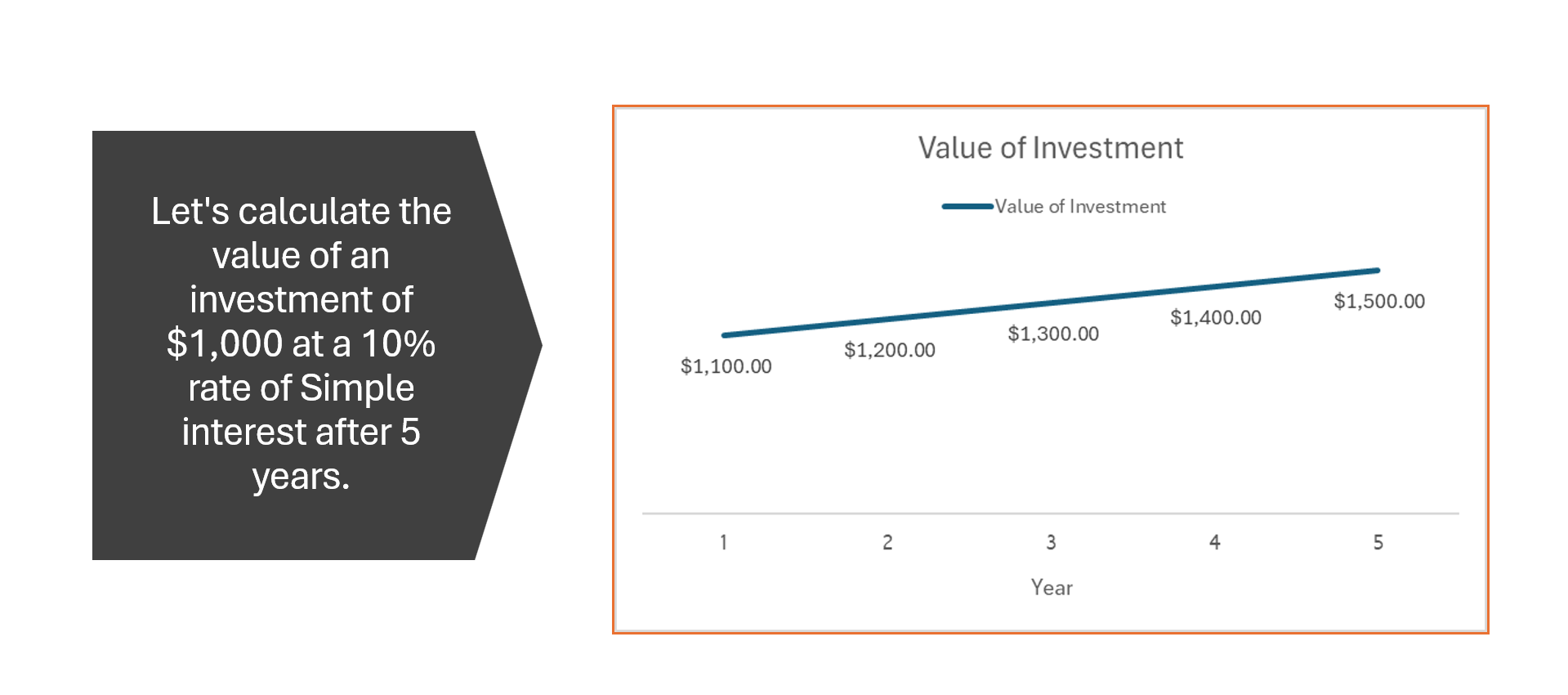

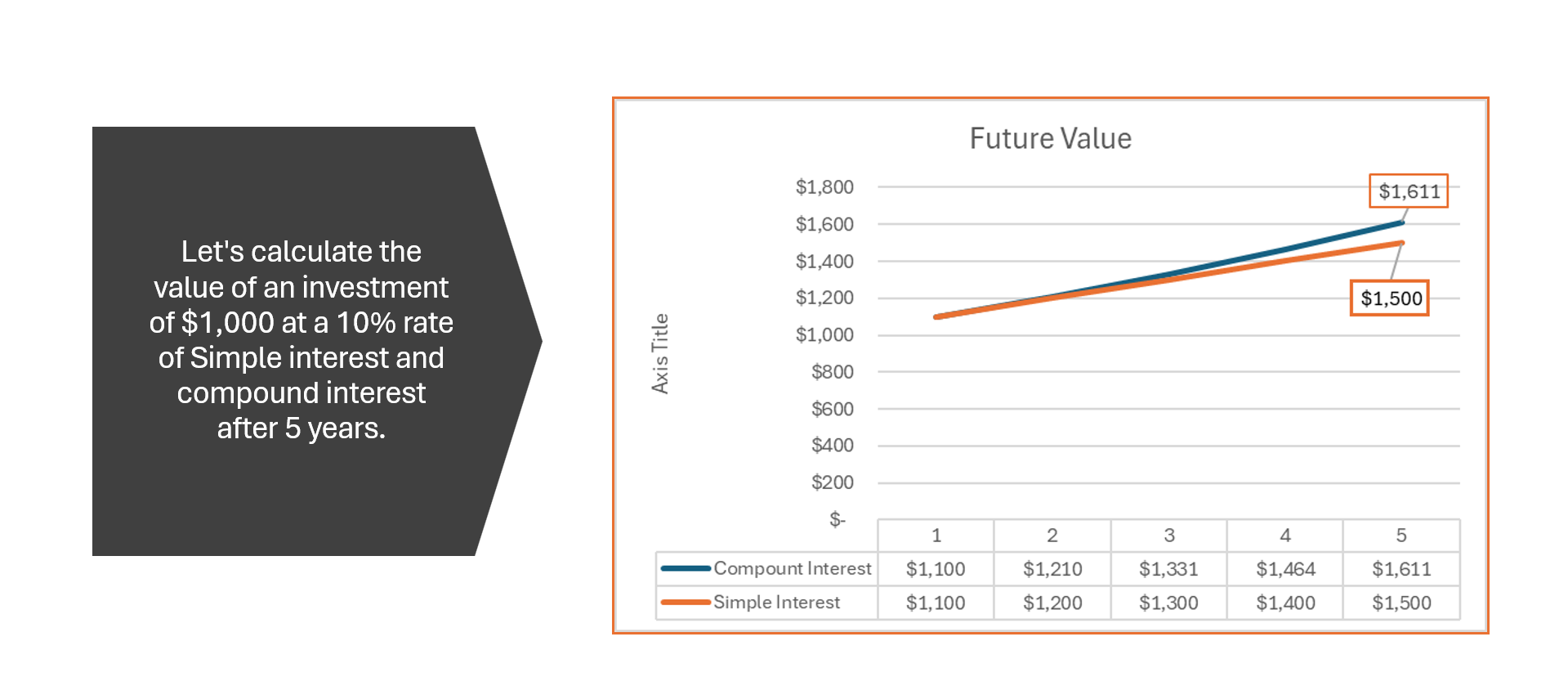

So, let’s say you’ve stashed away $1,000 (your principal) in a savings account with a 3% annual interest rate for 5 years. Plug those numbers into the simple interest formula, or input them into a savings account interest calculator: $1,000 (principal) x 0.03 (rate) x 5 (time) equals $150 in total interest earned.

Unlocking the Potential with Compound Interest

The Basics of Compound Interest

Diving into the essentials of compound interest, imagine it as an ever-growing snowball effect on your money. As your savings reach maturity, not unlike fine wine, the increase in their value becomes evident. Unlike simple interest, compound interest recalculates your earnings periodically by including both the initial principal and the accumulated interest from past periods. It’s a double scoop of financial growth – you earn interest on the money you’ve banked, plus interest on the interest that’s already been paid to you. When building a financial portfolio, understanding this principle could be vital in maximizing your earnings.

