In an inventory-centric world, nearly half of the small businesses are grappling with effective inventory management. That’s where you get ahead — by ensuring you’ve got a handle on your ending inventory, you’re positioning your business for better profitability and efficiency. Imagine having just the right stock levels to meet customer demands while sidestepping costly overages!

So, keep in mind that ending inventory isn’t just a figure to be reported; it’s the bedrock on which the sturdiest business plans are built. By pinpointing this value, you can forecast futures better than a seasoned oracle, blending past data with present insights for a winning strategy.

KEY TAKEAWAYS

- The Ending Inventory Formula is critical for efficient inventory management as it helps businesses determine the value of unsold goods at the end of an accounting period, which in turn influences balance sheet accuracy, reporting consistency, and planning for future inventory needs.

- Accurate calculation of ending inventory allows businesses to optimize operations, prevent overstocking or understocking, maximize profits, and fulfill customer demand more effectively, by informing decisions on when and how much inventory to reorder.

- Besides mainstream inventory systems, the use of the Ending Inventory Formula is essential for informed decision-making, contributing to cost savings by indicating optimal replenishment times, identifying the most profitable items, and guiding strategic stocking and promotional activities.

Demystifying the Ending Inventory Formula

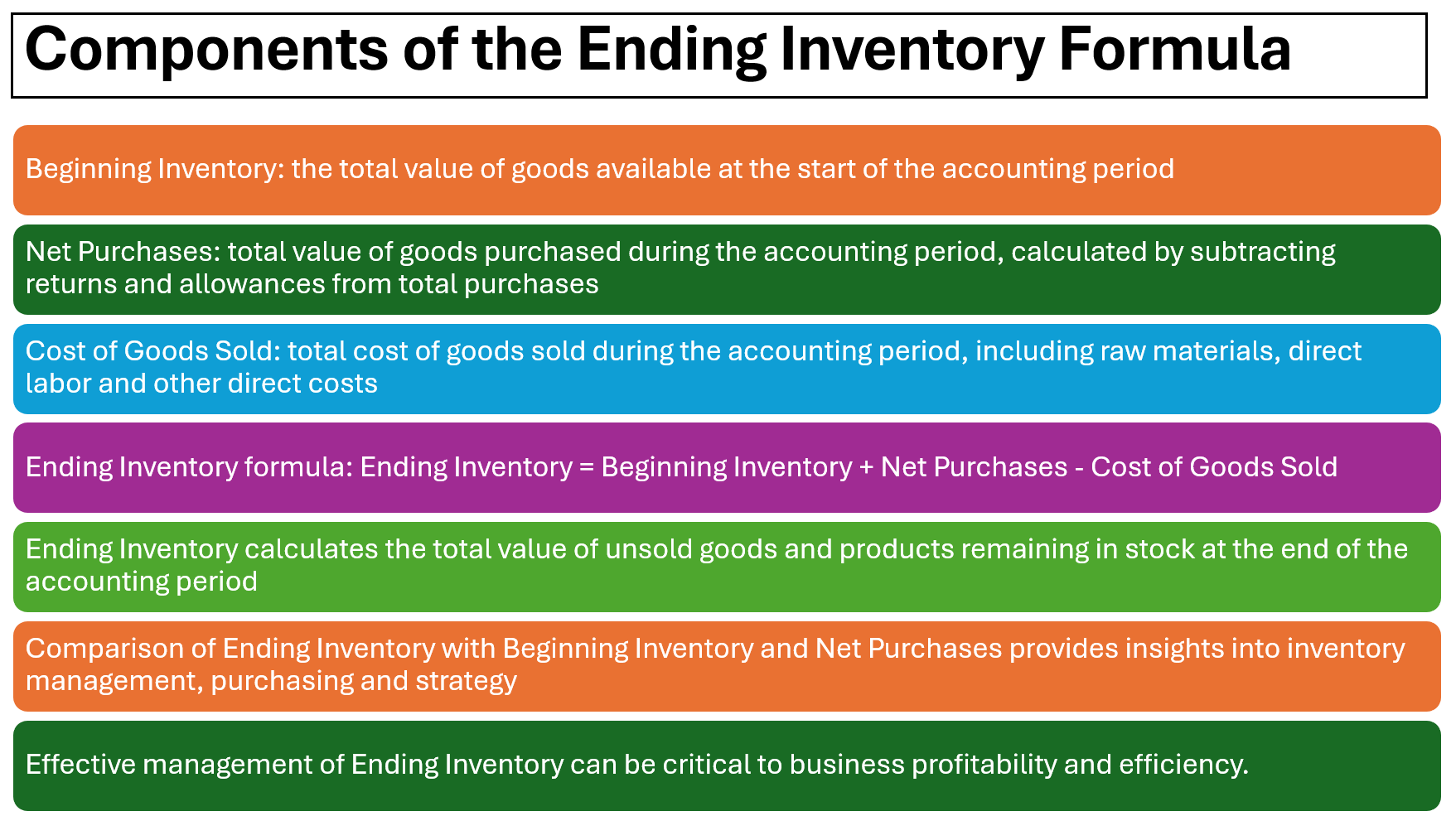

If the idea of diving into the ending inventory formula has you feeling more dread than excitement, you’re not alone. But fear not! This formula is a key ally in your business arsenal. It’s essentially a math equation that tells you the value of the unsold goods chillin’ in your inventory when your fiscal period wraps up. Here’s the classic formula that accountants and business moguls alike have come to know and love:

Ending Inventory = Beginning Inventory + Purchases - Cost of Goods Sold (COGS)

Breaking it down, you’ve got your beginning inventory (what you started with), your purchases (the fresh goods you’ve bought during the period), and the cost of goods sold (what you’ve waved goodbye to as customers snapped them up). Subtract the COGS from the sum of your beginning inventory and purchases, and voilà — you’ve got your ending inventory!

Understanding the ending inventory or closing stock helps you avoid those “oops” moments that can sting your wallet — like ordering too many widgets because you thought you had fewer. It’s a balancing act, and the ending inventory formula gives you the numbers to juggle with confidence. So, equip yourself with it and turn inventory management into less of a guessing game and more of a strategic play.

The Pillars of Inventory Calculations

Understanding FIFO, LIFO, and Weighted Average Methods

When it comes to managing your inventory, there are a few staple methods that are like the secret sauce to a perfect financial stew. These methods – FIFO, LIFO, and Weighted Average – each have a unique flavor and can significantly influence your financial statements.

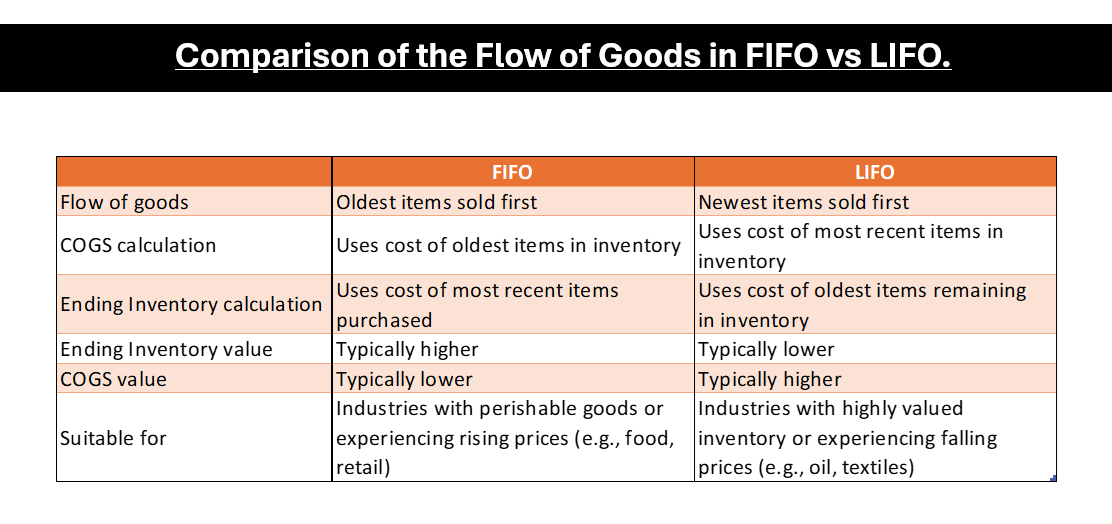

Imagine you own a boutique that sells the trendiest clothes. If you adopt the FIFO method, the first shirts you stocked will be the first ones sold. This approach mirrors natural consumption patterns and can really align with how goods move in perishable industries or those with products susceptible to obsolescence. Plus, in a period of rising prices, this method can give your profits a sweet little lift on paper since the older, cheaper goods are the ones ‘sold’ first.