Here’s the formula that spells out how the magic happens: Compound Interest = P(1 + r/n)^(nt). That might look like a secret needle in a haystack, but once broken down, it’s quite understandable. P stands for the principal amount, r is the annual interest rate, and n represents how frequently the interest is compounded—be it daily, monthly, quarterly, or yearly. The t is the amount of time in years that the money is invested. Using a CD account as an example of a financial tool in your portfolio, the compounding frequency might be less flexible, yet the maturity date ensures you benefit from a higher interest rate over time.

How Compound Interest Accelerates Your Earnings

Compound interest rapidly speeds up your earnings by putting your accumulated interest back to work. Think of it like a snowball rolling downhill, growing bigger with every revolution. This means each round of interest is calculated on a progressively larger base — your initial investment plus the accumulated delivery of interest from previous periods. Embracing compound interest is a key takeaway for anyone focused on retirement savings, as it can significantly boost your nest egg over time.

Consider the magic of compounding annually. If you sock away that $100 at a 5% interest rate in a tax-advantaged account, the first year nets you $5, making the new balance $105. The following year, you’re not just earning interest on the $100 but on the entire $105. The result? An interest payment of $5.25, slightly more than the year before. As years roll on, that amount continues to compound, pushing the growth of your investment at an increasingly brisk pace.

Your earning potential accelerates with this process, and when given enough time, it can turn even modest savings into a sizeable nest egg, proving to be incredibly powerful for long-term financial goals. Meanwhile, most other debts like mortgages, student loans, and auto loans typically charge simple interest, which does not benefit from this effect.

Side-by-Side: Comparing Simple and Compound Interest

When Simple Interest May Be Advantageous

Simple interest may take the financial crown in scenarios where predictability and straightforward management are top priorities. For instance, if you’re borrowing with a tight budget, simple interest spells out exactly what you’ll owe over time, with no surprises, hence its alignment with the values of accuracy and completeness. It’s ideal for short-term loans, where you’re planning to pay the principal down quickly, ensuring interest payments don’t escalate.

Moreover, those who prefer a fixed return on their investment, such as a certificate of deposit at a bank, might favor the immutability of simple interest. They can enjoy the certainty of knowing the exact amount their money will earn during the investment period, a comforting assurance for those cautious about market fluctuations or complicated interest strategies, all while upholding the importance of accuracy in their financial planning.

Scenarios Where Compound Interest Wins

In the game of long-term wealth accumulation, compound interest often steals the show. If you’re an investor aiming to grow your nest egg, compound interest is your powerhouse, especially if you start early. Let’s consider a compound interest savings example: if you have a $10,000 deposit in a savings account with a 4% annual compound interest rate, by the end of the first year, you’d have $10,400 without lifting a finger, and that amount would keep growing year over year due to compounding interest rates. Allowing your investments to sit undisturbed for years or even decades gives you the full advantage of the compound effect, dramatically increasing your returns compared to simple interest.

Retirement accounts like 401(k)s and IRAs are prime examples where compounding interest is king. The longer your time horizon, the more dramatic the benefits, as your earnings are reinvested to generate their own earnings. Additionally, compound interest can be a winner for debt instruments like high-yield savings accounts and bonds, where the goal is to augment your principal at a rate that outpaces inflation, thereby growing your real purchasing power over time.

Practical Examples and Real-World Impacts

To grasp the tangible impacts of simple and compound interest, consider their real-world applications:

To grasp the tangible impacts of simple and compound interest, consider their real-world applications:

Imagine you’re investing $10,000. With simple interest at a rate of 4% over 10 years, your investment would net you $4,000 in interest, making your total stash $14,000. Clean and uncomplicated.

Now, take that same $10,000 but put it into an account that compounds annually at the same rate. After a decade, you won’t just have an extra $4,000. Thanks to compound interest, you’d have about $14,802.44, an additional $802.44 earned from interest on your interest. This is not just theoretical maturation of funds; it’s a practical testament to the power of allowing your money to grow over time for future benefit, a core matter of personal finance.