On the flip side, if you’re feeling the pinch of inflation and costs are climbing, LIFO might be your ally. By accounting for the most recently acquired (and likely more expensive) items as sold first, you report lower profits – and that can mean paying less in taxes (a silver lining in tough times, perhaps?).

Lastly, if you’re a fan of the middle ground, the Weighted Average method smoothens out the extremes by calculating an average cost for items sold during the period. It’s like the porridge that Goldilocks chose – not too hot, not too cold, but just right, especially if your inventory items are pretty much identical.

Each of these Accounting methods comes with its strategic benefits, and whichever you pick can have ramifications for your financial reporting, taxes, and even your business operation strategies. So choose wisely to ensure your inventory tells the best story for your business context.

FIFO: First-In, First-Out Explained

Let’s get cozy with FIFO, shall we? FIFO, or First-In, First-Out, is like keeping a strict queue at a movie premiere. Items that shimmy into your inventory first are the ones hitting the sales floor first. It’s the go-to move for businesses that deal with perishables like fruits, medicines, or fashion trends that come and go faster than a TikTok dance.

So why is FIFO a crowd favorite? If your product prices are on a rollercoaster ride, FIFO tends to inflate your ending inventory value. That’s because you’re selling off the old stock at historic costs and keeping the shiny, newer inventory on the books. Think of it as having unsold units valued at current, possibly higher, prices, giving stakeholders the thumbs up regarding the state of your inventory.

Here’s a miniature breakdown of FIFO:

- Aligns with the actual flow: FIFO mirrors the natural flow of inventory for many businesses – send the old stuff out first!

- Reduced waste: By getting those early birds out the door, you’re less likely to end up with expired or outdated products.

- Higher net income during inflation: When costs are on the uptick, FIFO makes your COGS more conservative and your net income gets a bump.

- Current Stock Valuation: It’s akin to keeping your finger on the pulse of the market, as your ending stock reflects the most recent prices.

However, there are a couple of headaches to watch out for:

- Tax Burden: With higher profits, come higher taxes. That’s just the way the cookie crumbles.

- Mismatch: Real life isn’t always as orderly as FIFO assumes – sometimes, items don’t sell exactly in the order they arrive.

Best for: Businesses with items that can spoil, become obsolete, or those seeking to show a stronger balance sheet during times of rising prices. If that’s you, FIFO might be your inventory soulmate.

LIFO: Last-In, First-Out Unpacked

Diving into LIFO, or Last-In, First-Out, imagine you’re stacking cans of paint for an art supply store. The freshest, most vibrant cans you just received sit atop the older ones. When it’s time to restock the shelves, you grab from the top — the latest arrivals are the first to bid farewell. That’s LIFO in a nutshell: the newest products you bring into your inventory are the first to ship out.

During inflationary times, when your latest cans of paint cost more than the ones gathering dust, LIFO can be a savvy choice. By expensing those pricier cans first, your cost of goods sold (COGS) gets a bump, while your net income takes a dip — potentially trimming down your tax bill since you’re taxed on profits.

Here’s a more granular peek at the charm of LIFO:

- Tax Advantage: Who doesn’t love a bit of tax relief? In times of rising prices, LIFO can be a boon for your tax bill.

- Cash Flow Boost: With taxes potentially lower, you might have more cash on hand to reinvest into your business.

- Inflation Edge: By matching current costs with revenues, you paint a more realistic picture of your profitability.

Still, every rose has its thorns:

- Outdated Stock Valuation: Your ending inventory might be undervalued, reflecting those old purchase prices.

- Complexity: A bit of a headache for your accounting team, especially if you’ve got an inventory that varies a lot in cost.

- Regulatory Restrictions: Notably, LIFO is not allowed everywhere; some accounting standards outside the US give it a no-go.

Best for: Businesses with non-perishable goods and those operating in sectors with steep and steady price hikes. If strategically managing your tax liabilities and cash flow sounds attractive and you’re not locked into First-In, First-Out by regulatory constraints, consider keeping LIFO in your treasure chest of inventory tactics.

The Mechanics of Weighted Average Cost Method

Imagine all your inventory items cozied up and mingling together at a grand ball. They share and blend their costs so that every item has the same value — this is the essence of the Weighted Average Cost Method. It plays the role of a great equalizer, smoothing over cost fluctuations by taking a broad average.

This method calculates the average cost of your inventory by dividing the total cost of goods available for sale by the total number of units available. It’s like making a giant batch of cookie dough where all your ingredients are averaged into a consistent mixture. As new inventory waltzes in at different costs, the average gets recalculated, keeping the pricing dance in perfect rhythm.

Here’s why you might love it:

- Simplicity: It’s straightforward, making it easy to manage and understand.

- Stable Pricing: It smooths out the highs and lows in your cost records, which can be especially handy if prices swing faster than a jazz band’s tempo.

- Adaptability: Ideal for businesses with large quantities of similar items where individual tracking might earn you a headache rather than profits.

But it’s not all sunshine and rainbows:

- Less Tax Flexibility: Unlike LIFO, it doesn’t offer that tax-shaving edge during times of inflation.

- Potentially Misleading: In certain scenarios, the average cost might not reflect the true cost of recent purchases, obscuring actual cost trends.

Best for: Companies with homogenous inventory (think bolts of fabric or nails) or those looking to steer clear of the complexity that comes with FIFO and LIFO. If you want a middle-of-the-road method that gives you a solid, reliable average to work with, the Weighted Average Cost Method should be right up your alley.

Calculating Ending Inventory Step-by-Step

Traversing Through the Calculation Process

Calculating ending inventory is a bit like piecing together a puzzle — you need the right pieces in the right places and a little bit of patience. To traverse this landscape, start with the basics: count what you have. This means a physical inventory count, which can either be a fun treasure hunt or a long-haul mission, depending on the size and complexity of your inventory.

Next, it’s about getting cozy with the numbers. Gather your purchase records to see how much stock has been added during the period. Don’t forget those invoices and receipts; they’re your golden tickets to accuracy. Subtract the COGS (Cost Of Sold Goods) from the sum of your beginning inventory and those new additions. This is where it gets mathematical, but with a calculator or software, you won’t break a sweat.

Keep a keen eye out for discrepancies. If your physical count and records don’t match up, you’re in for a game of detective — better to catch errors early than have them tangled up in your reports.

And remember, consistency is king. Stick to the same method — FIFO, LIFO, or Weighted Average — throughout the period to avoid convoluting your calculations. Switching gears mid-way can lead to a sticky situation with your financial reports.

Consider this a strategic mission; you’re gathering crucial intel that will help command your business battles. Get it right, and you’re not just a business owner; you’re a master strategist plotting your empire’s rise.

Calculating ending inventory is an advantageous practice for businesses, particularly in the eCommerce sector, and a vital step in the accounting process.

Illuminating Examples: A Practical Approach

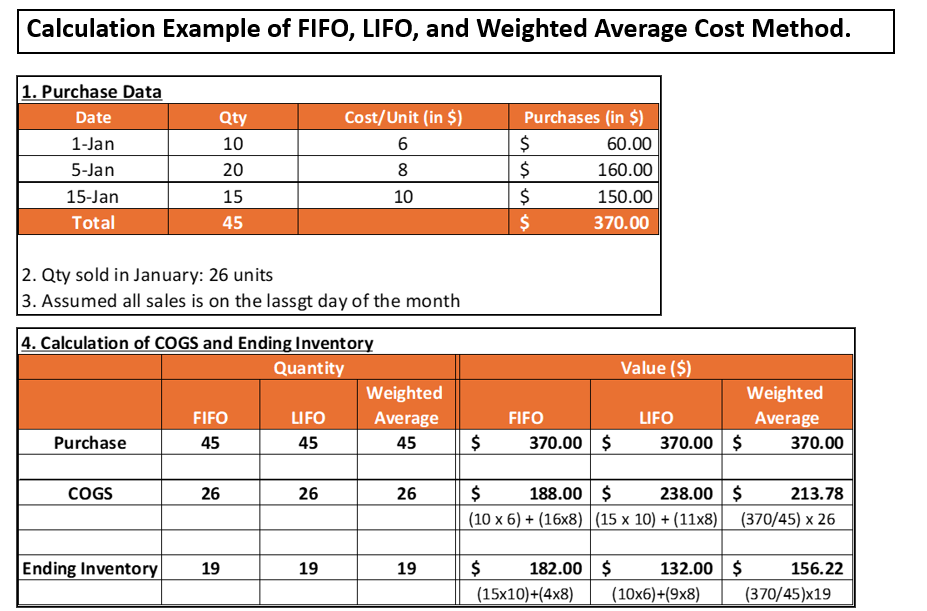

To get a firm grasp on ending inventory calculations, let’s roll up our sleeves and dive into some illuminating examples. Imagine you own a boutique chocolate shop – a sweet example, for sure!