Switching gears, let’s talk loans. Some lenders can even use your loan to pay them directly on your behalf, ensuring you do not default on essential payments. However, a car loan with simple interest remains straightforward – the amount you pay in interest is consistent, based on the original loan amount. But a credit card often uses compound interest, where carrying a balance means you’re charged interest on top of interest. This can quickly inflate the amount you owe, underlining the critical need to understand these concepts before borrowing.

Both simple and compound interest can significantly affect your financial health, whether you’re saving for the future or borrowing for the present. Understanding the difference can help you choose the right bank accounts, investments, and loan types to meet your financial goals—and that’s true: Not only are your deposits (up to $250,000) FDIC-insured , but you’re also less likely to spend the funds you set aside in a savings account. (Disclaimer: FDIC insurance does not cover investments or loans.)

Tips for Making the Most of Your Interest-Earning Strategy

To really stretch your dollars and make them sweat for you, let’s walk through some tips to jazz up your interest-earning strategy:

- Shop Around: Don’t settle for the first interest rate you stumble upon. Explore different financial institutions to find the highest Annual Percentage Yield (APY) for savings accounts or Certificates of Deposit (CDs).

- Start ASAP: With compound interest, time is a precious ally. Even small amounts can balloon over years, so kick off your saving habit early and stick to it.

- Regular Contributions: Consistently adding to your savings amplifies the compounding effect. Set up automatic transfers to ensure you’re always feeding your savings.

- Reinvest Dividends: If your investments pay dividends, reinvesting them ramps up the compound interest, as you’ll earn returns on a progressively larger principal.

- Limit Withdrawals: Keep your paws off your savings and let the interest compound. Frequent withdrawals disrupt the compounding process, clipping your money’s wings.

By leveraging these strategies, you’re not just saving money; you’re actively cultivating it, making it grow through the magic of compounding interest. With a little time and discipline, your financial future can blossom into something substantial and sustaining.

Key Factors Influencing Interest Calculations

When it comes to figuring out how your interest calculations stack up, there are a few key ingredients you need to factor in:

- Interest Rate: This is the biggie — it’s the percentage that dictates how much interest you’ll earn on investments or owe on loans. A higher rate means more money earned or paid.

- Principal Amount: The starting line for your interest calculations is the principal, which is the original sum of money invested or borrowed.

- Compounding Frequency: How often interest is compounded can supercharge your earnings. The more frequently interest is compounded, the more you earn.

- Time: Time is money, quite literally, in the world of interest calculations. More time means more compounding periods, which means more interest earned.

- Tax Implications: Don’t forget Uncle Sam. Taxes can take a bite out of your interest earnings unless they’re protected in a tax-advantaged account.

Understanding each factor’s role can help you navigate the choppy waters of finance more effectively. Keep them in mind when planning your savings strategy or contemplating a loan, and they can guide you towards smarter, more informed decisions.

FAQs: Demystifying Interest Rates and Maximizing Returns

Which is better for long-term growth, simple or compound interest?

For long-term growth, compound interest typically outshadows simple interest. By reinvesting your earnings, you benefit from the “interest on interest” effect, resulting in a larger balance over an extended period. This exponential growth significantly boosts your investment’s value when compared to the linear growth offered by simple for the same interest rate and time period.

Can I switch between simple and compound interest on my accounts?

Generally, the type of interest your account earns is not switchable. It’s determined by the terms set by your financial institution or lender. However, you might find some investment products offering a choice, so it’s always worth asking your provider if alternatives are available.

How often do financial institutions compound interest?

Financial institutions can compound interest at various intervals such as daily, monthly, quarterly, or annually. The frequency can greatly affect how much interest you accumulate over time, with more frequent compounding leading to more substantial growth of your investment or savings. Always check the compounding schedule when opening an account to understand its potential growth.

What about the interest you pay when you borrow money to buy a house or a car?

When you borrow money to buy a house or a car, you’re often dealing with compound interest, particularly for a mortgage. Early on, a larger portion of your payment goes towards interest rather than the principal. Over time, as you pay down the balance, more of your payment is allocated to the principal, reducing the amount of interest that compounds. Car loans, however, may use simple interest. It’s crucial to understand your loan’s terms before committing.