Example 1: FIFO in Action

- Beginning Inventory: 100 boxes of chocolates at $2 each = $200.

- Purchases during the month: 200 boxes at $2.50 each = $500.

- Sales during the month: 150 boxes of chocolates.

Using FIFO, you’ll sell the oldest boxes first. Since your sales (150 boxes) are less than your beginning inventory (100 boxes) plus what you purchased first (50 out of 200 boxes), you’ll calculate COGS using the oldest price.

- COGS: 100 boxes at $2 each + 50 boxes at $2.50 each = $325.

- Ending Inventory: The remaining 150 boxes at $2.50 each = $375.

Example 2: The Weighted Average At Work Using the same starting figures, but with the weighted average method:

- Total Cost of Goods Available for Sale: $200 (Beginning) + $500 (Purchases) = $700.

- Total Units Available for Sale: 100 (Beginning) + 200 (Purchases) = 300 units.

- Average Cost Per Unit: $700 / 300 units = $2.33 per unit.

- COGS: 150 units sold x $2.33 average cost = $349.50.

- Ending Inventory: 150 units left x $2.33 average cost = $349.50.

Through these examples, you become a maestro maneuvering through numbers, bending them to sing the tales of your business journey. Employ these practices, and watch as the once-foggy realm of inventory calculation becomes clear as day, turning you into a financial virtuoso.

Emerging Technologies & Best Practices

Software Solutions for Accurate Inventory Management

In the digital age, you have a mighty ally in the battle for accurate inventory management: software solutions. Gone are the days of pencil-pushing and endless spreadsheets. Now, you can command a fleet of automated systems that sync your inventory data with the grace of a symphony orchestra.

These kinds of software solutions are like a trusty sidekick, tirelessly keeping an eye on every item that enters or sashays out of your store or warehouse. They banish human error to the land of myths and streamline the entire process, making sure that your reports reflect reality as closely as possible.

Top 5 Features:

- Real-Time Tracking: Watch your inventory levels ebb and flow in real-time. No more guesswork, just pure knowledge.

- Automated Reordering: Set thresholds that automatically trigger reorders, ensuring that you’re never caught off-guard by an unexpected rush.

- Analytics and Reporting: Unlock the stories behind the data to optimize your inventory levels and forecast with precision.

- Multi-Location Management: Command a view of your stock across multiple locations from a single dashboard.

- Integration with Other Systems: Sync with accounting and sales to maintain harmony across your business operations.

Benefits:

- Minimize human error, reducing the labor and heartache of manual stock takes.

- Save time on inventory counting and instead use it to woo your customers or strategize your next big move.

- Make informed purchasing decisions with historical data patterns within your grasp.

- Prevent stockouts and overstocking, ensuring you have just what you need — when you need it.

- Generate financial reports with a newfound ease, supporting compliance and strategic decision-making.

Cons:

- There might be a learning curve or initial setup costs involved.

- Over-reliance on technology can pose risks if not backed up with periodic manual checks.

Best suited for: Any business owner ready to say goodbye to inventory woes, embrace the efficiency of modern technology, and make informed, data-driven decisions. Whether you’re running a cozy local boutique or a sprawling multinational, these software solutions are poised to revolutionize the way you manage inventory. Welcome to the future — a land where accuracy in inventory management reignssupreme.

Harnessing the Power of Automation and RFID Systems

Unlocking the magic of automation and RFID (Radio Frequency Identification) systems is akin to discovering a secret passage in the inventory management labyrinth. It’s where modern technology wields its power, simplifying what was once a Herculean task.

RFID tags are a game-changer. These tiny electronic ambassadors store and transmit information about your items without requiring the line-of-sight needed for traditional barcode scanning. Attach one to a product, and you can track its journey from arrival to sale, all with little to no human intervention.

Top 5 Features:

- Instant Tracking: Locate and account for items in the blink of an eye.

- Enhanced Data Accuracy: Reduce errors from manual counts for a more reliable stock picture.

- Speedy Checkouts: Accelerate the sales process, pleasing customers and employees alike.

- Theft Prevention: Keep an electronic eye on merchandise, deterring sticky fingers.

- Seamless Supply Chain Integration: Manage the flow of goods from suppliers to customers with unparalleled efficiency.

Benefits:

- Stay ahead of the curve with inventory insights that inform smarter business moves.

- Wave goodbye to the time drain of counting and recounting stock.

- Bask in the glow of customer satisfaction as they revel in quick, accurate service.

- Nip inventory shrinkage in the bud with improved visibility and security measures.

- Embrace a level of detail and analysis previously unattainable, allowing a deep dive into inventory trends.

Cons:

- Initial investment costs can be significant.

- Over-dependency on technology might leave gaps in case of system failures.

Best for: Those ready to embrace 21st-century technology and edge out the competition. Whether you’re looking to streamline a retail operation, a bustling warehouse, or a complex supply chain, automation and RFID systems can marshal your inventory with an ironclad grip on accuracy. Welcome to inventory management that’s not just smart, but downright intelligent.

Realizing the Impact of Ending Inventory on Business

Why Precision in Calculation Equates to Business Health

Have you ever heard that ‘accuracy is the soul of good business’? When it comes to ending inventory, precision isn’t just a lofty goal – it’s the key to a robust business health. Precision in calculating your ending inventory means you have a clear view of your current assets, which informs everything from budgeting to strategic planning.

Accurate ending inventory figures give you the power to diagnose the health of your business with the precision of a seasoned doctor. This clarity allows you to identify problems like underperforming products or unexpected sales trends quickly. With real-time data, your response can be swift and surgical, ensuring your business remains hale and hearty.

Moreover, accuracy in ending inventory affects financial reporting, tax obligations, and can even influence investor perceptions. In essence, when you maintain precise inventory records, you’re not just keeping your books tidy; you’re ensuring the heartbeat of your business remains strong and steady.

Depending on your industry, a slight miscalculation can either be a minor hiccup or a full-blown catastrophe. Imagine a clothing retailer during the holiday rush — just a few miscounts could lead to a cascade of stockouts or overstocks, tarnishing the brand’s reputation and affecting the bottom line. Stay precise, and you are the maestro of a well-oiled machine, capable of scaling new heights of business success.

Connecting Ending Inventory to Net Income and Reporting

When it comes time to talk profits, the trail leads back to your ending inventory. It’s an intrinsic part of the calculation that determines your Cost of Goods Sold (COGS), which is subtracted from your sales to figure out your Gross Profit. But the plot thickens — your Gross Profit then dances with operating expenses, and what’s left is your Net Income, the grand finale of your financial performance tale.

It’s easy to think of ending inventory as just a minor player in this epic story. However, underestimate its impact, and your net income could be skewed, painting a misleading portrait of your business’s financial health. Overstate your ending inventory, and you might report higher profits than you’ve actually earned, leading to a potential tax boondance but also a false sense of security. Understate it, and the opposite happens; your profits seem shy, and you may undersell your business’ success.

When it’s time to unfurl those financial reports — a thrilling event for stakeholders and investors — the accuracy of your ending inventory stands as a pillar supporting the veracity of your entire financial narrative. Nail this, and your reports resonate with trustworthiness and transparency.

So, when you connect the dots between ending inventory and net income, what you’re really doing is ensuring the story your numbers tell is as true as it can be — that’s not just good math, it’s good business. With accurate reporting, you’re laying down a runway for your business to take off towards a future crafted with informed decisions, financial integrity, and a reputation for reliability that attracts investors and customers alike.

Overcoming Common Pitfalls in Inventory Calculations

Navigating Stock Discrepancies and Miscalculations

Navigating the choppy waters of stock discrepancies and miscalculations can be a daunting aspect of managing ending inventory. Yet, it’s an essential voyage if you aim to keep your business on an even keel. Picture this as charting your course through a sea of numbers, where every piece of your inventory holds the key to maintaining balance in your ledger.

The first step in your navigation is regular stock counts, a compass to guide you towards accuracy. These counts, when balanced against your recorded inventory, highlight discrepancies that could be due to a multitude of reasons: maybe an item fell overboard (was misplaced), walked the plank (theft), or was swept away by a rogue wave (damage).

Then comes scrutinizing your data entry process, where even the most minor errors can set you miles off course. A vigilant eye here prevents small mistakes from ballooning into financial icebergs down the line. And let’s not forget miscalculations — they’re like hidden currents that can suddenly change the direction of your profits and losses.

To navigate successfully, consider these proactive measures:

- Implement robust inventory procedures.

- Embrace technology like barcode scanning to lessen human error.

- Review and adjust regularly to account for changing conditions.

These are your loyal crew members, ensuring that when it comes to stock discrepancies and miscalculations, you’re always prepared to swiftly adjust the sails and set a course for true business prosperity.

So take the helm with confidence, knowing that as you navigate these challenges, you’re steering your business towards the shores of success, with every piece of inventory accounted for and every miscalculation corrected. The journey isn’t always smooth, but it’s always worth it.

Practical Tips for Consistent and Accurate Record-Keeping

To maintain a clear, navigable map through the landscape of inventory management, here are some practical tips to ensure your record-keeping is as consistent and accurate as the North Star.

Simplify and Standardize: Create a standardized process for recording all inventory-related transactions. Uniformity is your friend, making things easier for everyone to follow and enforce.

Embrace Technology: Leverage inventory management software to automate data entry and reduce the risk of human error. It’s like having a tireless, meticulous virtual assistant who never needs a coffee break.

Regular Reconciliations: Scheduled reconciliations can catch errors early. It’s like doing regular health check-ups for your inventory — preventing small issues from becoming big problems.

Training Is Key: Invest in training your team on the importance of accurate inventory tracking and the tools they’re using. Well-informed crew members make a shipshape business.

Audit Trails: Ensure your system supports a clear audit trail for each change in your inventory. It’s the breadcrumb trail you can follow back if something goes awry.

Physical Counts Are a Must: Despite the wonders of technology, regular physical counts are irreplaceable. They allow you to confirm that your digital records match the physical reality.

Review and Revise: Be open to reviewing your inventory process and making necessary adjustments. As your business evolves, your inventory system might need to flex and grow too.

With these tips, you’re not just churning out numbers; you’re crafting a chronicle of precision that safeguards your business’s bottom line.

These strategies require effort and dedication, but they’re the foundation of any successful business. Accurate record-keeping isn’t just about playing defense against errors; it’s about positioning your business to seize opportunities and drive growth with utmost confidence.

FAQs in Mastering Ending Inventory

What Exactly Constitutes Ending Inventory or closing inventory?

Ending inventory, or closing inventory, includes all the goods that a business has in its possession at the end of an accounting period that is unsold. This encompasses items in various stages of production: raw materials, work-in-progress, and finished goods ready for customers. It’s the last line item under the current assets section on your balance sheet, showcasing what you’re primed to sell in the next cycle.

How Does One Choose the Right Inventory Valuation Method?

Choosing the right inventory valuation method or Inventory valuation formula hinges on factors like the nature of your products, market conditions, and financial goals. Consider product shelf life—perishables work well with FIFO, whereas non-perishables might suit LIFO during inflation. Evaluate tax implications, since LIFO can lower tax expenses. Lastly, think about your business growth plans and how you want to portray your financial health. Consult with an accountant to align your strategy with accounting standards and make an informed decision.

Can You Estimate Ending Inventory Without COGS?

Yes, you can estimate ending inventory without the exact COGS using the gross profit margin method or the retail inventory method. Both approaches use historical data or ratios to approximate the value. While not precise, these estimates can help for interim financial statements or when a physical inventory count isn’t feasible. Nonetheless, for accuracy, eventually, you’ll want to nail down the true COGS.

What Are the Implications of Inaccurate Ending Inventory Records?

Inaccurate ending inventory records can wreak havoc, leading to misstated financial statements, misguided business decisions, and tax discrepancies. You might either overpay or underpay taxes, and poor stocking decisions could result from skewed data, potentially causing excess inventory or stockouts. This inaccuracy can hurt your company’s reputation, investor relations, and customer satisfaction. It’s a domino effect that can ripple through your entire operation.

How to calculate ending inventory using the fifo method?

To calculate ending inventory using the FIFO method, follow these straightforward steps:

- Start by listing your inventory purchases and production costs in chronological order, with the oldest costs first.

- Then, determine the total number of units sold throughout the period.

- Multiply the number of units sold by the cost of your oldest inventory to find the COGS.

- Subtract this COGS from the total cost of inventory purchased to arrive at the ending inventory cost.

Remember, this method assumes that the earliest goods purchased are the first ones sold.